The US and Israel launched a joint attack on Iran this weekend. The key highlights are below:

Iran’s Supreme Leader Ayatollah Ali Khamenei was killed.

Multiple top leadership positions in the Iranian regime have also been eliminated. President Trump noted that “Operation Epic Fury” was so successful that the replacement candidates were also killed.

Iran responded by attacking Israel, US bases, and Gulf Nations, including Qatar, the UAE, Kuwait, Bahrain, Jordan, Saudi Arabia, Iraq, and Oman.

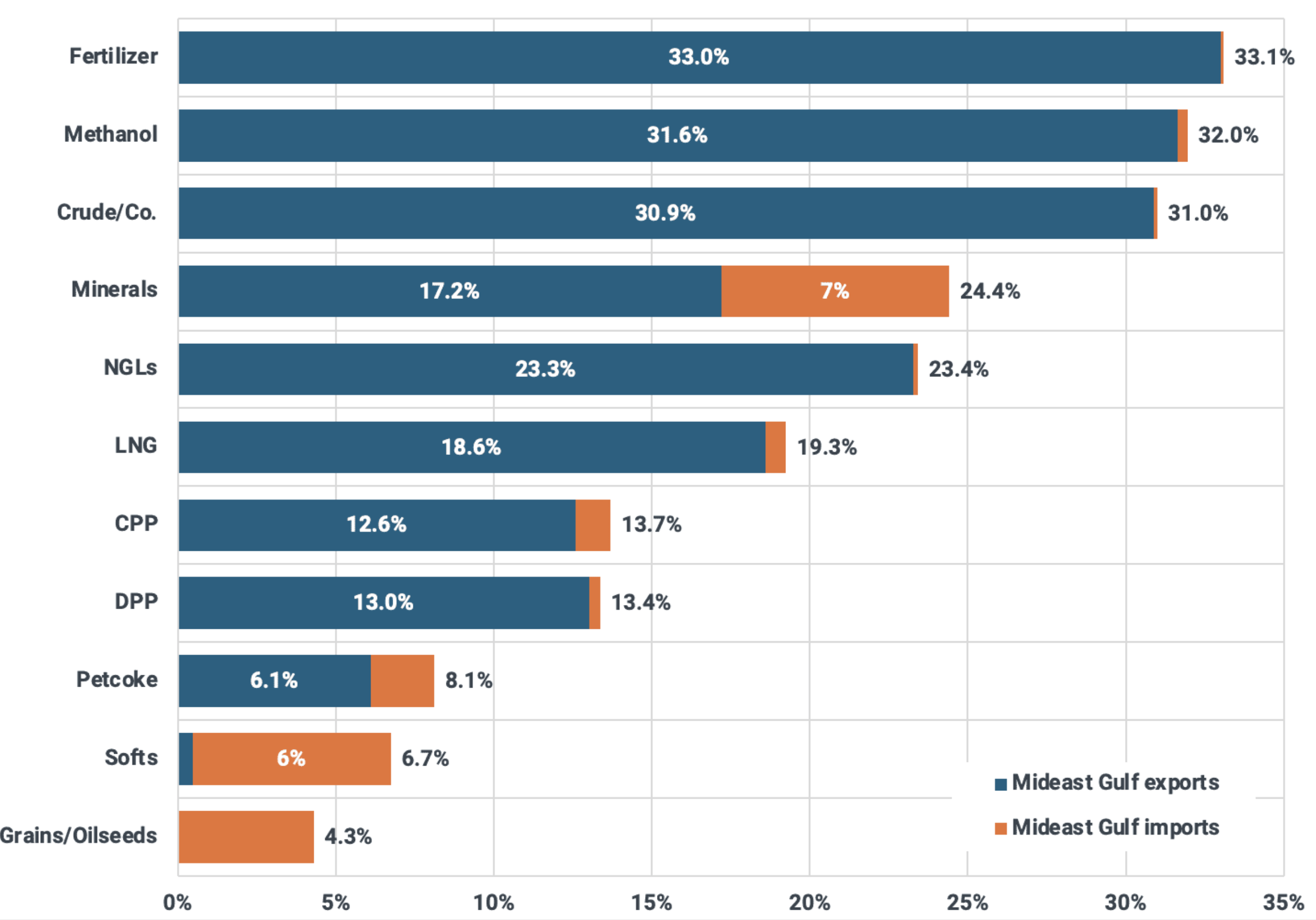

Marine insurers began cancelling existing war risk policies for vessels in the Gulf and Strait of Hormuz over the weekend. In Kpler’s blog post update, it noted that while the Strait of Hormuz isn’t technically closed, the lack of insurance has slowed tanker traffic. This has major implications for global commodity flows:

Source: Kpler, Matt Smith

Only Answering The Questions We Know The Answers To

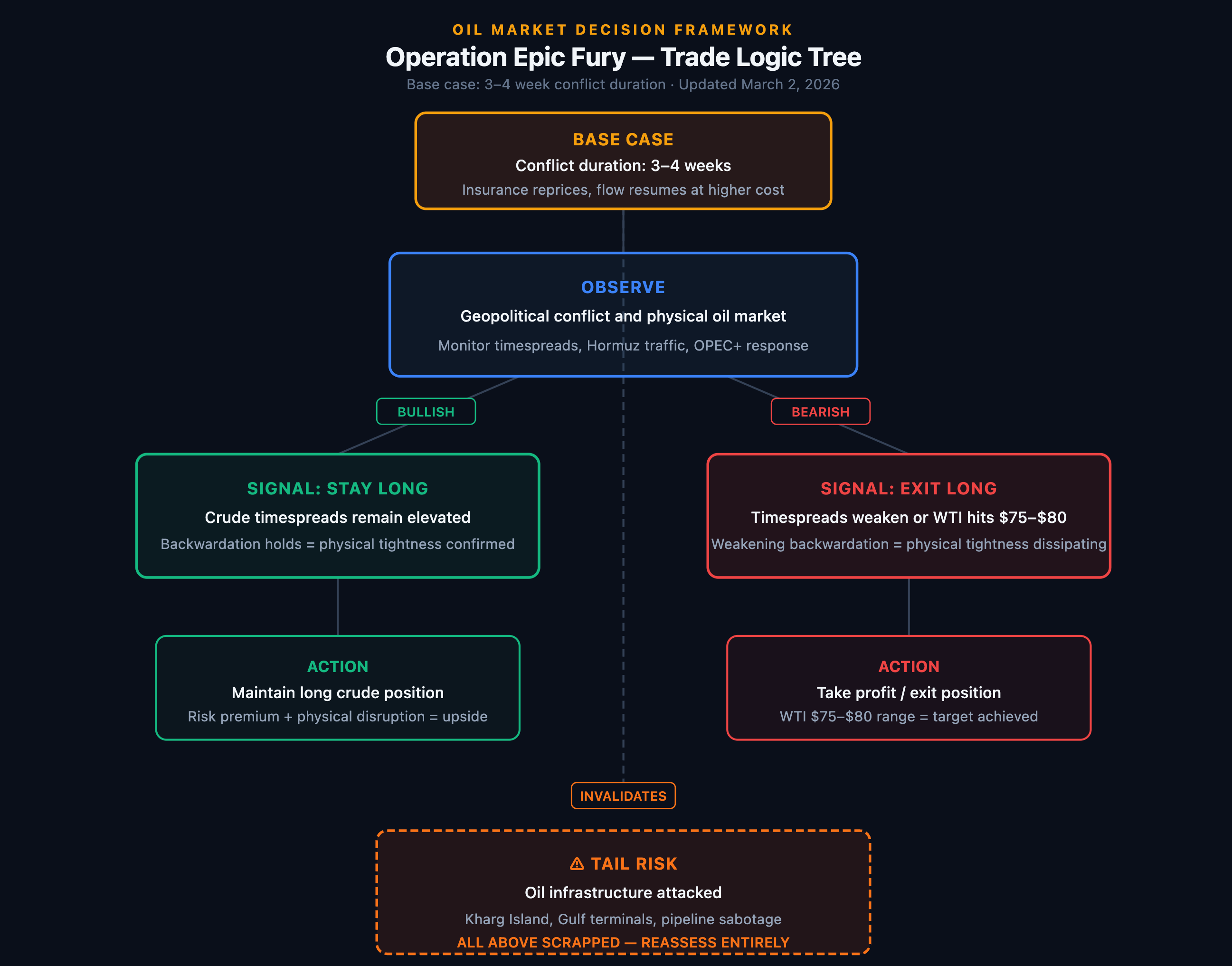

Updated on March 2nd, below is my gameplan:

I’m not a geopolitical expert, and I won’t pretend to be one. The reality is that many of us have no idea what to expect between the US, Israel, and Iran. We can only answer the questions we know the answer to, so instead, I will write the following section in an interview format.

How long will the US, Israel, Iran conflict last?

I have no idea.

How does this impact global energy trade flow?

If we don’t know how long this conflict will last, we have no way of knowing the impact on the trade flow. One can use an estimate for the duration of the conflict, but this framework will not provide any value because it’s just pure speculation.

Where should oil trade without geopolitical conflicts?

$59-$62

By H2 2026, we see WTI trading in the $65 to $70/bbl range.

Geopolitical risk premium today (with WTI at $70 is about $8 to $11/bbl).

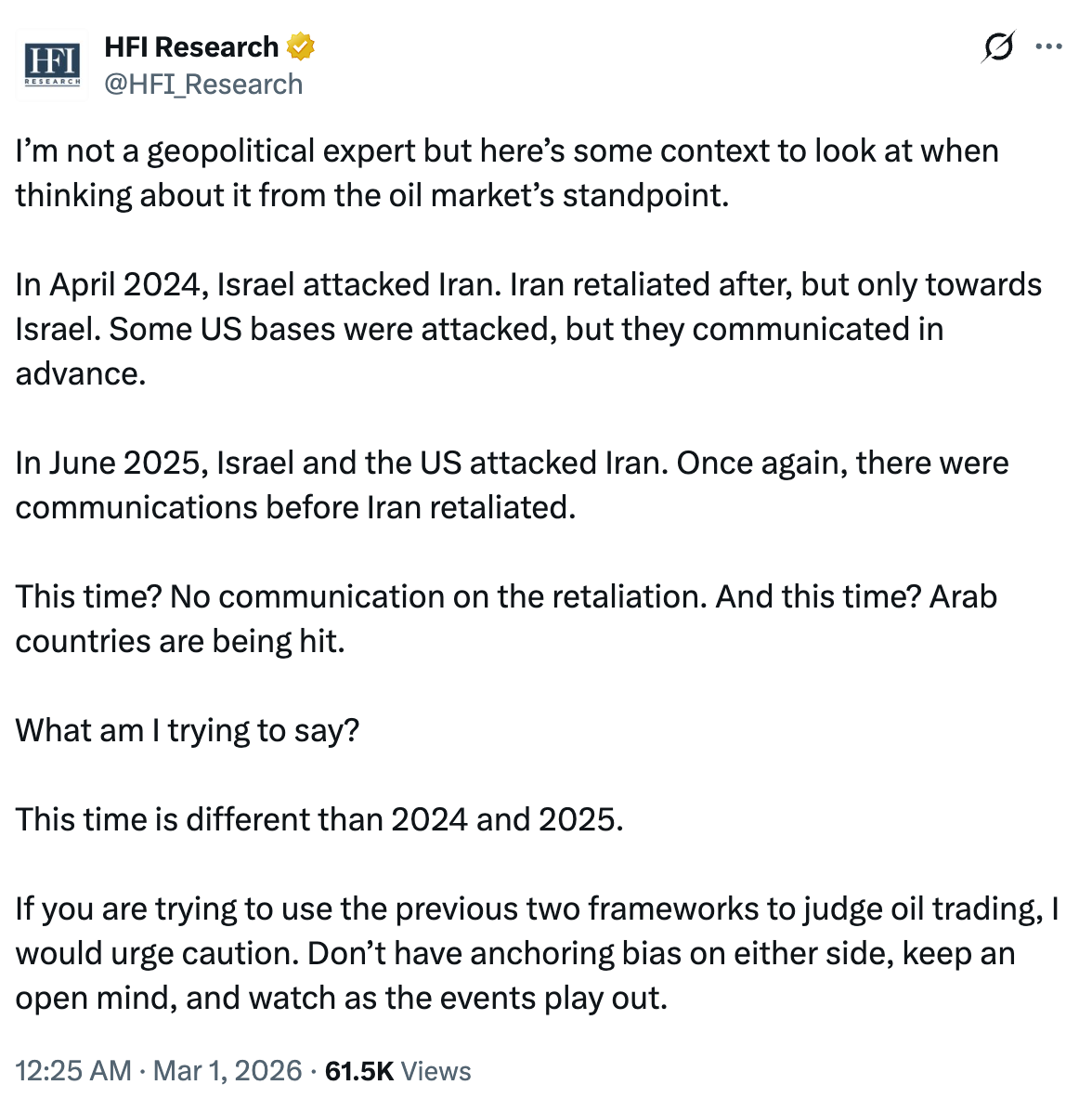

From your experience, does the current conflict match the ones you’ve seen in the past?

Over the weekend, I wrote a post on X as follows:

My gut hunch is that this time feels different. Iran’s Supreme Leader just died. The remaining Iranian leadership has already seen what it looks like to be negotiating with the Trump administration. Sources on the ground from the previous week were indicating that a peace deal was close, only to have Israel and the US take out the leaders over the weekend. Even from a diplomatic standpoint, it seems hard to justify further negotiations. But that’s just my gut hunch, and I have no facts to back this.

How would you trade your current long oil position?

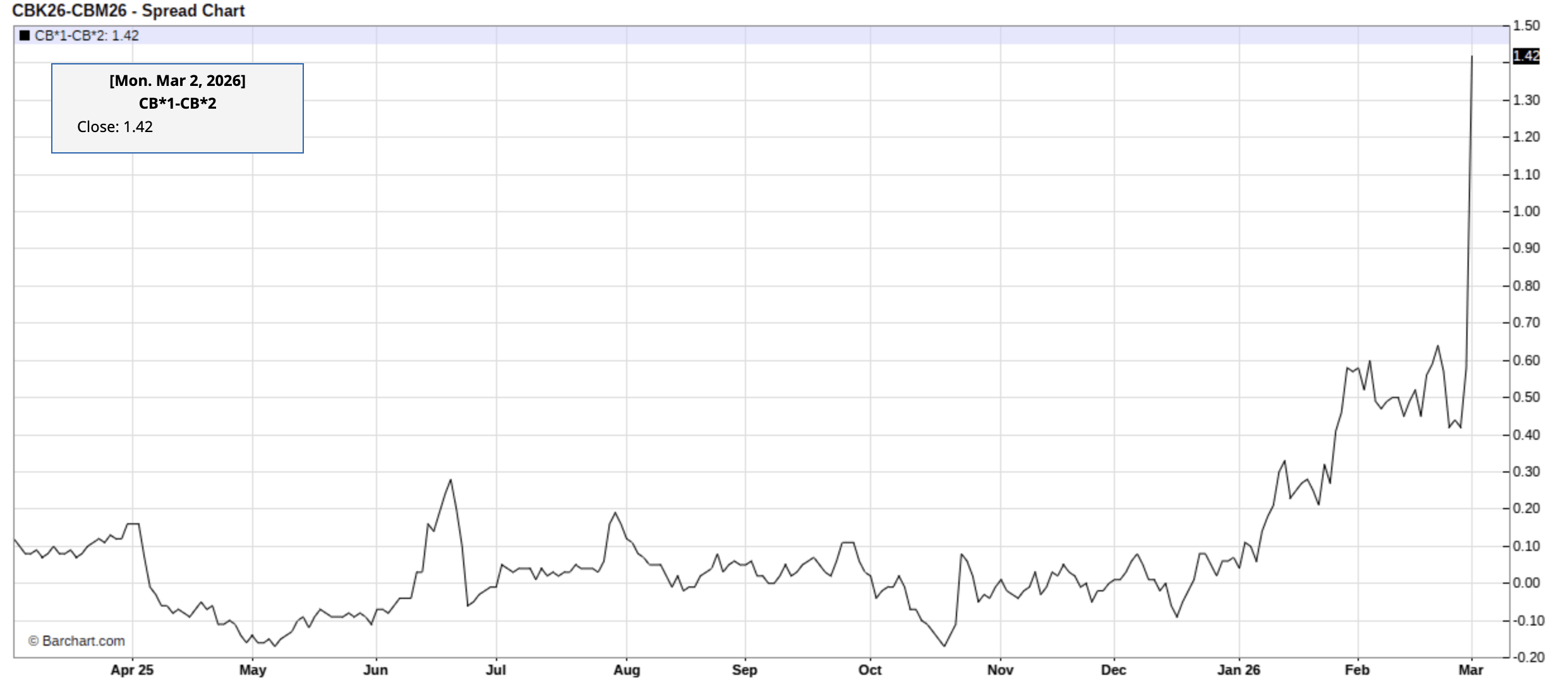

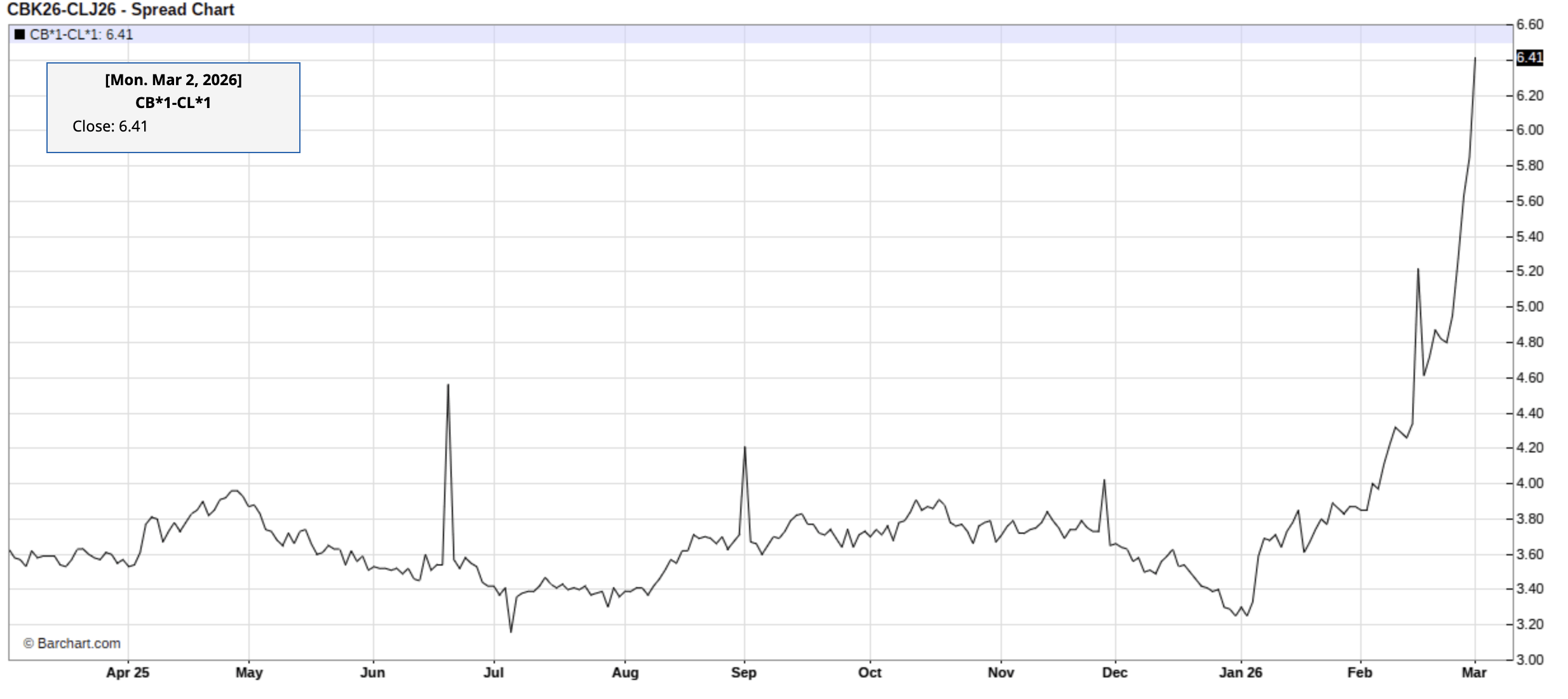

I’m paying attention to the physical oil market moves more than anything else. Historically, the peak has always coincided with some dramatic move happening in the spreads. As you can see, the Brent 1-2 timespread is spiking, which is perfectly sensible. Meanwhile, the Brent-WTI spread is also spiking, indicating that traders are trying to pull the barrels out of the US.

Brent 1-2

Brent-WTI

I’m long USO with a cost basis of $73.56. I think the risk/reward for a long position becomes unfavorable if WTI reaches $75/bbl. We are not far from there with WTI trading at $71.50.

My gameplan is to monitor both the physical oil market and the geopolitical development. Again, there’s no way of knowing when the conflict will end. If WTI gets to $75/bbl, I will look to exit.

Would you short oil after closing your long position?

No. Because the geopolitical side is very hard to predict, it’s best to take no action.

What do you make of the OPEC+ production increase over the weekend?

OPEC+, excluding Saudi and the UAE are already producing near max as I wrote in this article.

I think the production increase is more symbolic than anything else. Saudi, on the other hand, is fully capable of increasing exports to fill any gaps left behind by Iran or others. If Brent continues to move higher, we should see Saudi crude exports jump.

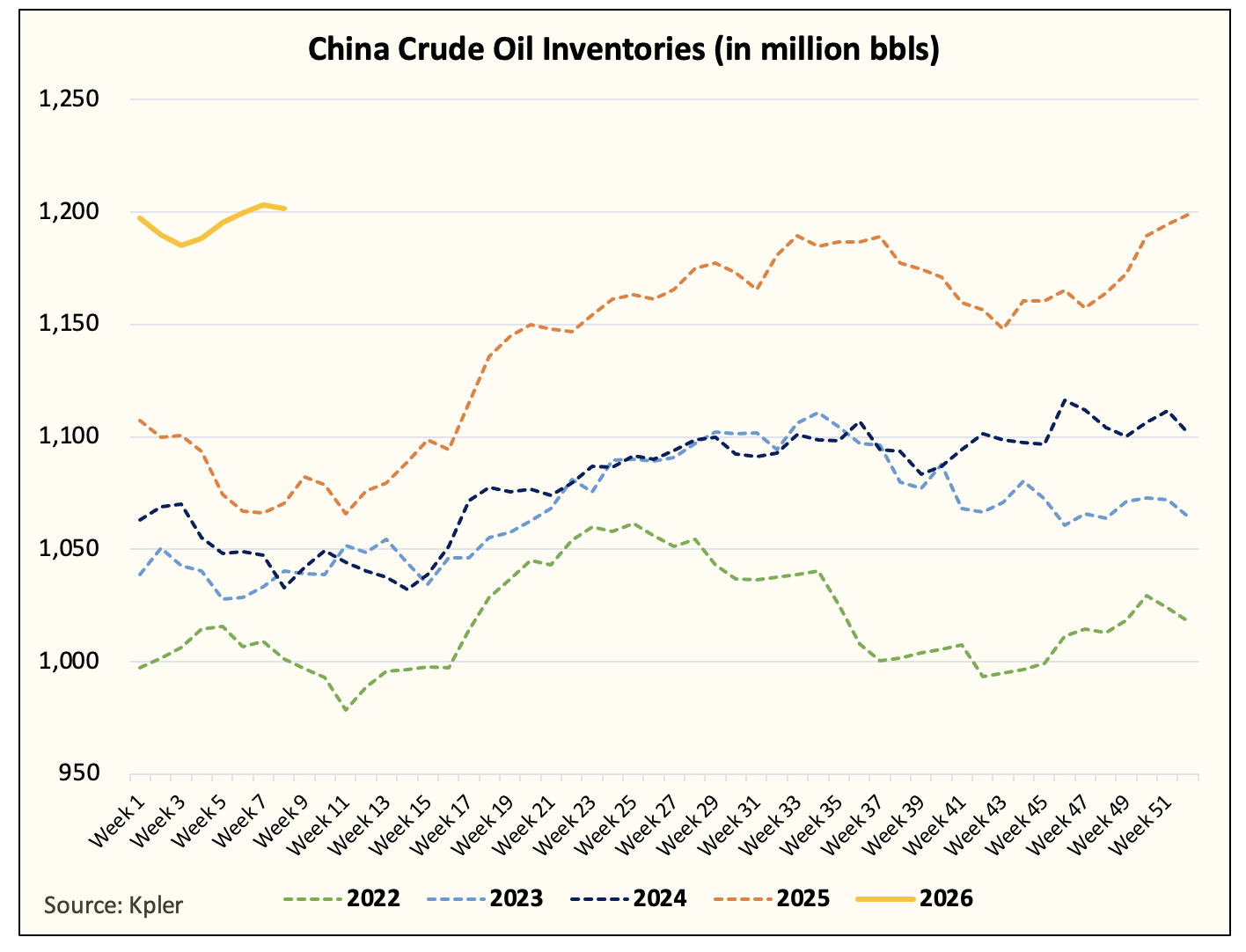

What about China?

China’s crude buying will slow with oil prices where they are today. The excess build-up we saw throughout 2025 will be used to replace some of the demand this year. One of the key tailwinds for this year’s oil market balance was China’s SPR buying, so higher oil prices will reverse this tailwind into a headwind.

In addition, China will start importing more Russian crude following the disruptions we are seeing in the Strait of Hormuz. We could see a meaningful drop in oil-on-water as this gets absorbed onshore.

Again, higher oil prices will just slow China’s crude buying, which is in itself a headwind.

What about natural gas?

A lengthened conflict that disrupts shipping flow in the Strait of Hormuz will boost global LNG prices. This will, in turn, boost demand for US LNG exports, which will push Henry Hub prices higher. It won’t be a 1:1 impact, but the higher demand will be nice considering that the first half of March is expected to be one of the warmest since 2000.

Now, if the weather starts to moderate as I’m seeing now, I expect natural gas prices to recover back to $3.5/MMBtu. A big driver of US natural gas prices will still be dependent on the weather, so geopolitical conflicts or not, the market will remain fixated on fundamentals in the US.

Do you think energy stocks will move higher?

In general, when oil and natural gas prices rally, energy stocks follow. But since it’s geopolitically driven, energy stocks don’t usually follow it 1-to-1. The main reason is that no one buys energy stocks because of a temporary bump in price. We would have to see a sizable change in the futures curve before valuation multiples rerate. And at the moment, a lot of energy stocks are ahead of fundamentals, so it’s more likely we see them take a breather.

What’s the takeaway for readers?

No one knows how long the conflict will be. But just know the following:

Iran is already producing at max capacity (~3.55 million b/d of crude). Any disruption is asymmetric to the downside for supplies.

Fundamentally, WTI should be trading near $60/bbl, but we are already trading at $71.50. The risk/reward becomes unfavorable if WTI gets close to $75/bbl. That’s the level where we will take profit on our USO long.

If we exit our oil long (not exiting energy stocks here, we are bullish long-term), we are not going to short oil. Geopolitical risks are too uncertain and too unpredictable.

Prolonged conflict will be bullish for natural gas as global LNG prices move higher. Henry Hub pricing will still be predominantly influenced by US gas fundamentals, but higher LNG demand will be a small tailwind.

OPEC+ supply increase for April is more symbolic than something material. Saudi has the spare capacity to meet any supply shortfall in the near-term (to an extent). If you really want to know what OPEC+ is doing, just watch Saudi oil exports.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO, BOIL either through stock ownership, options, or other derivatives.