The 2020 oil market setup can teach us a lot about the framework for understanding the “extreme” nature of the oil market. Here’s a quick history lesson from someone who was in the middle of it.

Background

Many of you are familiar with the origin of the COVID virus, so I will not bore you with that. Instead, let me help you understand the oil market setup going into 2020.

At the start of Q4 2018, President Trump was set to announce sanctions on Iranian oil exports. By the end of September 2018, OPEC+’s Joint Ministerial Monitoring Committee (JMMC) met and said that there’s nothing more they can do to prevent Brent from surpassing $80. In particular, Saudi’s energy minister (at the time), Khalid Al-Falih, said:

Asked if prices were too high, he replied, “I cannot speak to prices because I do not directly influence prices. What I can directly influence is ensuring that markets are well supplied, and that we will do today.”

Two weeks later?

President Trump pulled his first “TACO” by announcing an exemption on the oil sanctions. Oil prices went into a freefall.

OPEC+ met in December 2018 and decided that it was time to reduce output again. After increasing output at the end of June 2018 at the request of President Trump, OPEC+ reversed course.

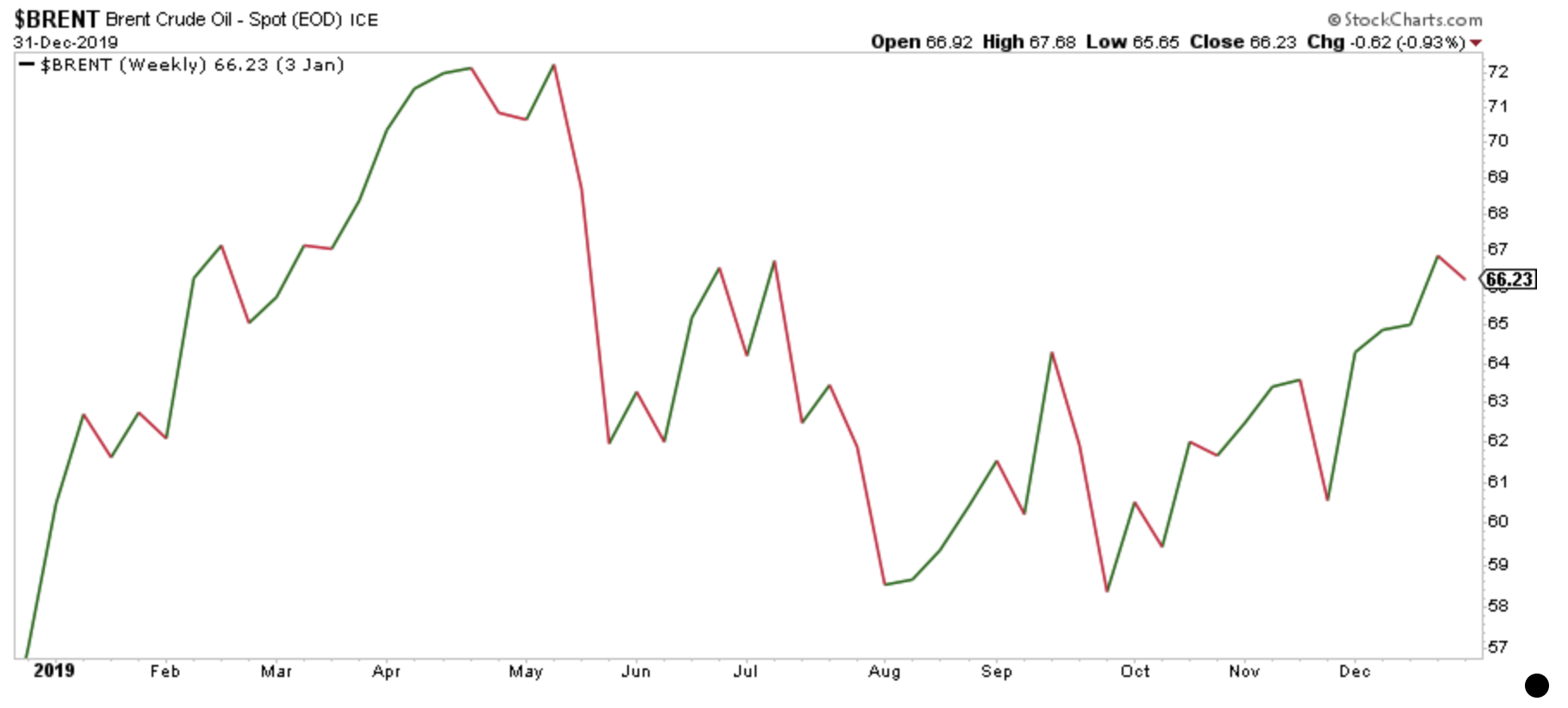

Throughout 2019, Brent traded in a tight range between $59 to $73.

The physical oil market was tightening with refining margins staying elevated. The market consensus was that the global oil demand outlook was uncertain due to the US/China trade war. Most analysts expected 2020 oil market balances to remain constructive, and US shale producers had just adopted the religion of spending within cash flow (after the 2018 spending spree).

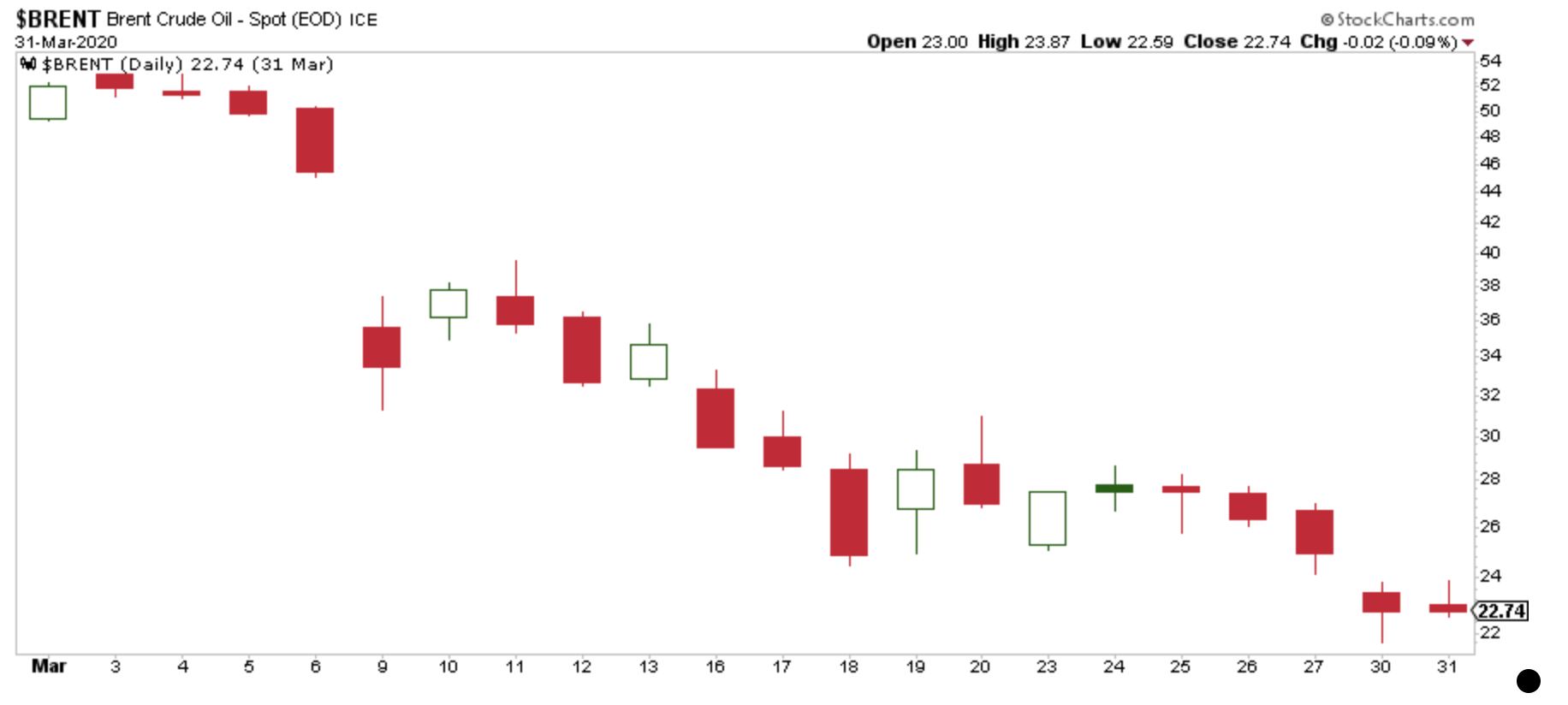

Coming into early 2020, oil market fundamentals were healthy. Inventory changes were slightly better than the seasonal norm. But by the end of January, the news of a mysterious virus was making headlines in mainstream media. Some very smart oil traders (we were not one of them) saw the Chinese government’s response (lockdown) and extrapolated it to the rest of the world. Pierre Andurand was one of them, and his fund made a killing shorting oil during the lockdown and bought the dip on the way up.

By early March, it was evident that OPEC+ had to meaningfully cut oil production to prevent the world from hitting storage tank tops. Global oil demand, at the time, was assumed to have fallen by at least ~3 to ~4 million b/d. OPEC+ had to cut production by at least that much. But in-fighting amongst the Russians and Saudis prevented a large production cut from taking place.

For some of us who have been in this sector for a long time, March 8, 2020, was one of the worst days in living memory. Saudis, in the middle of the pandemic lockdown, announced the most aggressive oil price war in history. Instead of cutting oil production by ~3 to ~4 million b/d, the Saudis turned on the taps and increased production to their maximum capacity. In addition, the Saudis announced record cuts to official selling prices in every region of the world. Europe saw the largest price cuts, as this hurts Russia the most.

Immediately after the announcement, oil prices went into a freefall.

During that time period, people fretted over the possibility that this oil price war would kill oil producers forever. The one part of the analysis that most analysts did not write about at the time was how realistic the duration was. We took a look at the economics and concluded that there was no way this would continue.

In addition, the Russians could not afford to produce at that price. Production shut-in was inevitable, and if that was the base case, agreeing to a product cut is the most obvious course.

Fast-forwarding 3 weeks later, on April 9, 2020, OPEC+ agreed to the largest production cut in history: 10 million b/d.

Funny side note: Mexico, a non-OPEC member, almost blew the deal apart because it did not want to cut oil production. It was going to show declining oil production even if Brent went to $80! I remember the frustration I felt at the time, reading the headlines coming out of the OPEC+ meeting. The good old days.

Was the oil market saved?

No, and this is where the history lesson is helpful in understanding the oil market today.

Relevance to the Oil Market Today

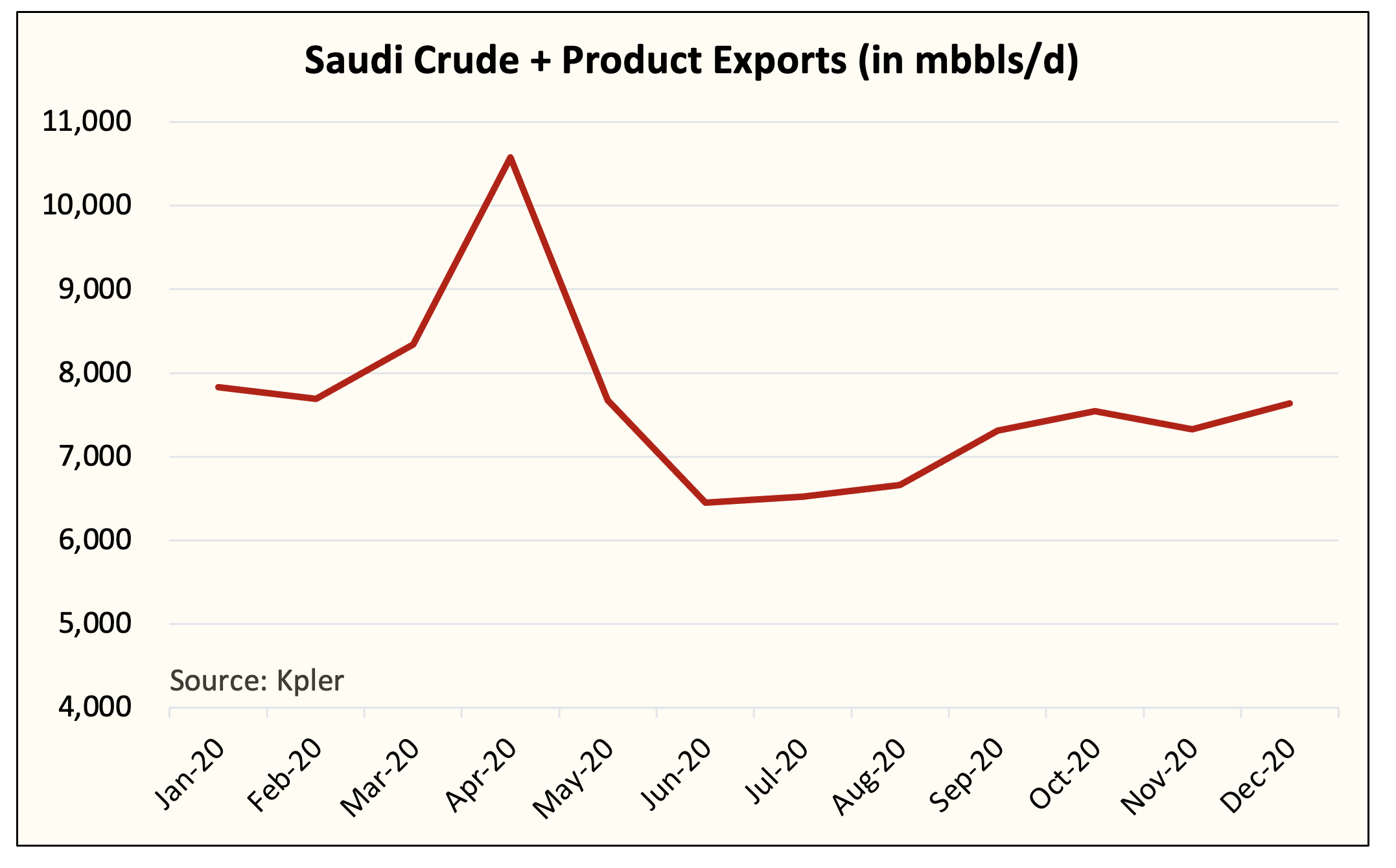

OPEC+’s production cut didn’t take effect until May 2020. The low oil prices at the time had already forced most OPEC+ producers to cut production. Saudis were the only exception at the time as total oil exports exceeded 10.5 million b/d!

The mismatch between elevated production and the demand drop from COVID-mandated lockdowns left the oil market in a temporary surplus of ~20 million b/d. And since the Saudis don’t start cutting oil production until May, April was going to be a brutal month.

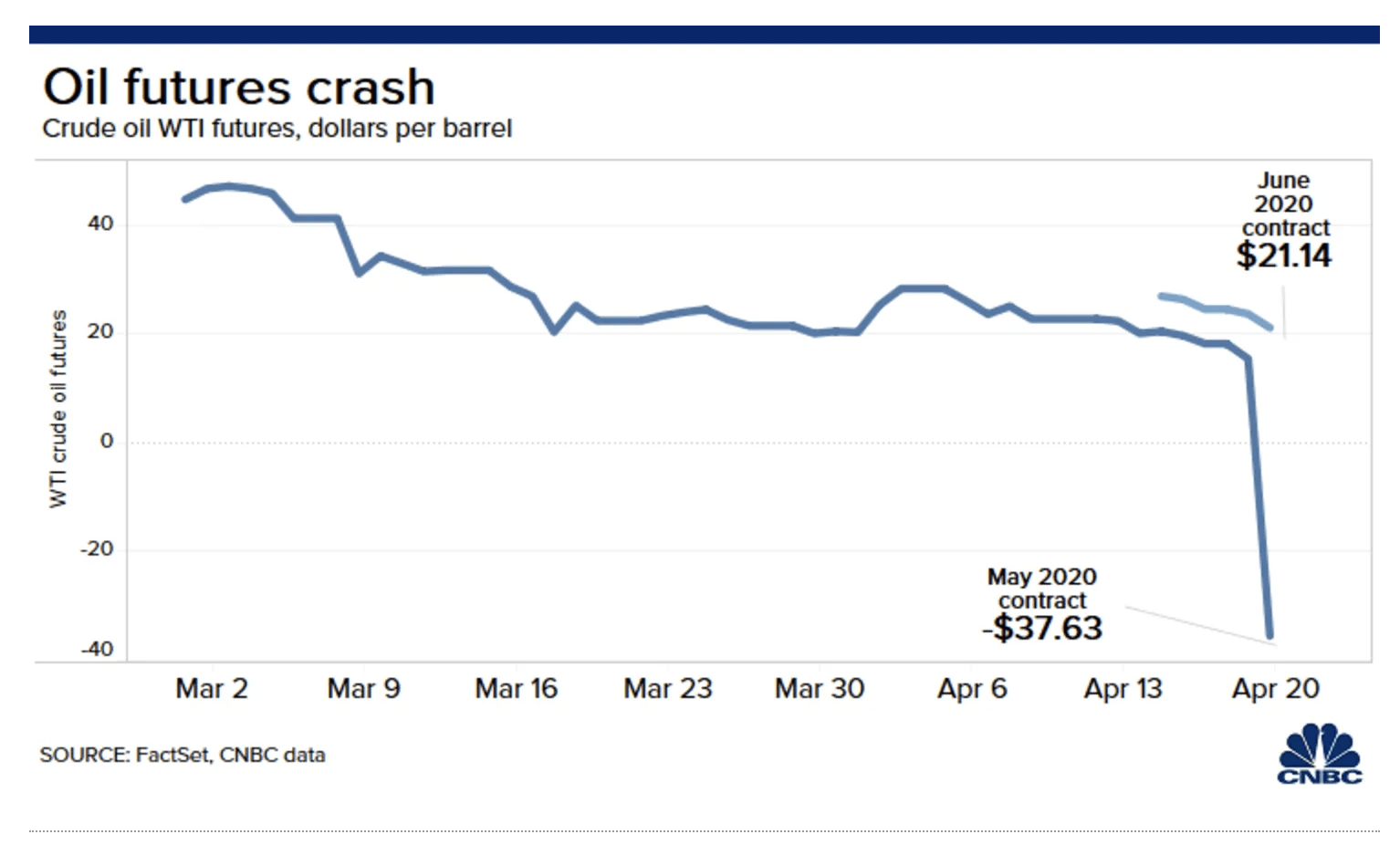

Sell-side analysts started estimating how quickly the world would hit tanktop in oil storage. Will the super contango we see in the oil curve push floating storage on tankers to an all-time high? Will VLCC rates 5x?

The narrative started to gain momentum. Couple that with real-time data showing a massive jump in oil inventory, and the world started pricing near-term oil futures as if tanktop were a reality. We all know what happened next: oil prices went negative.

Source: CNBC

What is the relevance to the oil market today?

Strait of Hormuz tanker flow remains low. Yes, we are seeing tankers go through with AIS turned off, but the flows remain a fraction of what they were before the conflict started.

Despite the whipsaw in the oil market today, history tells us this is not the end of the price move. Amid COVID, OPEC+’s historic intervention was unable to prevent a further collapse in oil prices.

This time is the reverse.

With each passing day that goes by without tanker flows returning to normal, Gulf Coast Countries (Iraq, UAE, Kuwait, Qatar, Saudi) will see onshore inventories build. Once storage reaches capacity, production will be shut in. (Note: This is already happening with Argus estimating production shut-in between 6.2-6.9 million b/d.)

Simultaneously, global oil inventories will begin to decline by ~11 million b/d. We are currently absorbing the excess we have on water, but once that’s gone, visible oil inventories will show a rapid decline.

Similarly, even if tanker flows return to normal by tomorrow, the production shut-in situation will take weeks to return to normal. Every day that goes by, the situation worsens.

So was $119 the peak?

I don’t know. But if history is any guide, we will reach an obvious extreme before this ends. Don’t rule out another price spike in the making. Remember, the oil market only had 2 weeks of cushion. If tanker flows don’t return to normal by the end of this week, I fear the worst has yet to come.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO Call Spreads either through stock ownership, options, or other derivatives.

I think we are over $100 tomorrow. I really hope Iran is not mining the Strait. That would just be a disaster all around.

If oil production is only down 6 million barrels per day, why will inventories decline by 11 million barrels per day? I'm a little confused. Thank you.