IEA just announced the largest ever strategic petroleum reserve (SPR) release in history: 400 million bbls.

This is the best gift the oil bulls can ever ask for.

Let’s be real, no one wants oil prices shooting past $120/bbl.

First of all, you can’t even make money off of that price spike unless you are only long prompt month oil futures.

Second, energy stocks will never reprice using the prompt month. Most of the price rally will be centered on the front end of the futures curve, so what you will see is massive backwardation followed by depressed oil prices down the curve.

Finally, the price spike will prompt demand destruction, so you end up pushing down demand while producer equities don’t benefit. No one wants that.

What the SPR release does is it buys the global oil markets additional time to get through the disruptions we are seeing in the Strait of Hormuz. Remember that the oil market operates just as much off of sentiment as it does fundamentals.

Our analysis indicates that the maximum SPR release rate is between 3 to 4 million b/d (globally). EIA notes that the US SPR release rate is ~4.4 million b/d, but that’s the technical maximum. In 2022, we saw the max closer to ~1.5 million b/d.

The current disruption in the Strait of Hormuz is ~11 million b/d (crude only). Production shut-in total is 4 to 7 million b/d with that figure increasing with each passing day. Producers in the Gulf have already filled available tankers offshore with crude and the buildup in onshore inventories are reaching a peak. We will hear additional production shut-in soon if tanker flows don’t return to normal by the end of this week.

The Immediate Cushion

As we detailed in our WCTW last week titled, “Why Aren’t Oil Prices At $100?“ This is what we wrote about the immediate cushion for the global oil market:

The Middle East exports ~19 million b/d of crude + condensate + product through the Strait of Hormuz. Saudi’s East-West pipeline has a capacity of ~5 million b/d, but a chunk of that was already in-use. UAE also has the ability to bypass with the Abu Dhabi pipeline (Habshan-Fujairah) with a capacity of ~1.8 million b/d.

Excluding Iranian flows (~2 million b/d), that leaves us with ~10 to ~12 million b/d at risk.

We’ve already had 6 days of disruptions. This amounts to ~60 to ~72 million bbls of crude + condensate + product. Production shut-in so far has been restricted to producers with no real storage capacity (Iraq).

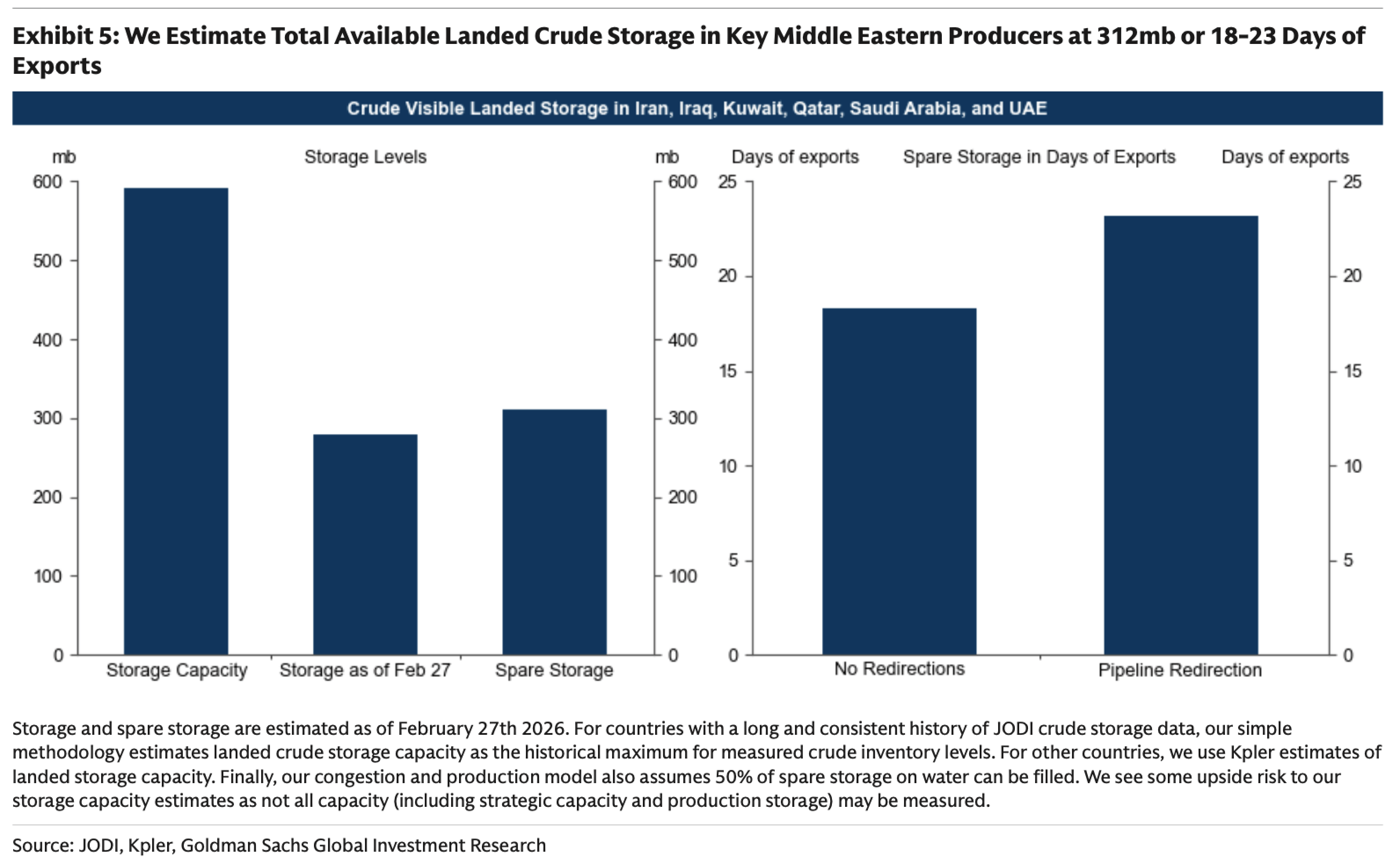

Goldman estimates that there are ~312 million bbls of capacity available. So we are still 2 weeks away from needing to shut in more production.

After storage capacity hits max capacity and if tanker flows remain restricted, that’s when we will see panic. Meanwhile, the global oil market is working through the excess crude on water and the surplus in storage that we have in 2025.

By our estimate, excess crude on water and excess onshore storage will be gone in 2-3 weeks. This is roughly the same timeline as the production shut-in scenario.

In other words, if we don’t see tanker activity pick up after 2 weeks, prepare for the worst-case scenario. For now, the oil market is absorbing the shock via the excess in storage. It won’t have much left after.

This is primarily the reason why we haven’t seen oil shoot past triple digits just yet.

In addition, as of the latest data, we have about ~100 million bbls of excess oil-on-water. By the end of this week, that surplus will have been eliminated.

Elevated OPEC+ crude exports in February will help in cushioning the loss in exports now, but that will run out by the end of this week as well.

From the onshore storage standpoint, excess crude in China will help cushion Chinese petroleum prices, but the US and others will show a rapid decline in onshore storage in the coming weeks. OECD oil inventories will fall below the 5-year average by the end of this month even with SPR release.

Can the oil market withstand $100+ prices in the near-term? Fundamentally, yes. We still have cushion for another 10 days or so, but if more production shut-in is announced, the oil market will price in the worse.