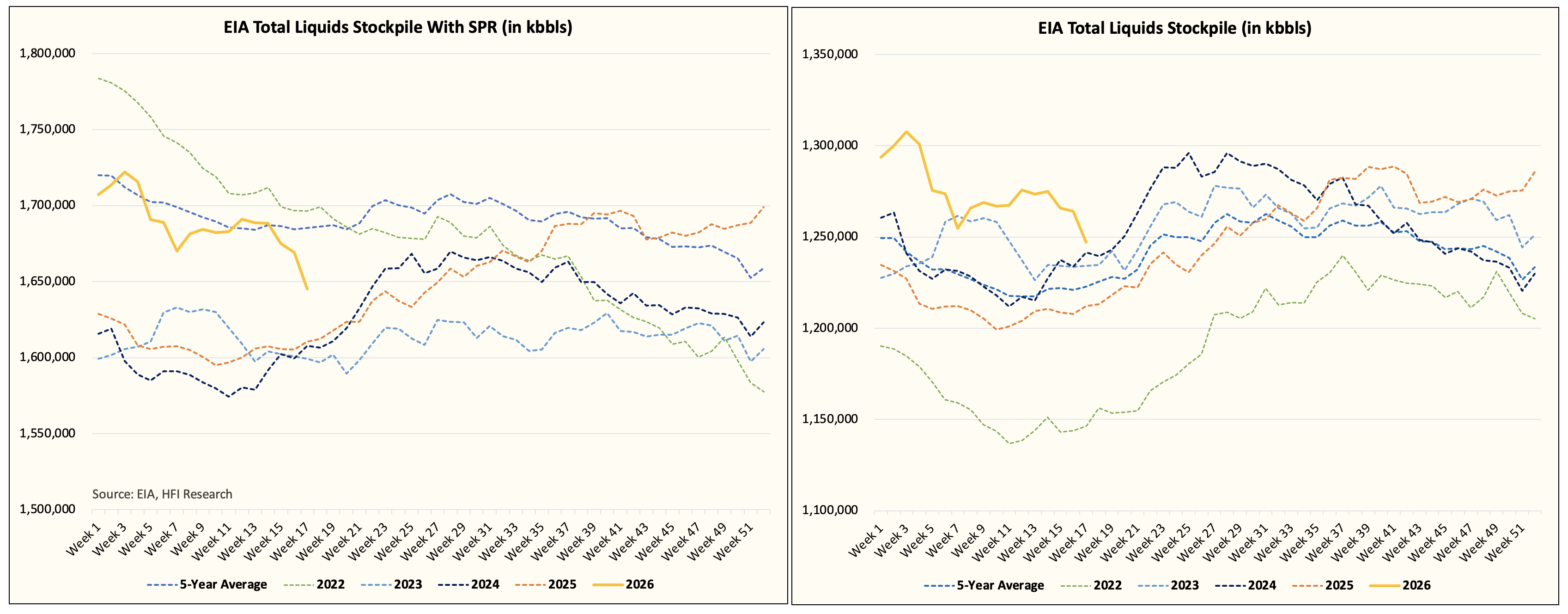

There was a rude awakening in the oil market today. EIA reported a monstrous 24.1 million bbl decline in oil inventories. SPR release was 7.1 million bbls. US commercial crude storage declined 6.2 million bbls.

As we explained over the past 2 weeks, visible oil inventories will start to plummet. Today was just a preview of the many more inventory draws ahead. The crazy thing is that even if the Strait of Hormuz opens this very second, the incoming oil inventory draws won’t stop due to the logistical timing issues we explained here.

In this article, I will answer the following questions:

What does the sequencing look like? (What happens first, etc)

What happens to oil prices?

Sequencing

Let’s start with sequencing because there’s a lot of misinformation out there.

The Strait of Hormuz closure is impacting crude flows more than product flows.

Now I’ve seen some generalists bring up the comparison to 2022, so this needs to be cleared up first. In 2022, there was a global refinery shortage. Due to mandated COVID stay-at-home policies from 2020 to 2021, global refinery throughput declined structurally. Following Saudi’s oil price war in March 2020, the historic OPEC+ production cut that began in May 2020 led oil inventories to normalize by the end of 2021.

As Russia invaded Ukraine in March 2022, the global oil landscape was already tight on products, so the fear of sanctions on Russian oil led the market to panic over concerns about products. This was most notable in diesel. And since the world was short on refining capacity and no crude supplies were lost, refining margins took the bulk of the price increase, while crude lagged. This is why you never saw Brent surpass $125/bbl.

To summarize: 2022 was due to 1) low global oil inventory stockpile, 2) shortage of refining capacity, and 3) no loss in crude supplies.

It’s important to understand this framework because it will help you understand the sequencing I’m about to explain.

The Strait of Hormuz closure is resulting in an 11 to 12 million b/d loss of crude. Here’s the breakdown by country:

Saudi: 3.5-4 million b/d

UAE - 1.75 million b/d

Iraq - 3.5 million b/d

Kuwait - 2.35 million b/d

Bahrain - 0.18 million b/d

Total shut-in: 11.33 to 11.83 million b/d.

You will see others talk about the product flow outage, but to be conservative, I’m just assuming it gets replaced by refineries outside of the Middle East.

Asia is the most dependent on this crude supply. Following the Strait’s closure, we saw China ban the export of products. This immediately sent Asian refining margins higher. This was the first event in the sequencing.

Asian refineries outside Japan, South Korea, and China do not hold sufficient crude in stock to last more than 2-3 months. The immediate impact is that if there’s no flow arriving, refineries have to reduce throughput. This, coupled with China’s ban on product exports, kept refining margins high.

But again, the main shortage here is crude, so while refining margins gained initially, it’s not the segment that will gain the most.

My analysis indicates that global refining margins have already peaked. Refineries are now exiting maintenance season, so every refinery is incentivized to maximize throughput.

Based on the current refining margins, crude can rally another $20 to $25 per barrel. This will squeeze refining margins, so refineries with insufficient crude will throttle throughput again. If end-user demand can absorb higher product prices, margins will rebound once throughput is reduced, and the cycle will rinse and repeat.

In essence, refining margins will bounce back and forth from here on out, while crude is going to stay in an uptrend. Unlike 2022, most of the upside this time will be in crude.

For the time being, we are far too early in this cycle to be looking for the “turning point”, but as I explained in this article, we have all the signals in place.

What’s Next?