Please read “The Oil Market Breaking Point” article.

In our write-up published on March 25, we outlined a range of scenarios and explained that the oil market’s breaking point would be mid-April. We are now past the breaking point.

From this moment forward, the 11 to 13 million b/d of supply outage will either show up in 1) crude storage draws, 2) product storage draws, or 3) demand destruction.

For those of you not familiar with the logistics or logic of this, let me bring you up to speed.

The oil market breaking point coincided with the last barrels from the Persian Gulf to the end user. Once those tankers offload the barrels onshore, the lack of offloading will start to drain onshore oil inventories. (For additional details on the onshore storage math, please see this write-up.)

At the moment, the global refinery outage is over ~5 million b/d, with ~3 million b/d concentrated in the Middle East. Asia and Europe are both reducing refinery throughput, but just because refineries throttle back doesn’t mean end-user demand is down.

The subsequent reduction in refinery throughput will lead to faster product storage draws, raising petroleum product prices. This cycle will then feed itself back into higher refining margins and, thus, higher refinery throughput.

This cycle will rinse and repeat for a few more weeks:

Elevated crude prices > compressed refining margins > lower refined products > lower product storage > higher refining margins > higher throughput > higher crude prices

On the physical market, you will see this game being played by traders who hold storage and refineries that don’t have storage. This, of course, will only last as long as there is something to draw down in onshore crude storage, but that time is running out soon.

By the first week of May, the only Asian countries with real excess in crude oil inventories will be Japan and China. Everyone else will have to scramble for barrels on the market, and if the Strait of Hormuz remains closed, that’s when you will see refineries pay any price they can to secure the barrels they need. Because the alternative is shutting down the refinery.

For Europe, the lack of crude will become apparent by the same timeframe. US crude exports will have averaged near ~5.5 million b/d by then. OECD crude oil inventories will have reached operational minimum with the remaining excess crude in storage residing in the US.

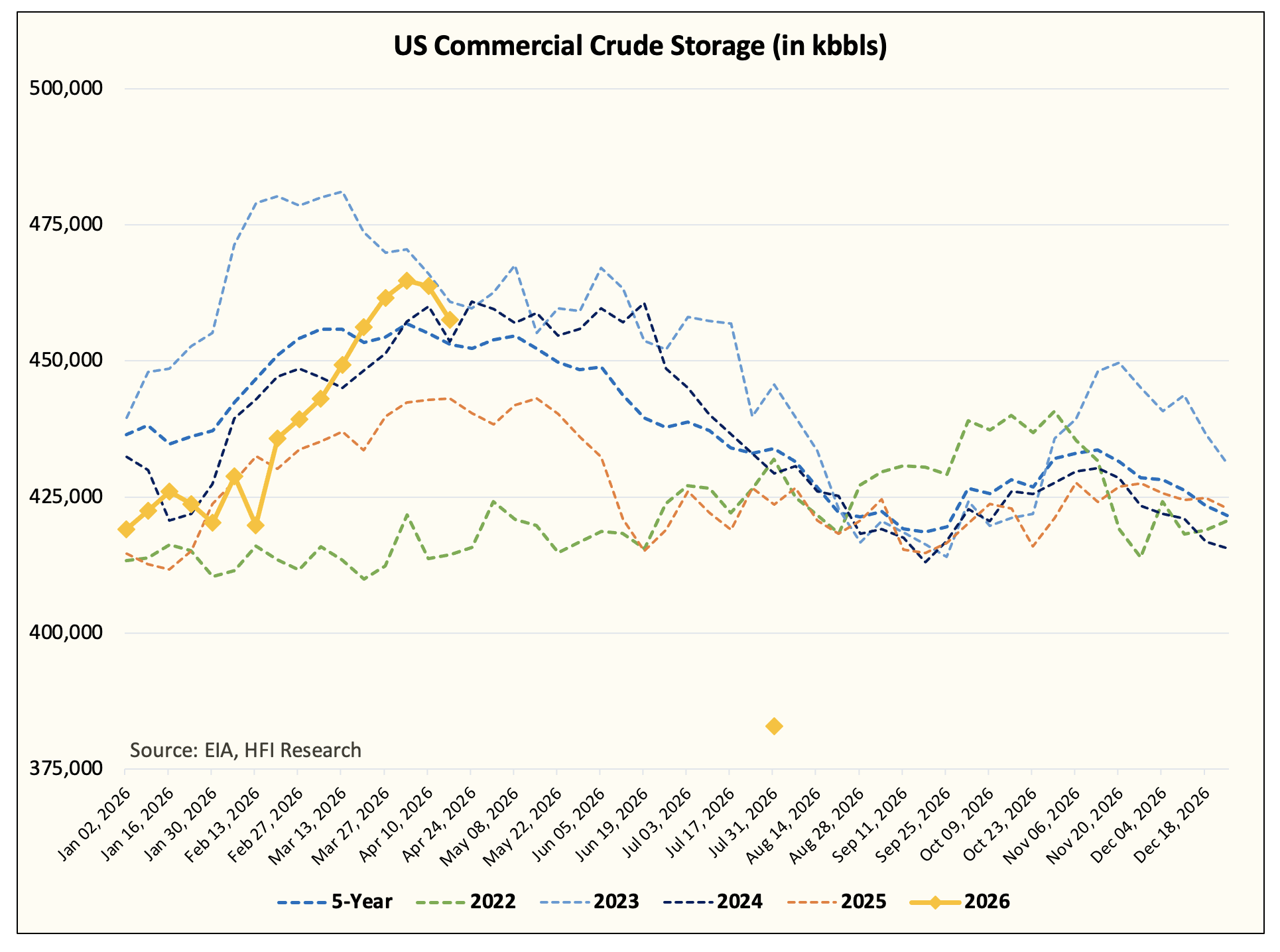

By our estimate, US commercial crude storage will be below ~400 million bbls and approaching the operational minimum (370 to 380 million bbls) by the end of July. This includes an estimated SPR release total of 139 million bbls.

At some point between now and then, the Trump administration will have to ban both product and crude exports. We suspect that Trump would ban product exports first, and if US refineries start throttling throughput due to a compression in margins, they will ban crude exports after, which would be a disastrous scenario for US shale and Canadian oil producers (more on this in a later write-up).

Everything I just wrote above will play out regardless of what happens to the Strait of Hormuz. Even if the US and Iran reach an agreement to reopen the Strait of Hormuz without conditions, onshore oil inventory draws will materialize.

Rationale Explained Again

Let’s say that by Tuesday, the ceasefire ends with a long-lasting peace deal in place.

There are ~160 million bbls of floating storage in tankers that will rush for the exit. These barrels will take 30-40 days to transit + offload. For these tankers to return, it would take an additional 20 days.

As for the other segments in the market, there are 70 VLCCs headed for the US right now to load US crude and offloading to Asia. The time it takes for these VLCCs to load will be 6-8 weeks. Transit time to Asia will be another 45-50 days. To offload and go back through the Strait of Hormuz would be another 20-25 days. In total, we will not see meaningful tanker traffic back in the Strait of Hormuz from this entourage for at least 3 months.

To alleviate the current onshore storage build-up in the Middle East, we would need at least 100 VLCCs. There are 600 million bbls of onshore storage, and to give producers enough cushion to restart production, onshore storage needs to drain down by ~200 million bbls. Again, tanker activity shows that’s not physically possible until mid-to-late June, at the earliest.

Once the onshore crude storage drains, we need a steady flow of tankers coming to through the Strait of Hormuz to pick up crude. By this point, producers like Saudi, UAE, Kuwait, Qatar, Iraq, and Bahrain can restart. This process will take a few more weeks all but guaranteeing that the lack of supply continues.

Again, by our rough estimate in the March 25 Breaking Point write-up, the cumulative storage lost due to the closure is already ~1 billion bbls. This increases to 1.2 billion bbls by the end of April, 1.59 billion bbls by the end of May, and 1.98 billion bbls by the end of June.

We do not have enough commercially available crude for that much supply loss. This is why demand destruction is needed to prevent such a scenario from materializing.

This is just math.

The Problem With The Geopolitics

I hate geopolitics. It’s unpredictable. There’s no margin of safety. It’s a lot of grey and never black and white. But in the case of the Iran conflict, it seems to be all-or-nothing.

My friend PauloMacro recently recommended Professor Robert Pape, author of the Escalation Trap. And I digested everything he wrote and talked about over the last 2 months. He recently shared a piece titled, “Why the Ceasefire Keeps Failing.” I recommend that you read that.

Now speaking from my experience, what I witnessed this weekend came straight out of a horror film.

Since the conflict began at the end of February, most tankers have chosen to do nothing and wait. There were theories that the Strait of Hormuz was closed due to a lack of insurance. I also shared that view in the early stages of the conflict, but as the events progressed, especially what transpired this weekend, I was shocked.

IRGC physically implemented the closure by threatening tankers with gunfire. We saw this visibly through tanker activity. This is the first time since we started tracking tanker activity that we saw tankers turn around in volume. In the past, we saw maybe 1 or 2 tankers do that, but not in the size it did this weekend.

To me, this signals that 1) IRGC is firmly in control of the Strait of Hormuz and 2) the conflict will need to get worse before it gets better. It is clear from the demands that the IRGC/Iran is making that the US would never agree. So the option is very narrow here, and the only way to solve this issue in the long run is to “solve” it if you understand what I’m saying. I fear the worst has yet to come, and I don’t say this lightly.

Oil Market Scenarios

In our previous article on the oil market’s breaking point, we explained that if the Strait of Hormuz opens by the end of April, Brent will “drop down” to $110/bbl; it’s trading at $95 today.

As I already explained, the oil market has passed the breaking point. The onslaught of oil inventory draws coming will shock the market awake. I suspect that only when financial players see the physical shortages playing out will they wake up to the reality that this supply outage is real. Until then, most people will not be able to accept the reality.

It is what it is.

If the Strait of Hormuz opens after April, we cannot provide an accurate oil price forecast. We will have crossed too deep into the Rubicon. This will have been the largest oil supply outage in the history of the oil market by a magnitude of 4x. Fundamental market theories will no longer apply here because there’s no price for outright shortages. When a market runs out of fuel, it just runs out.

What does that last marginal barrel trade for? I have no idea, and I don’t think anyone will be smart enough to know the answer.

What I do know is that demand destruction is coming, and for oil watchers, policy announcements will be what “kills” demand. To balance ~11 to ~13 million b/d of global supply outage, we need the same magnitude of demand loss as during the mandated COVID lockdowns.

And even in that dire scenario, the market will be “balanced” and not in surplus. But it will have dampened the impact on price, and the barrel counters, including myself, will know when the inflection point (fundamentally speaking) is here.

So if you want a short summary:

I have no idea what happens to oil prices if the Strait of Hormuz stays closed past April, but it’s not $95/bbl.

Policy-mandated demand destruction will rebalance the oil market, but only keep storage from declining further.

We have developed market signals in place to watch for this turning point when it comes.

Conclusion

The oil market breaking point is here. Global onshore oil inventories are going to plummet, and the decline will be at a pace no one has ever seen before. US oil inventories were the last to start declining, and we will see it in next week’s EIA oil storage report. Once the market sees the visible onshore inventory draws, prices will quickly inflect.

If the Strait of Hormuz remains closed past April, no one will be able to tell you where oil prices top out. We will have gone too far into the Rubicon. Oil demand destruction will be the only way to rebalance the price, so instead of fixating on “price”, we need to follow the signals.

But if there’s anything you can take away from this article, it’s this:

The oil market won’t rebalance at $95 per barrel. Oil prices will have to reach a level high enough to offset ~11 to ~13 million b/d of supply outage. Governments will have to mandate COVID-like demand reduction policies to depress demand. Even then, it will have only offset the supply outage and not pushed the oil market into surplus. On the geopolitical side, I fear that we have entered a phase of “getting worse before it gets better,” as both sides (the US and Iran) appear not to budge.

On the investing side, I put my money where my mouth is.

Here are the following trade alerts we published to paid subscribers:

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO, UCO, BNO call options, USO call options either through stock ownership, options, or other derivatives.

Long USO May $135, $145 strike calls.

Long USO May $215-$245 call spreads.

Long USO June $125 calls.

Long BNO July $50 and $60 calls.

It is baffling to me that oil is currently less expensive than it was Thursday. We are back to a stalemate, and another roughly 50 million barrels of oil weren't produced. We must be living in a parallel universe.