US oil production plateau is here. We have been pounding on this theme all year. This is part 4 of this series and you can read the 3 previous articles above to see whether or not we are on track.

Part 3 was published on Oct 3 with an important section titled, How to verify that we are right?

Here's what I wrote:

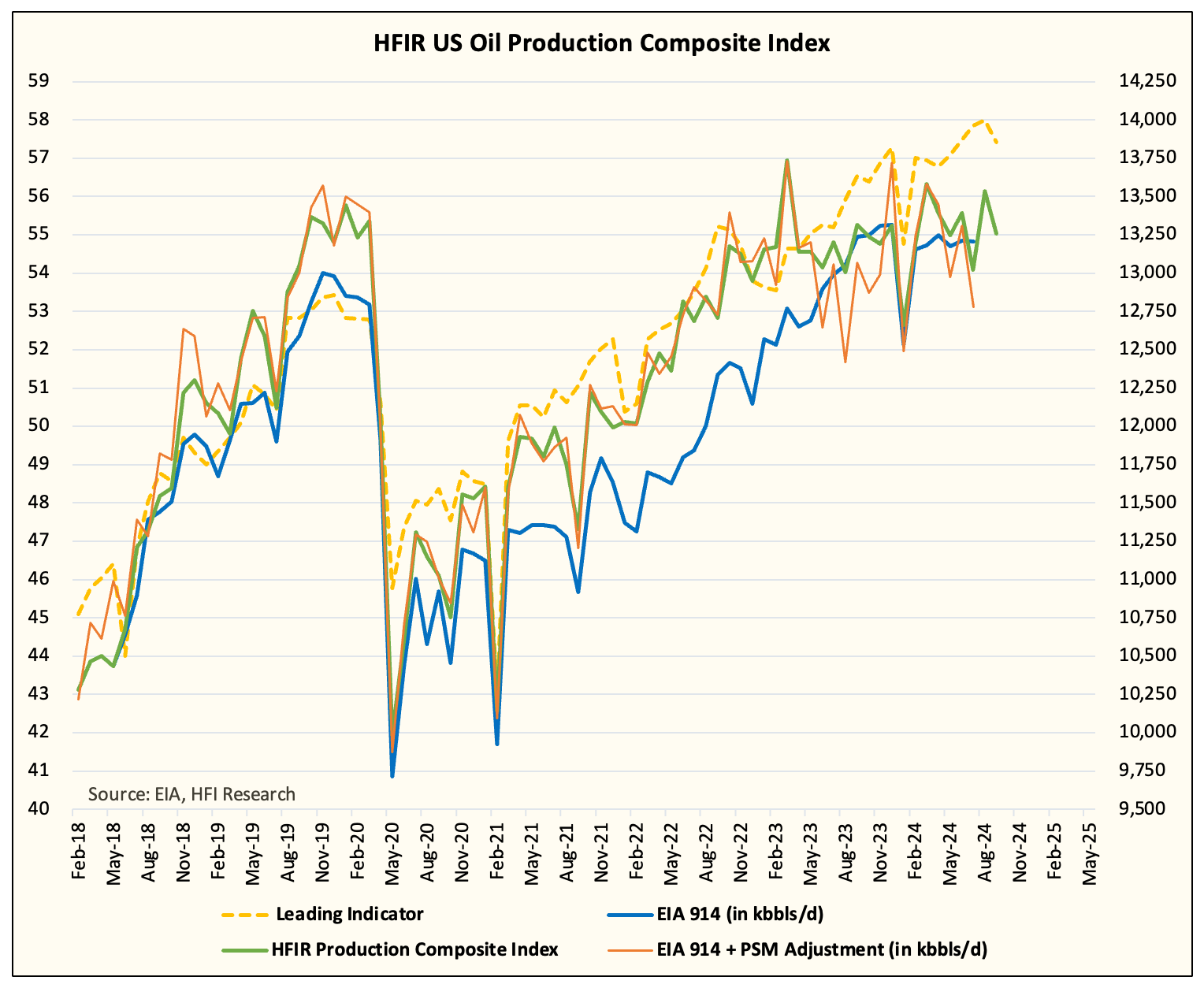

As always, I want to give you tools to validate that we are on the right track. The first tool is to keep watching our real-time US oil production tracker. This has been an excellent tool in figuring out where production is headed, and occasionally, we post our production matrix, which encompasses all the data points.

Second, Matterhorn is coming online, which should increase natural gas takeaway capacity in the Permian by 2.5 Bcf/d. We expect US crude production to increase by ~175k b/d as a result of this new pipeline. If, however, our real-time data fails to show an increase in implied US crude production, then it will be another signal that validates our theory here - US shale oil production is getting gassier.

Finally, EIA oil storage should continue to surprise to the upside versus our weekly estimates. As readers will know, we publish our weekly crude storage forecasts, and typically, our estimates are usually very close to EIA's results. The only times when our results differentiate materially is either when US oil production is disappointing to the downside or surprising to the upside. In either case, we will notify you of what we are seeing. You will also be able to see the development in our real-time US oil production tracker.

With the latest EIA 914 report, it appears obvious that the disappointment in US oil production is coming to fruition.

For October, production + adjustment showed an implied value of ~13.7 million b/d according to our model. Instead, EIA reported 13.457 million b/d for the production and -0.145 million b/d for the adjustment resulting in real production of 13.312 million b/d.

This is ~400k b/d below where we had pegged production and despite the increase we saw in gas takeaway in Matterhorn, we have not seen any corresponding increase in crude production.

To make matters worse (or better), our implied US oil production figure shows an even lower production rate for December.