The situation with natural gas requires a lot more attention. As we have detailed in our reports, the oil market has some immediate cushion to supply any incoming gaps until the end of March:

Sanctioned oil-on-water

Global SPR release

Excess onshore oil inventories

For the oil market, the cushion runs out by the end of March, so chaos will ensue if tanker flows don’t return to normal by then.

But for the global natural gas market, Qatar’s outage will have a profound effect on everything from electricity to economic growth to heating. Qatar accounts for ~20% of global LNG supply, so every day it is not supplying the world, that’s 20% less LNG available. There’s no SPR to supplement Qatar. The only way out of this, eventually, is through demand destruction similar to the events we saw in 2022.

Structural Implications

Immediately after the Iranian conflict started, we wrote a piece titled, “A Fascinating Situation Is Unfolding In Natural Gas.” In it, we specifically detailed the geopolitical ramifications of the force majeure announced by Qatar:

But the geopolitical conflicts that unfolded over the weekend changed all that. In particular, the most notable event was Qatar announcing force majeure on its LNG gas exports. Qatar is the 3rd largest LNG exporter in the world. Most of its contracts are long-term. Qatar exported ~90% of its LNG capacity to Asia.

With LNG tanker rates spiking amidst the geopolitical turmoil, US LNG gas exports suddenly become the most attractive place to lock in long-term commitments.

Take a stepback and think about this for a moment. Elevated geopolitical conflicts in the Middle East have just demonstrated how vulnerable LNG flows can be. And since natural gas is a time-sensitive commodity (needed during the winter heating demand season), having an adequate supply on time is vital for the buyers.

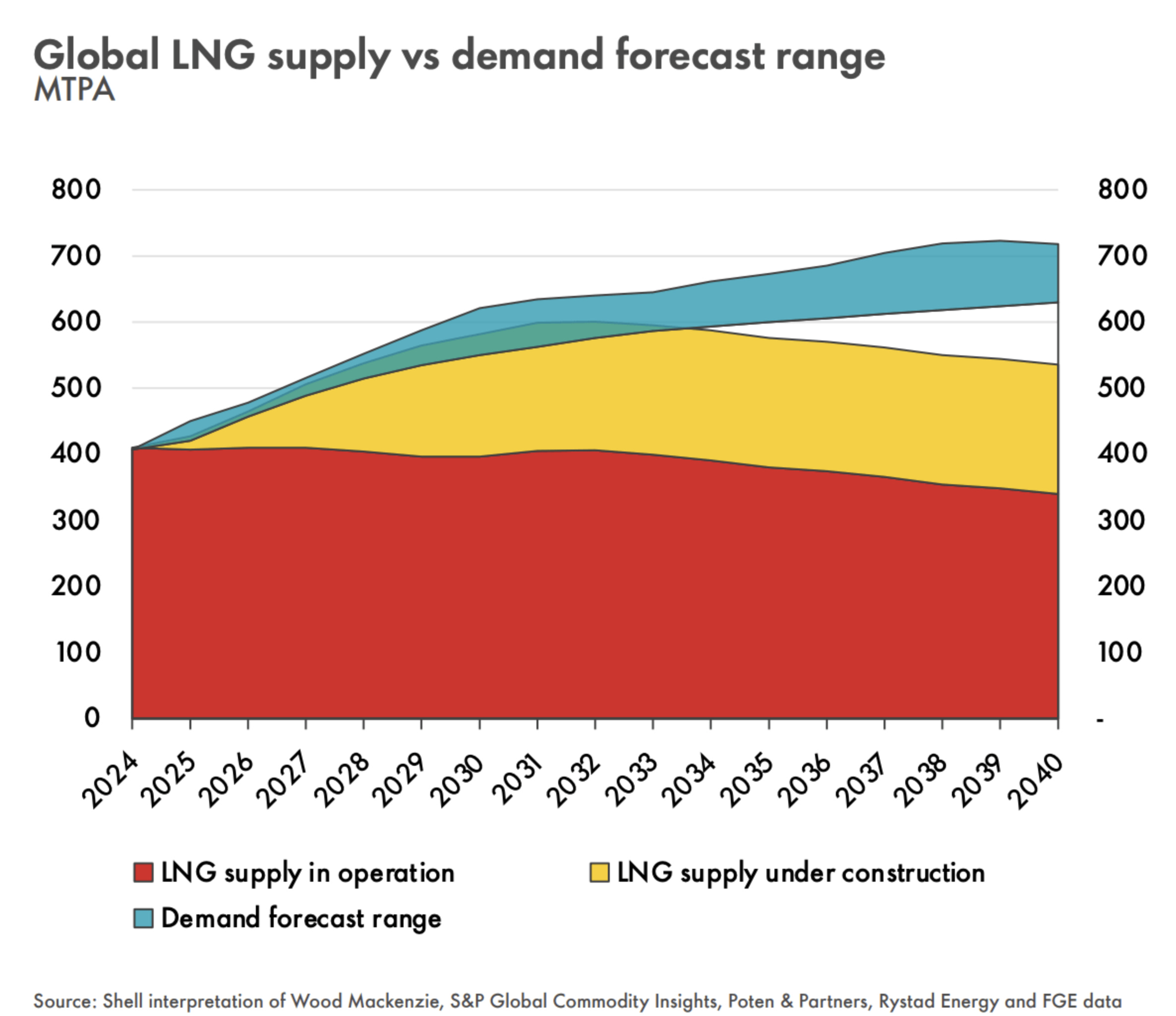

Everyone in the industry expected the global LNG market to be in surplus through 2030. Here was Shell’s 2025 LNG outlook:

As you can see, the demand forecast range varies as it depends on 1) weather, 2) price, and 3) adoption rate. Assuming everything goes perfectly, demand outpaces supplies by 2030. But if any of the steps meet a hurdle, we could see the global LNG market tip into a surplus, which would pressure prices.

Now, couple this outlook with the current anticipated LNG export demand increase in the US, and you can draw an interesting conclusion. Supply uncertainty in the Middle East will prompt buyers to want to lock in long-term contracts with US LNG exporters.

Source: S&P

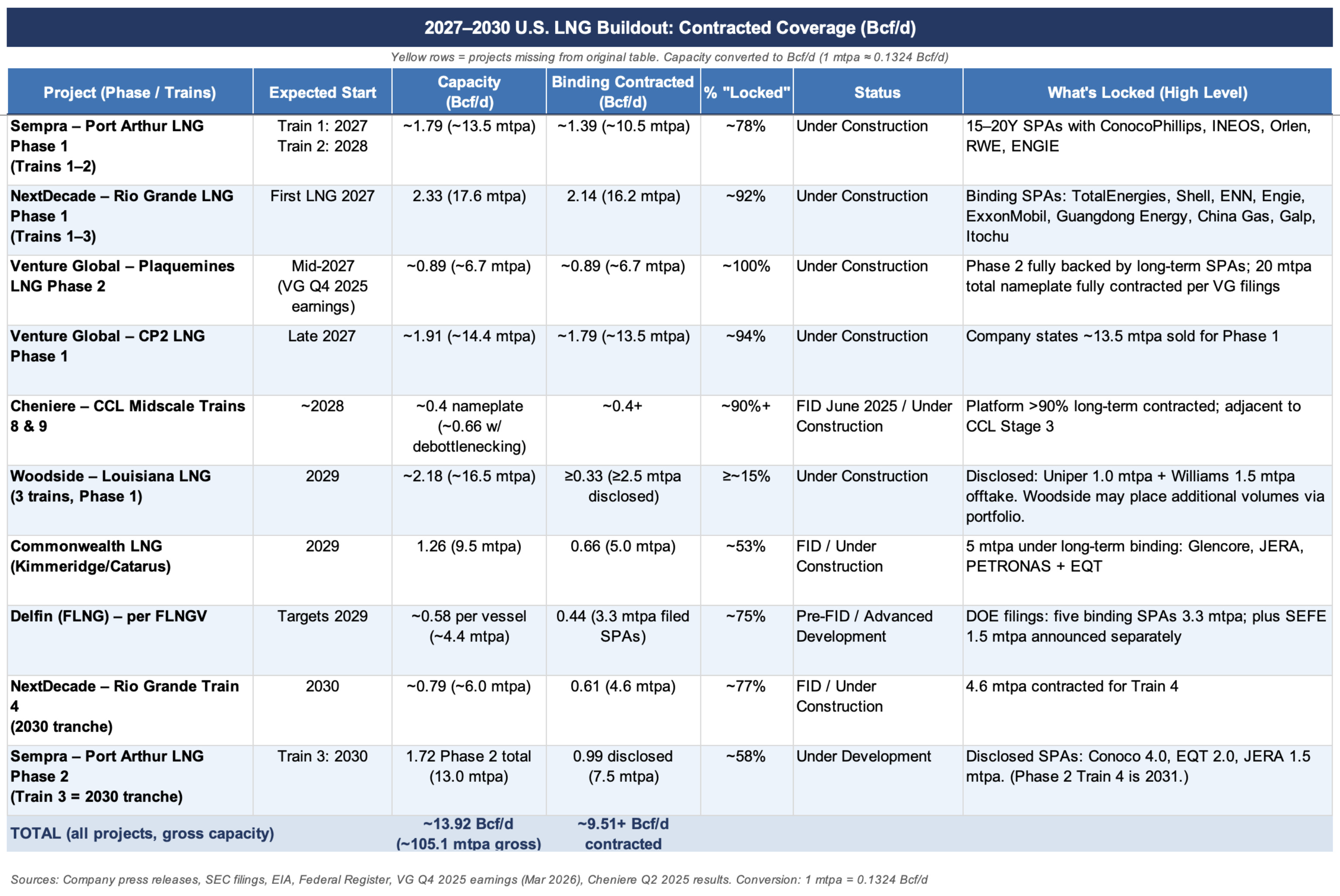

This insight was first brought to us by Dr. Anas Alhajji, whom we thank greatly for sharing this unique and differentiated take.

Between 2027 to 2030, only 68% of the incoming LNG facility buildout is contracted.

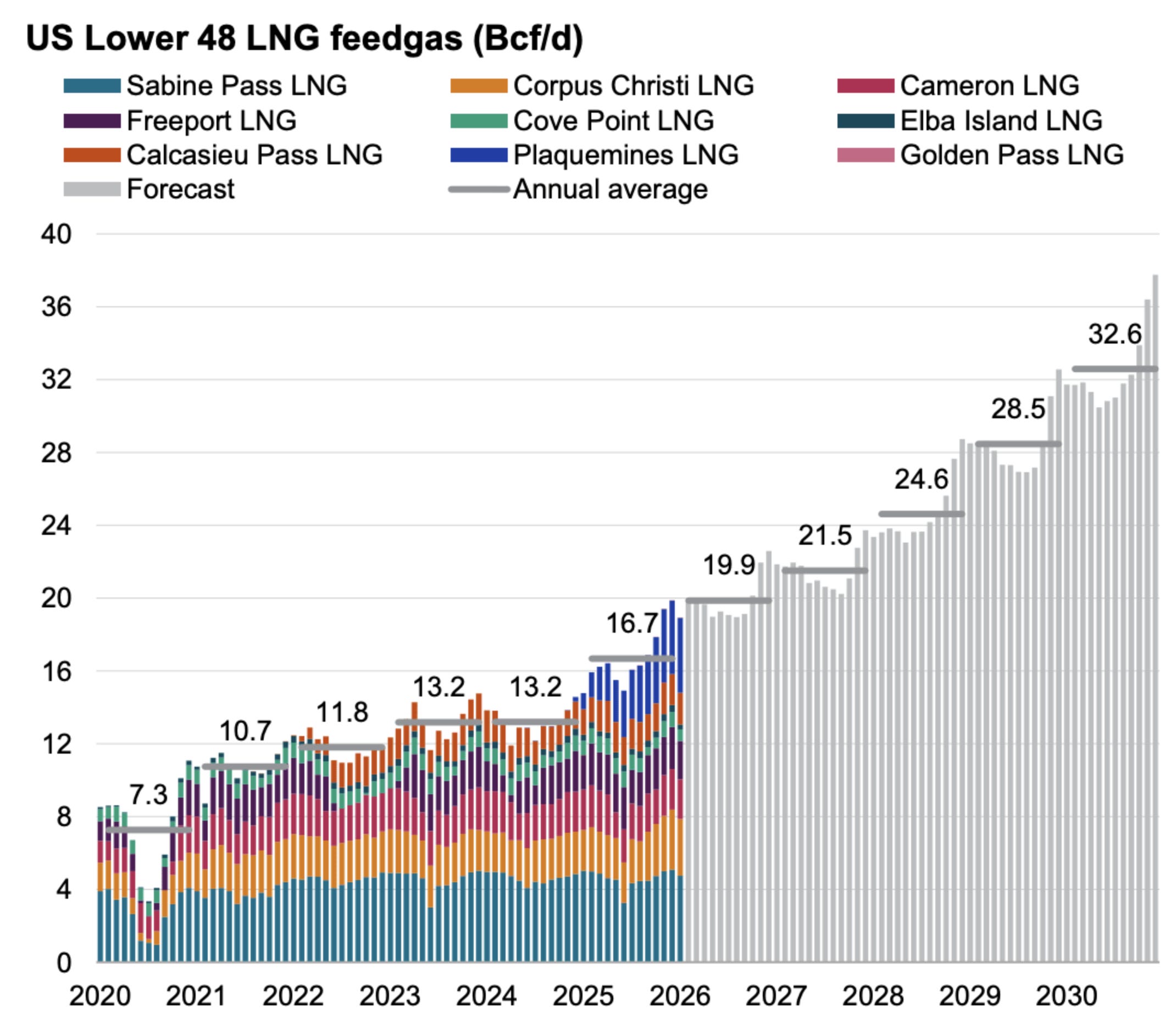

The increasing instability in the Middle East, especially if the conflicts are prolonged, will be very beneficial for US natural gas producers and exporters. The US is already the largest LNG exporter by far. US shale gas producers have some of the best economics in the industry. Not to mention that Permian, the key US shale oil region, is selling natural gas today below $0/MMBtu.

In our view, the Qatar force majeure will have altered the global LNG landscape for the years to come.

A major macro narrative heading into 2026 was that the global LNG market would be in surplus by 2027. New capacity increases from both the US and Qatar will push the market into a surplus, creating pricing pressure and potentially preventing new US LNG facilities from securing funding.

With each passing day that the Strait of Hormuz remains closed, the long-term structural implications grow stronger. The US is now the safest and most secure place to lock in long-term LNG commitments. Not only are US LNG exports price-competitive, but the geopolitical landscape has all but ensured that this structural tailwind will continue for years to come.

To put it bluntly, we have never ever seen a disruption of this scale or duration. For most energy analysts, the closing of the Strait of Hormuz was always a tail risk, but never a real risk. It’s never happened, so how can you account for that?

Well, it’s happening, and this will change how utilities and LNG buyers think about future contracts for years.