Editor’s Note: This article was first published to paying subscribers on Dec 11, 2024. We are reposting the article without any changes. Here’s the link to the original article:

The Out Of Touch Oil Market Will Meet Reality Soon

Elevated OPEC+ spare capacity, peak Chinese oil demand, extreme supply surplus in 2025, OPEC+ disunity, and whatever else people are saying to themselves to believe oil prices will crash lower, I've heard it all this year.

Enjoy.

Dec 11, 2024

Elevated OPEC+ spare capacity, peak Chinese oil demand, extreme supply surplus in 2025, OPEC+ disunity, and whatever else people are saying to themselves to believe oil prices will crash lower, I've heard it all this year.

In particular, one of the best arguments I've seen pertains to the material growth we are going to see in US oil production.

Spoiler alert: It's not happening.

On August 9, we published our report titled, "US Oil Production Slowdown Is Real." We said:

Why this matters...

One of our key variant perceptions coming into 2024 was that people overestimated the production growth we saw from shale in 2023. The main culprit for this is from EIA's production reporting change. Following the June 2023 introduction of "transfers to crude oil supply," EIA purposely increased US oil production in an attempt to eliminate the dreaded "adjustment" figure. The reality is that US oil production was meaningfully higher at the end of 2022 (please see our real-time graph for the spike into the end of 2022).

So while headline growth showed +1 million b/d, the reality was closer to +250k b/d to +300k b/d. This, in turn, resulted in overly optimistic US shale oil production growth assumptions into the end of 2024 and 2025.

As a result, most oil analysts are overstating non-OPEC supply figures in 2025, which is pushing them toward the bearish side.

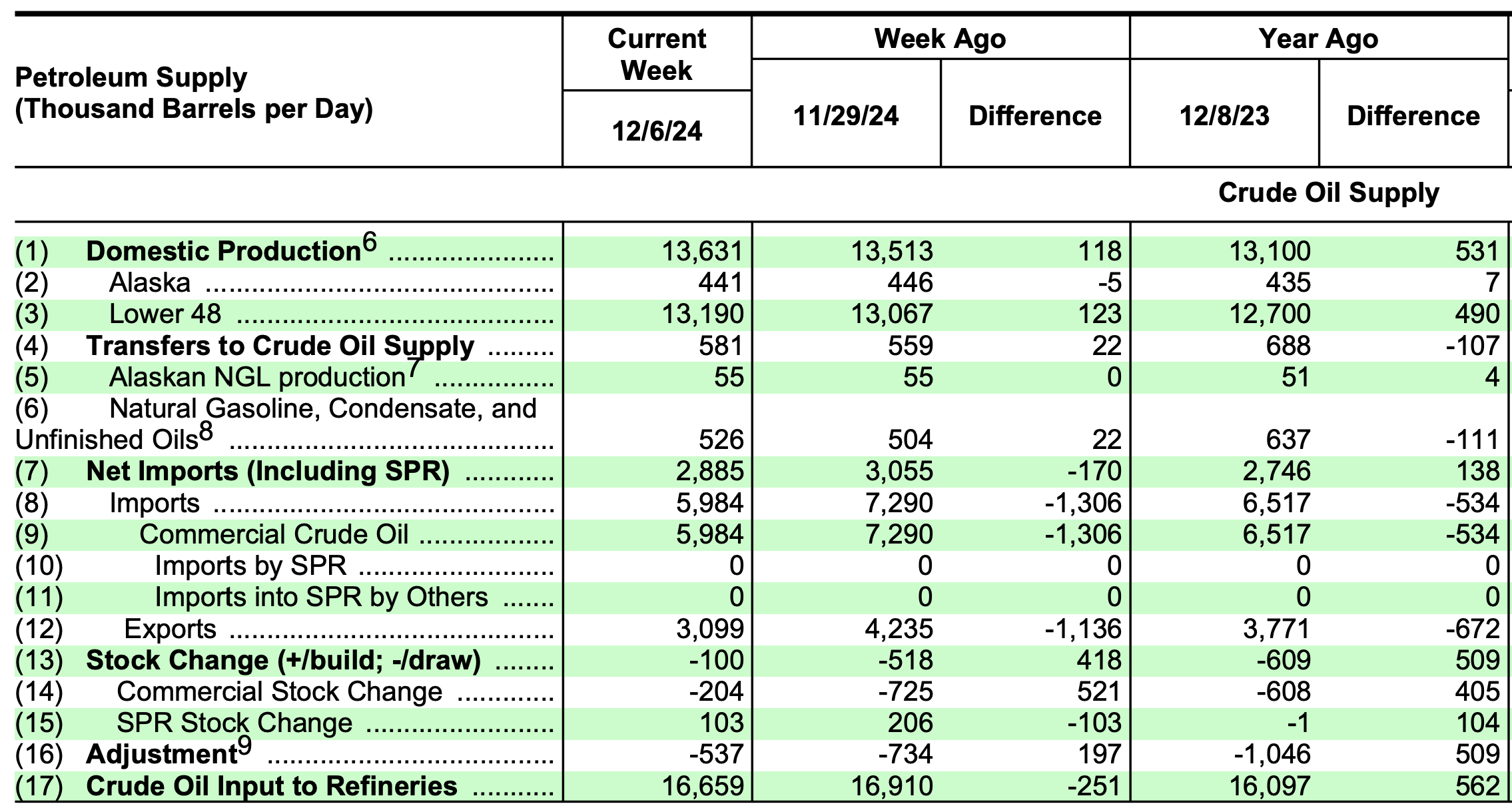

Fast forwarding to today, real-time data is showing US oil production disappointing to the downside, while headline EIA US oil production figures hit an all-time high of ~13.63 million b/d.

Once again, the people unaware of the data are being fooled into believing that US oil production is ramping higher.

While EIA does a great job of disclosing its methodology change and the associated variable changes, people do not pay attention to details, and this week's production increase is simply to match the change in EIA's short-term energy outlook or STEO.

Source: EIA

In fact, more often than not, I have to point out to people that the weekly US oil production figures published by the EIA are not "real" and instead a modeled figure from the STEO. The STEO is just EIA analyst assumptions and has no basis in reality.

Source: EIA

And even for those keenly aware of the data, they only go as far as using the "adjustment" figure to account for the implied difference in US crude balance. But even this method fails to account for the real underlying US oil production trend.

Why?

Because US crude exports are based on customs data. And the EIA explains that there will be differences in timing due to reported customs figures and real exports. This delta is the main reason why finalized crude export figures (from the EIA PSM) are different than what the EIA weekly reporting is.

Such trivial, yet important differences, are why the oil market has more questions than answers. But for people like me who've followed the data this closely for a decade, none of this is a surprise.

So when I say that this oil market is out of touch, it really is. And one of the biggest out-of-touch things with regards to the oil market is the idea that US oil production is ramping.

By my estimate, US crude production today is around ~13.25 million b/d to ~13.3 million b/d. This is flat y-o-y. In October and November, we saw an increase in US oil production, but December is expected to show a drop.

Even if we assume that this week's EIA data was an anomaly, the implied US oil production figure fell to ~12.2 million b/d, which will be hard to reverse back higher. I don't think this is where US oil production is, but the fact that it disappointed that much implies to me that there's no "exit production growth", which is important to understand if you are modeling into 2025.

Outlook for 2025

Why is December important?

Q4, in general, is a very important quarter for US shale producers. All producers weigh capex in the 2nd half of the year due to seasonality and cheaper servicing pricing during the summer. Adverse weather effects also force operators to spend the bulk of their capex in Q3. This is why Q4 production is the most important because of the capex spent in Q3.

Historically, US oil production has always ramped into year-end. We saw this evidence clearly throughout the Shale Revolution. This time around, we did not see the meaningful move higher. In fact, one can argue that with Matterhorn coming online, Permian oil production growth has so far disappointed expectations.

At ~13.3 million b/d exit, Q1 US oil production will fall down to ~13.1 million b/d again. The decline is the result of flush production decline from Q4 and lower drilling and completion activities in Q1.

In terms of capex, we would have to see a ~15% to ~20% increase in producer spending in 2025 for us to push US oil production to ~13.65 million b/d. Without this capex spending increase, it will be extremely difficult to achieve this production level.

Out of all the major US shale producers, only Occidental and Exxon will be meaningfully increasing production in 2025. And even in those growth scenarios, Occidental will grow ~50k b/d and Exxon will grow ~75k b/d (all liquids).

This combined with natural declines from other producers could result in US oil production being flat y-o-y.

Looking at analyst expectations, most of them are still expecting Q2 2025 balances to show ~13.65 million b/d in US crude production. The reality will be closer to ~13.3 million b/d, which would put the delta at -350k b/d. This delta coupled with the disappointing Brazilian production growth could put the non-OPEC gap at ~650k b/d.

This huge gap will allow OPEC+ to increase production starting in Q2 2025. With the OPEC+ agreement allowing producers to slowly phase in production into 2026, the impact to the oil market will be negligible and one of the biggest ceilings on the oil market will be gradually lifted (OPEC+ spare capacity).

Meeting Reality Soon

Persistent bearishness in the oil market as it pertains to the surplus expected in 2025 will meet reality soon. With US oil production disappointing to the downside, oil market balances will be closer to neutral for Q1 2025 versus the +1.4 million b/d expected by the market.

If US oil inventories fail to build in Q1, the market will change its tone rapidly, and oil prices will re-rate to storage implied prices. Concerns over spare capacity will remain, so readers should expect a $7 to $8 discount. WTI should trade in the mid to high $70s allowing producers to profit.

At this price range, global oil demand should continue to recover, while non-OPEC supplies peak.

Frustrating

For energy investors, I can't imagine a more stressful period than the one we are seeing today. Fartcoin has a market cap of $400 million and Tesla is up ~69% for the year hitting $420 per share. Everything feels like it's fake and made up, and value investing has completely gone out of favor.

But I think it's during times like these that you have to really stay focused on the things that are important. Regretting and looking back at the decisions you could've made doesn't do you any favors. Only by improving your process and looking forward to how you can get better will you find peace and clarity in the mind.

I think it's okay to be frustrated, but don't let your emotions dictate your rational thinking. Be mentally strong and focus on the important stuff. Stay true to the process.

At the end of the day, reality will matter again. It might not feel like it will anytime soon, but the rubber always meets the road.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.