(WCTW) The Oil Market Breaking Point

Looking at the various scenarios for oil prices using the latest data.

In this piece, I will break down for you the various scenarios on the horizon. Now that we are nearly 4 weeks into this Iran conflict, what does that do to the oil market?

On March 9, we published a public piece titled, “My Latest Thoughts On The Oil And Natural Gas Market Amidst The Iran Conflict.” In it, I said:

Here’s what this means for oil prices (bbls lost scenario includes time to bring back production):

Scenario 1: Tanker flows resume tomorrow: Brent will average in the high $70s to low $80s for the rest of the year. (~210 million bbls lost)

Scenario 2: Tanker flows resume by March 15: Brent will average in the mid to high $80s for the rest of the year. (~290 million bbls lost)

Scenario 3: Tanker flows resume by March 22: Brent will average in the low $90s for the rest of the year. (~370 million bbls lost)

Scenario 4: Tanker flows resume by March 29: Brent will average in the mid-to-high $90s for the rest of the year. (~450 million bbls lost)

I don’t even want to contemplate what will happen to the oil market if tanker flows don’t resume to normal by March 29. Oil demand destruction is the only way out of it, and the prices will have to be extreme.

Soon after the report, IEA announced a global SPR release totalling 400 million bbls. This will dampen the impact of the supplies lost, but as we discussed in our follow up piece titled, “The IEA Just Gave Oil Bulls The Biggest Gift Ever By Coordinating The SPR Release.“ I wrote:

From an oil trading standpoint, traders will be reluctant to push oil prices up until the cushion is gone. The simultaneous SPR release will help dampen a lot of the worries over immediate supply needs, but it will only be a short-term fix. The market will remain on edge and with each passing day that tanker flows don’t return to normal, oil prices will gradually shift higher.

On the downside, an immediate ceasefire or any truce will send oil spiraling lower. For example, if a peace deal is announced before March 15, the net balance to global oil inventories will be +110 million bbls (400 million bbls - 290 million bbls).

This has the potential to send Brent back into the mid-$70s.

On the other hand, if there is no peace deal, and the disruption lasts until the end of March, the net balance will be -50 million bbls. With each passing week, the deficit increases by ~80 million bbls.

So yes, SPR buys time, but it does not fix the issue at hand. Tanker flows need to return to normal.

Thankfully, it does prevent a catastrophic price spike scenario in the near term, which will prevent meaningful demand destruction from taking place.

Fast forwarding to today, we are now at the March 29 scenario we laid out at the beginning of the month. Let’s look at the latest facts to discern where the oil market is headed.

Facts

Production shut-in total from Saudi Arabia, the UAE, Kuwait, Iraq, and Bahrain has reached 10.98 million b/d.

Iraq: -3.6 million b/d

Kuwait: -2.35 million b/d

UAE: -1.8 million b/d

Saudi: -3.05 million b/d

Bahrain: -0.18 million b/d

Saudi has maxed out the East-to-West pipeline. It is currently exporting ~4 million b/d in the Red Sea.

The UAE can also bypass via the Abu Dhabi pipeline (Habshan-Fujairah). The ~1.8 million b/d is also maxed out.

Tanker traffic flow in the Strait of Hormuz remains nonexistent. The fact is that even if the war ends tomorrow, it will take a few months to increase production and resume normal traffic.

Scenarios

I will give you three scenarios:

The war will end by the end of this week. Traffic returns this weekend.

The war ends by the middle of April.

The war ends by the end of April.

Keep in mind that the SPR release of 400 million bbls bought the oil market more time versus our initial assessment (from March 9). Oil price scenarios below will reflect the change in SPR.

Scenario 1: Ends this week

Impact on global oil inventories: -50 million bbls (including SPR release)

Impact on Brent: initial sell-off into the low-$80s before averaging in the mid-to-high $80s for the rest of the year.

Scenario 2: Ends the middle of April

Impact on global oil inventories: -210 million bbls

Impact on Brent: initial sell-off into the low-$90s before averaging in the mid-to-high $90s for the rest of the year.

Scenario 3: Ends at the end of April

Impact on global oil inventories: -370 million bbls

Impact on Brent: initial sell-off into the $110s before averaging $110-$120 range for the rest of the year.

Breaking Point: Mid-April

For the oil market, there will be a breaking point. For the time being, the market is taking the view that the conflict will resolve before the middle of April. This view is important in the context of analyzing where oil prices are headed.

Oil is priced on the margin, and as long as there’s enough “supply” to go around, the market won’t panic. What you are seeing in the oil market today is a lack of panic. The combination of jawboning from the Trump administration, sanction relief on Iran/Russian crude, and the SPR release have kept prices at bay. None of it will work once we hit this breaking point.

For now, the evaporation of global oil-in-transit has not translated to onshore inventories just yet. Our estimate is that by the middle of April, this will come full steam ahead.

If the conflict is not resolved by mid-April, IEA will need to coordinate another SPR release of ~400 million bbls. Without this action, oil prices will reach demand destruction levels ($200+).

Longer-Term Impact

In Energy Aspect’s latest weekly perspective, it noted that the total supplies lost for the market will total ~930 million bbls. It is estimated that the cumulative production lost from May to December is ~340 million bbls.

Their estimate is far more aggressive than ours. In our storage sensitivity analysis, we did not factor in how countries like Iraq and Kuwait will take 3-4 months to bring production back to normal. It appears that we may be far too conservative on this front.

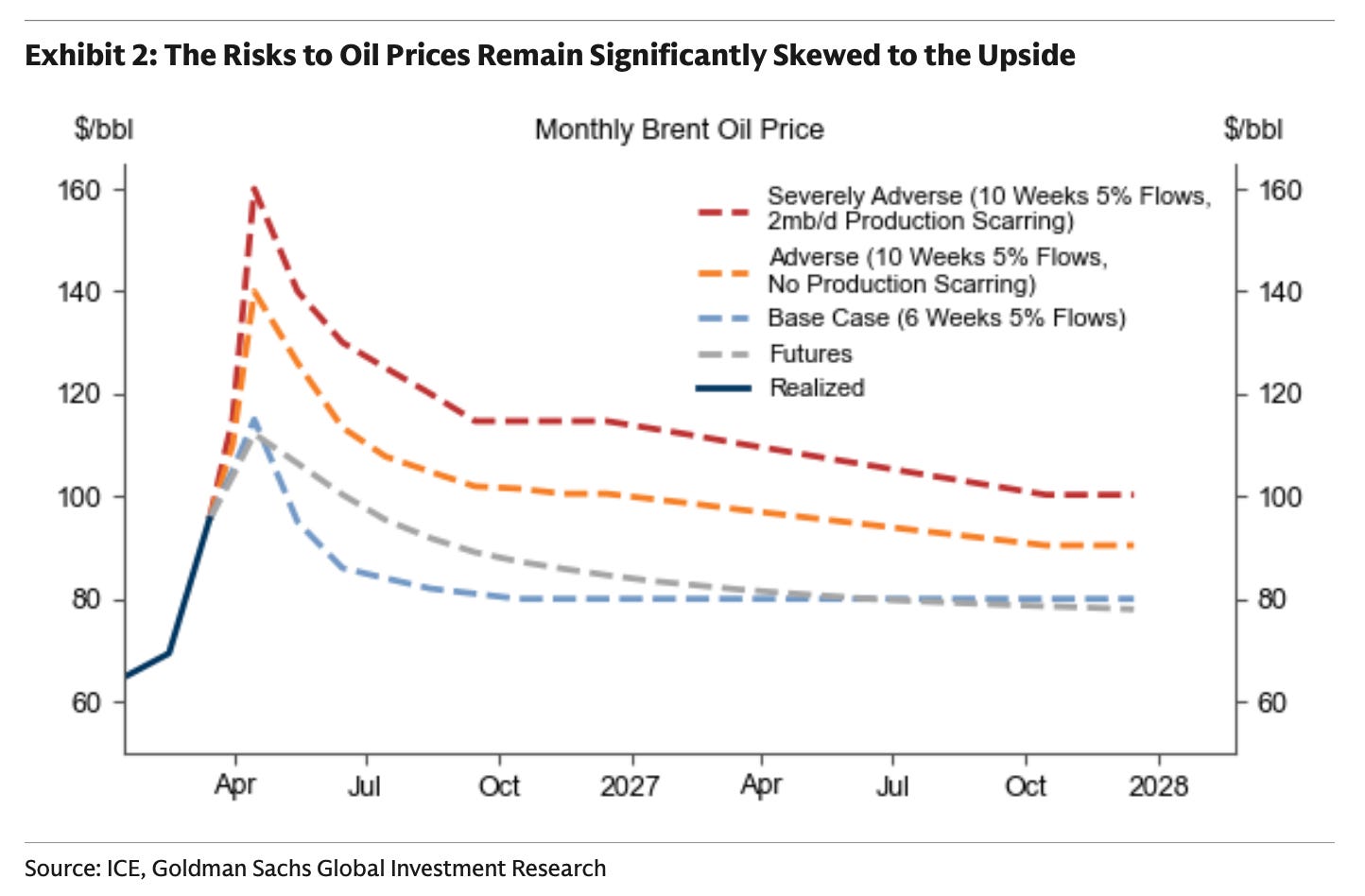

For Goldman, the longer the conflict lasts, the higher oil prices will last.

In the above scenario, Goldman gives the scenarios of what it would look like if the conflict is prolonged for another 10 weeks. It aligns with the scenario we gave above.

In essence, there’s a breaking point in the oil market. Once we’ve crossed the rubicon, there’s no going back.

Readers should expect structurally higher oil prices going forward. The supply losses we are seeing today will have a meaningful impact on global oil balances going forward even if the war ends at the end of this week.

How Long?

I have so far refrained from commenting on “when” I think this conflict will end. This is motivated in part from not jinxing myself and in part because I have no idea when it will end.

But I will just say this, unlike the previous conflicts, where there were efforts made to “escalate to de-escalate”. I just don’t see any of that now. The retailiatory attacks are done with zero notice. Iran appears to be targeting Gulf nations as opposed to just targeting Israel alone. The response is what initially prompted me to think that, “this time was different.”

Now that the conflict has gone on for nearly 4 weeks, I fear that with each passing day there’s no deal, the probability of a deal diminishes greatly. As I explained in our piece titled, “Running Out Of Time.” Iran is fully aware of the math behind the oil market. All it needs to do is wait for the breaking point to unfold in the oil market before extracting max concessions from the US. From a tactical standpoint, it has no advantage to reach a deal now. The Strait of Hormuz card has been played and it can’t be replayed again in the future.

For the Gulf Coast countries, if the current Iranian regime is not toppled, it will be held hostage to this situation time and time again in the future. This is unacceptable even if there’s some framework for a “toll fee” going forward.

As a result, the logic leads me to believe that it’s not up to the US to dictate terms here. It’s up to the Iranians, and given this being the case, it will push for the breaking point in the oil market. It will test the US’s resolve. All it needs to do is “survive” for another 3 weeks before things start to break.

But again, I am not a geopolitical expert. I have no idea what I’m talking about here. All I can tell you is that from a fundamental standpoint, this is where we stand today.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO, UCO either through stock ownership, options, or other derivatives.

I am long: USO May 15, 2026, $215-$245 call spread, USO May 15, 2026, $135 call.

Just to play devil's advocate: given the current conditioning of the oil market (assumption that war will end imminently, jawboning from trump etc), why couldn't the market just assume that by April 15, IEA releases another 400mbbl from SPR again, pushing the 'breaking point' out further? Given that we are operating in markets that are addicted to selling risk premia, don't we need to stress test when is the *actual* final breaking point where no other options are left in world stocks? Do you have any sense for when this would be? 1. If SPR releases another 400mbl from SPR, how many more weeks does that buy? 2. How many total barrels does global SPR have left to release and how many weeks do those barrels provide assuming they are all released and SPR stocks go to zero?

Is there any chance that China might release some oil from its SPR?