I feel like I'm screaming into the void. The data I'm seeing and the narrative I'm reading do not match. In fact, the divide between data and reality is so far apart now, that the bulls and bears are at two extremes.

In particular, the disconnect between perception and reality is best captured by this chart:

Source: IEA

In its latest oil market report, IEA is so confident that oil market balances will be in the surplus that it said:

The decision by OPEC+ to delay the unwinding of its additional voluntary production cuts by another three months and extend the ramp-up period by nine months through September 2026 has materially reduced the potential supply overhang that was set to emerge next year. Even so, persistent overproduction from some OPEC+ members, robust supply growth from non-OPEC+ countries and relatively modest global oil demand growth leaves the market looking comfortably supplied in 2025.

It further added the following:

On that basis, our current market balances still indicate a 950 kb/d supply overhang in 2025. If OPEC+ does begin unwinding the voluntary cuts from the end of March 2025, this overhang would rise to 1.4 mb/d. A key uncertainty for the trajectory of OPEC+ crude supply remains the level of compliance with agreed targets, with our estimates showing collective output 680 kb/d above targets in November.

I want you to take a step back and read that again. IEA expects +950k b/d of surplus in 2025. This is one of the larger surpluses since the oil crash started in 2014.

In fact, if you go back and read all of IEA's oil market reports since 2014, aside from the COVID demand destruction, IEA hasn't forecasted a surplus this large since the end of 2014.

Source: IEA

The large surplus going into 2015 resulted from the oil price war the Saudis started in Nov 2014. As a result, the surplus was explainable, and the physical market showed obvious signs that a surplus was coming.

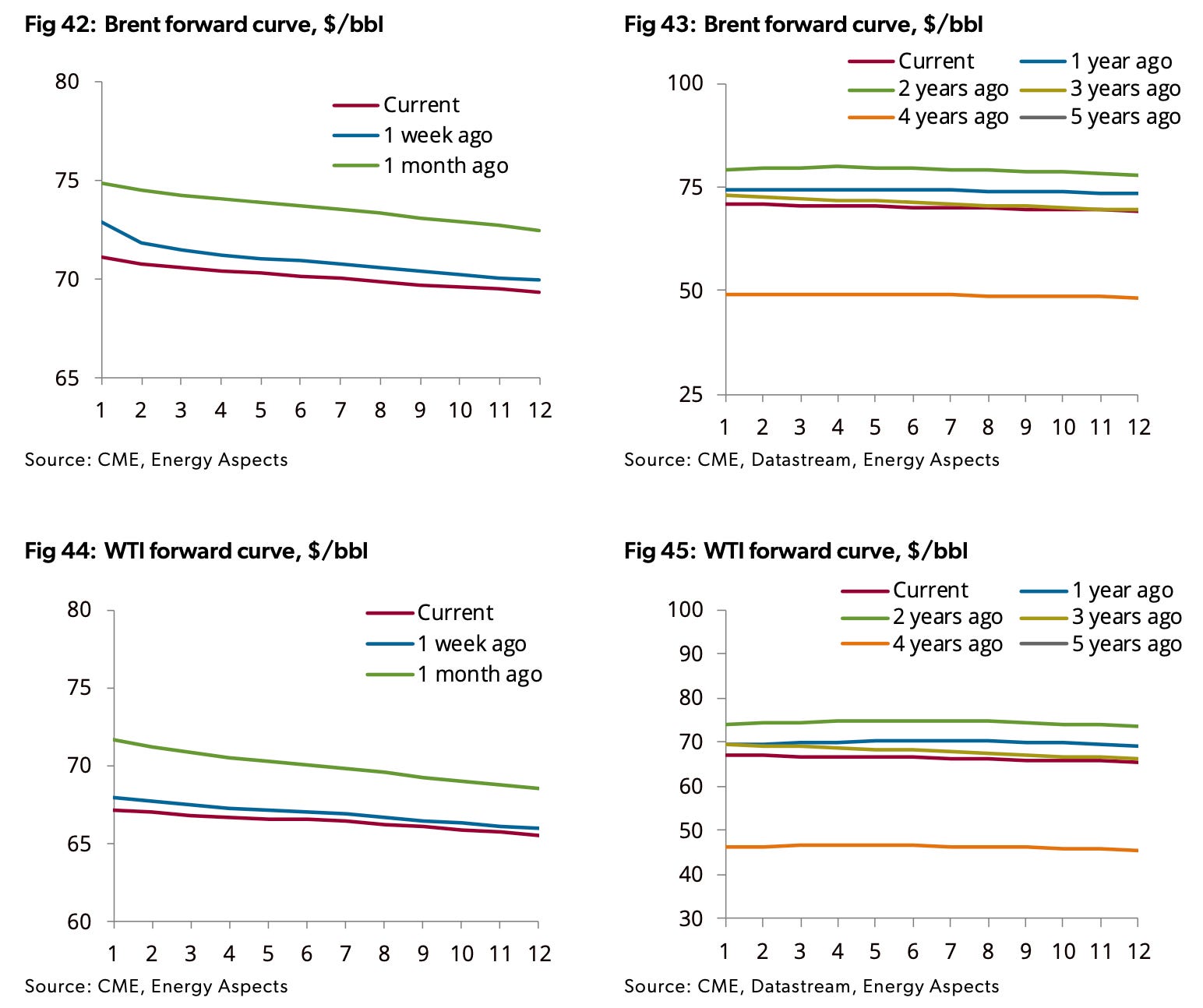

Here is a chart we found of the futures curve at the different timestamps above. And you can see that as oil prices crashed following the Saudi market share war (in 2014), the futures curve went straight into contango.

But with similar builds projected for 2025, we are not seeing remotely the same physical market reaction.

Source: Energy Aspects

You can clearly see that the futures curve remains backwardated. So while the market is not in strong disagreement that we won't have any draws, the lack of a contango structure in the futures curve is an indication that a massive surplus will not materialize.

To make matters worse (or better), IEA is expecting higher inventory draws in Q4 2024 now. October showed observed stock changes of -1.27 million b/d.

Preliminary data shows a rebound in global oil inventories for November, but December data will likely show a global inventory draw again. In total, Q4 balances will point to a draw of ~800k b/d.

With OPEC+ keeping the voluntary production cut in Q1 2025 and a deficit of 800k b/d in Q4, global oil supplies would have to increase by 2 million b/d or global demand will have to fall by 2 million b/d to match IEA's surplus estimate.

While global oil demand does fall seasonally in Q1, higher heating demand could immediately impact balances considering that Q1 2024 was materially impacted by bearish weather.

But even if you assume demand falls by ~1 million b/d in Q1 2025, the natural decline from the US and Canada in Q1 will not push global oil supplies higher. As a result, global oil inventories at worst will show a build of ~200k b/d versus IEA's +1 million b/d surplus.

This is why none of this makes any sense. Not only does the physical oil market not jive with what IEA is saying, but the reality of the oil market balance shows a completely different outlook.

This truly feels like the Twilight Zone.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

Hey - join those of us who are saying the same thing about the stock market. Where's all that transparent data that we thought we'd have by now? Price doesn't lie, and it's saying the market will be tight. And how ridiculous is it to even forecast a "1 million b/d" surplus? Are they seriously trying to say that inventories will build by 365 million from where they are now? Where's it all going to go, and as you've pointed out, the curve doesn't show any financial coverage to carry it.

IEA has for many years now, lost track of its mandate, mission and focus. It's completely shifted towards promoting and supporting the Green-Agenda no matter how retarded or misguided the case may be. This is politically driven, and not one single adult has ever slammed the table and told them to go back to doing their job. They should be defunded and scrapped together with all the false propaganda they have produced.