Unprecedented, that’s the only way to describe everything that’s going on in the energy market today.

The Iran conflict is creating the largest supply reduction in the history of the oil market. No other disruption even comes remotely close to this.

We have been updating in real-time the tanker flow videos on X, and things look grim.

Some tanker tracking firms have noted that tankers are still moving through the Strait of Hormuz, but their AIS (automatic identification system) is turned off.

That’s probably the case, but the most important point still stands: the traffic in the Strait of Hormuz is nonexistent.

With each passing day that goes by with no visible tanker movement, these are the impacts on the energy market:

~19 million b/d of crude, condensate, and products.

~20% of global LNG.

Natural Gas (LNG Market)

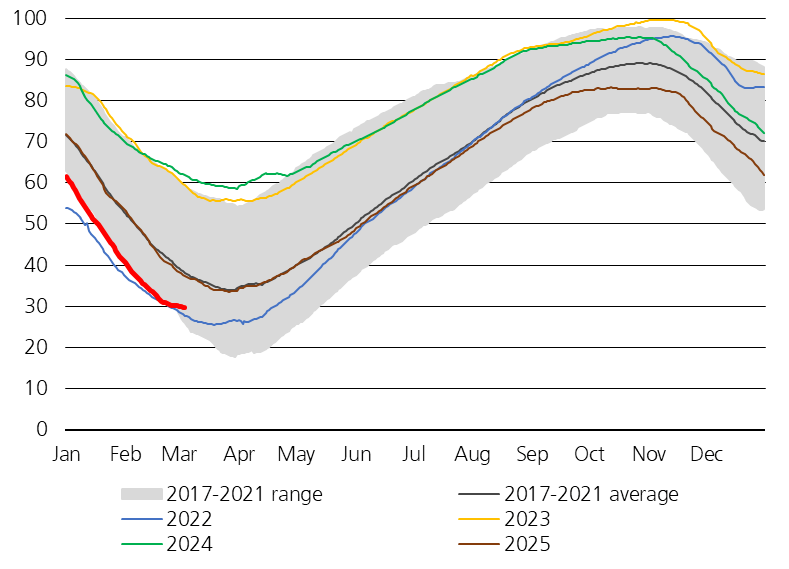

At the moment, Qatar has reduced or shut down its LNG facility, which would take weeks to come back online. This is ~20% of global LNG flow, and with each passing day, the global natural gas storage situation worsens.

The situation in the global natural gas market is unique because natural gas is a unique commodity. Natural gas is a time-sensitive commodity. We should all be thankful that we were past the heart of the heating demand season before this chaos unfolded, but as the injection season gets underway, we have 32 weeks (from the beginning of April to November) before we enter the next heating demand season.

These injection months are crucial to price stability in the upcoming winter. Without sufficient natural gas storage, we will have uncontrollable price spikes. In 2022, Russia invaded Ukraine in March, after the heart of the heating demand season, European natural gas prices reached levels that destroyed industries.

We are on a similar path.

Source: Giovanni Staunovo

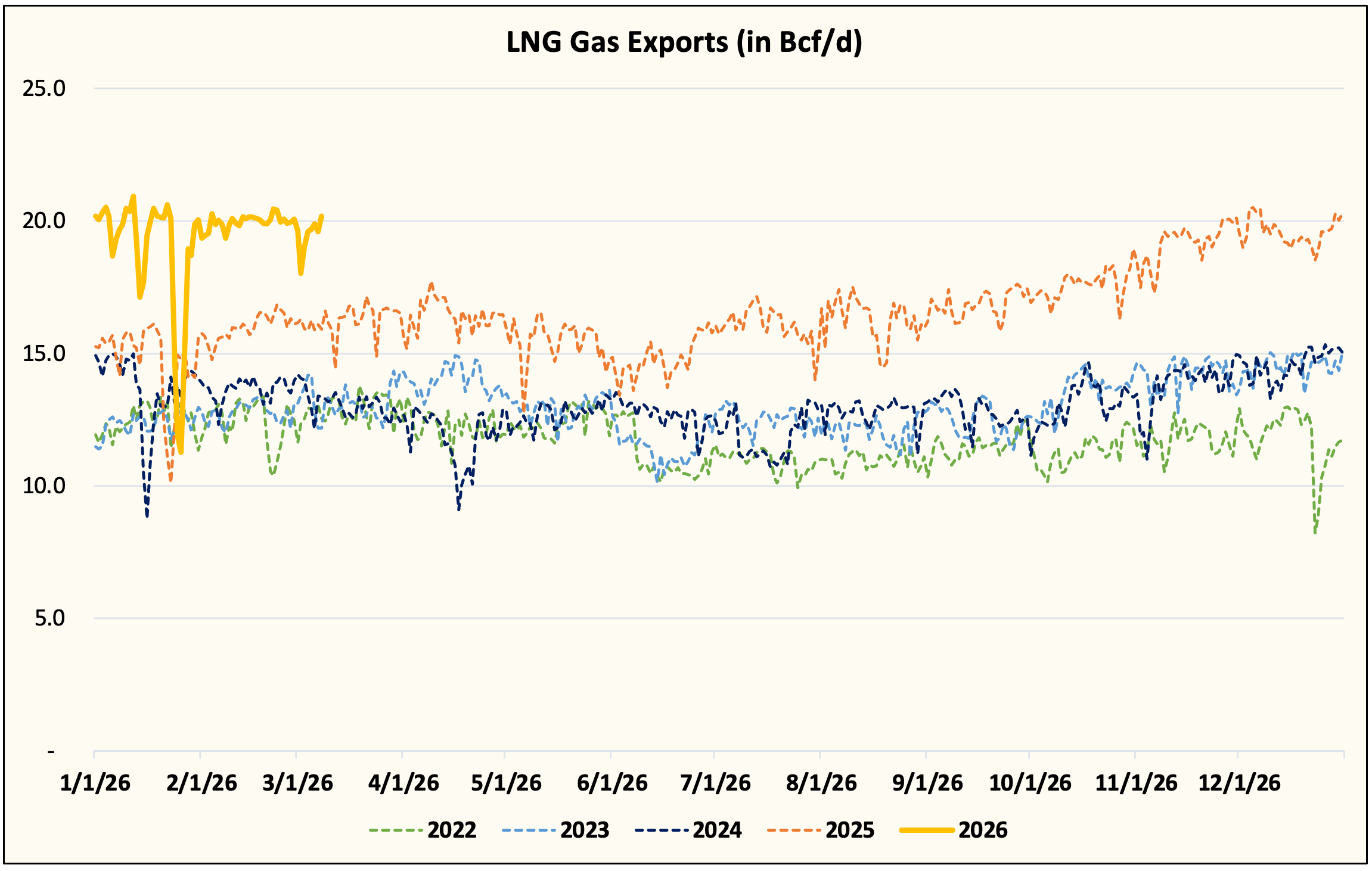

Luckily, this time around, US LNG exports are meaningfully higher than in 2022 (+8 Bcf/d), so the price spike won’t be as severe. (Note: The US supplies ~36% of global LNG flow.)

But as long as Qatar’s outage persists, US natural gas prices will continue to rise. US LNG exports this year will operate at max capacity. We alluded to this effect when we discussed our long BOIL position in this write-up.

By the end of this week, if the Strait of Hormuz situation doesn’t correct, Henry Hub will reach $4.5/MMBtu+. Some of you might be wondering, shouldn’t Henry Hub trade according to US natural gas fundamentals? Yes, but a similar thing unfolded in 2022 when global natural gas prices skyrocketed. We don’t expect a similar parabolic rise this time around, but it’s not correctly priced at $3.42/MMBtu (prompt month).

Oil

This is what the Strait of Hormuz closure (not technically closed) is doing to the oil market.

Each day that goes by with no flow, oil-on-water is dropping by ~11 million bbls (~77 million bbls per week).

Production shut-in has already reached ~4 million b/d, and by the end of this week, this figure is expected to hit 6.5 to 7 million b/d. Storage capacity is reaching its limits in Iraq and Kuwait. The UAE is next, followed by the Saudis. Saudi oil production won’t shut in unless this conflict lasts more than a month, but the damage to the global economy would already be done.

Even if the tanker flows return to normal tomorrow, logistical jams will keep production shut-in for at least a month.

Here’s what this means for oil prices (bbls lost scenario includes time to bring back production):

Scenario 1: Tanker flows resume tomorrow: Brent will average in the high $70s to low $80s for the rest of the year. (~210 million bbls lost)

Scenario 2: Tanker flows resume by March 15: Brent will average in the mid to high $80s for the rest of the year. (~290 million bbls lost)

Scenario 3: Tanker flows resume by March 22: Brent will average in the low $90s for the rest of the year. (~370 million bbls lost)

Scenario 4: Tanker flows resume by March 29: Brent will average in the mid-to-high $90s for the rest of the year. (~450 million bbls lost)

I don’t even want to contemplate what will happen to the oil market if tanker flows don’t resume to normal by March 29. Oil demand destruction is the only way out of it, and the prices will have to be extreme.

As for the prompt-month oil futures, each passing day will result in more severe, more parabolic moves. My guess will be as good as yours, and so my advice would be to use the scenarios above to figure out what price you want to pay for energy stocks using our updated E&P valuation sheet.

What is the catalyst to fix this?

We initially thought that the Trump administration’s policies on DFC insurance (for tankers) would at least encourage some tankers to move. That’s clearly not the case.

Jon and I have debated about how this will be resolved. Jon’s view is that Trump will give up on this because of the following reasons:

Trump will TACO because of elevated oil prices, the impact on the global economy, and the timing for the midterm elections.

High oil prices will hurt the US economy, his voter base, and the outcome of this year’s elections.

The disruption is too great for it to continue.

It’s hard to argue against all that.

Now, what happens if Trump doesn’t TACO?

Naval escort + ground invasion in the South to secure the Strait of Hormuz stretch. This would take a long time.

A far bigger and better insurance coverage is provided by the US. Dr. Anas Alhajji continues to believe that it’s an insurance issue preventing the tanker flows from resuming. If so, the DFC will have to substantially increase the coverage size of $20 billion.

Iran reaches a peace agreement with the US and Israel. That seems unlikely given everything that has unfolded so far. Mojtaba Khamenei is now the Supreme Leader, and he appears to be more hardline than his father was.

In essence, outside of a full retreat, the conflict will continue, and given the uncertainty on tanker flow, things look grim for now.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BOIL either through stock ownership, options, or other derivatives.

I have one question. Can you explain just a bit more why it would take at least 21 days for production to resume where it has been shut in. I would love to understand that better. If that is true, it really changes how I think about things. Thank you very much in advance.

Another comment. Can you please explain the math. This is very important. If only 6 million barrels of production are currently offline, 400 million barrels divided by 6 million is a bit over two months. If production lost increases to 10 million barrels, then that is 40 days.