The setup is perfect.

The consensus expects major non-OPEC supply growth this year just as US shale oil production slowdown materializes. Meanwhile, IEA continues to project 1+ million b/d in surplus even as physical oil market timespreads increase in backwardation.

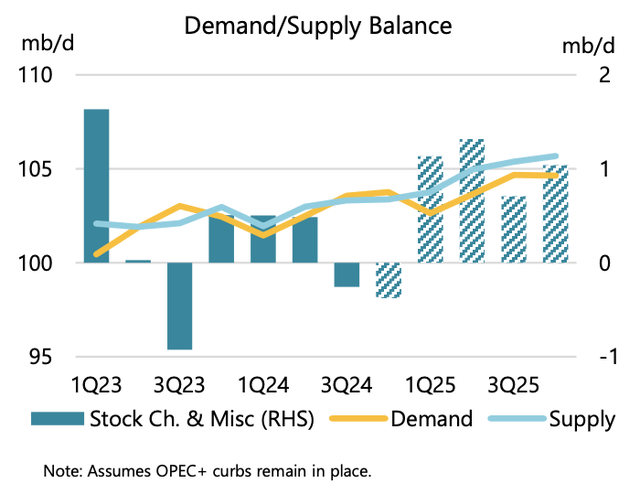

IEA Balance

Brent 1-2 Timespread

Since I've started following oil, this is the largest disconnect between perception and reality.

US Oil Production

Earlier this week, we published our WCTW titled, "An Alarming Trend Is Developing In US Shale Oil Production (Part 4)." In it, we discussed how October's US oil production once again disappointed to the downside and why it's important going forward.

To put into perspective the disappointment in US oil production this year, we made a growth proxy index since 2016.

This uses the EIA 914 oil production figure along with the adjustment factor to calculate the real US oil production figure. We indexed it to December US oil production to gauge just how much growth we saw in that year.

As you can see in the chart, 2018 was an exceptional year where US oil production grew by ~2 million b/d exit-to-exit, while 2024 is on track to be the weakest year to date.