Trump Won, Now What?

Oil, natural gas, Chinese equities, and drill baby drill.

Despite all of the headwinds and setbacks, Donald Trump did it once again to become the 47th President of the United States of America. I'm not political at all, but after all the traveling I've done in Asia so far, I am damn proud to be an American.

While we can all agree that our relationship with this country can be a love and hate one at times, what makes it so great is that democracy does work. When one side gets too woke, reality hits back, and we saw that firsthand with this election.

Looking back on this election, there are a lot of things we can take away.

Mainstream media is dead. With the advent of Polymarket and Kalshi, waiting for mainstream media to report who won the Presidential election is like waiting for snail mail to be delivered. Elon Musk's purchase of Twitter turned out to be pivotal, and without it, the race would have been much closer (vs a landslide).

Americans are smart and platforms like X and Substack will only grow with time. Readers are starting to flock away from the mainstream media, and writers (such as ourselves) will benefit from the increasing trend in readership.

But putting this aside, let's talk markets. What does a Trump presidency do to the oil market?

On Oct 21, we published a piece detailing the incoming policies from Trump. The first order of business will be to enforce sanctions on Iranian crude exports. The legal process is already in place, and as we've mentioned many times in the past, the Biden administration turned a blind eye on the ramp up in Iranian crude exports.

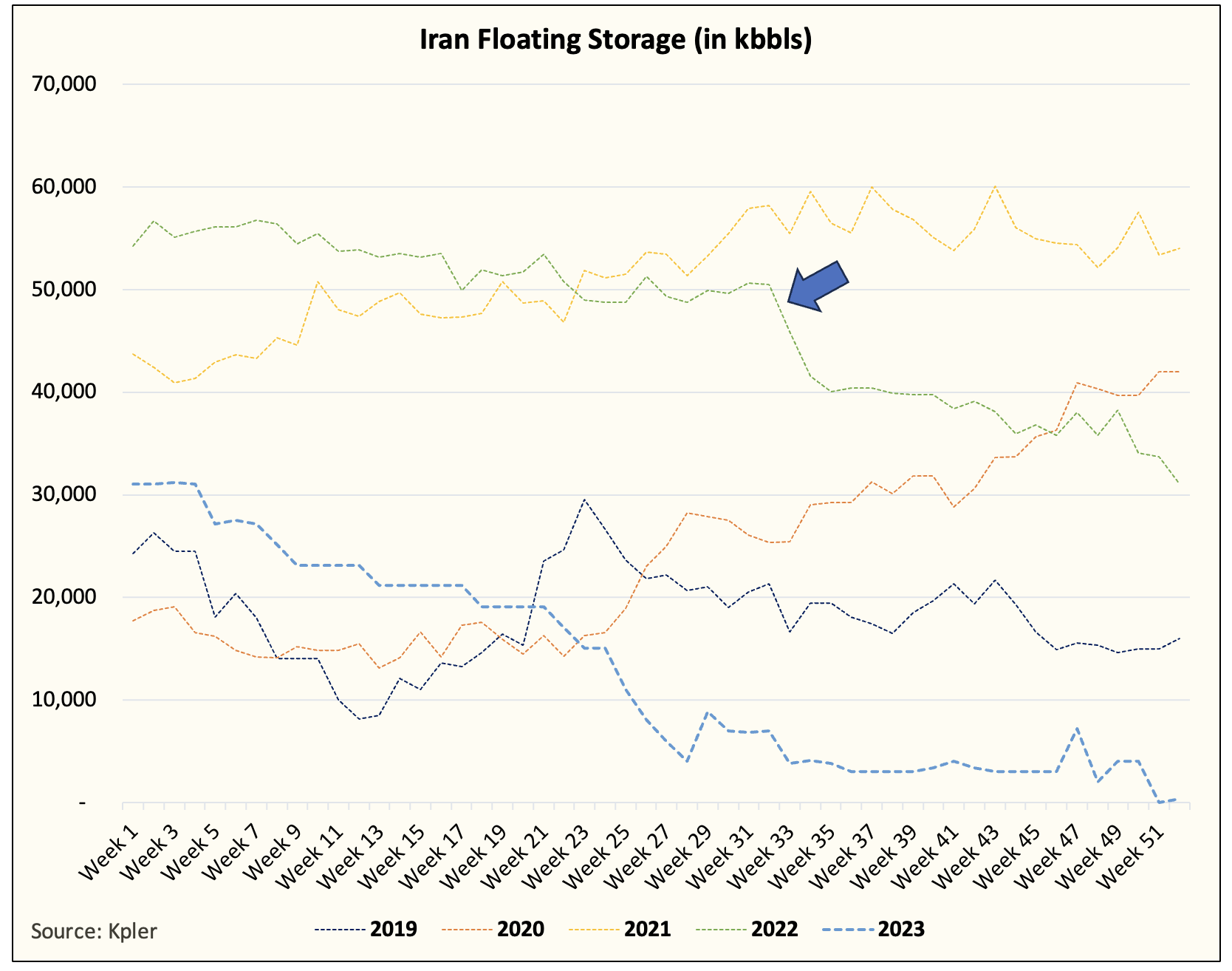

While we expect a gradual decline in Iranian crude production, the first signal we should see will be a material increase in Iranian floating storage.

You can see from this chart we've shared in the past that Iran increased production coincided with the material drop in floating storage. Similarly, we should start hearing about floating storage building to know that Iranian sanctions are being enforced.

But given the logistical timeline of when Trump goes into office, OPEC+ has to decide on whether or not to delay the production increase in early December. My take is that OPEC+ will extend the production increase until Q1 2025 thus preventing some of the inventory builds the market is expecting. And if Trump enforces sanctions like I think he will, then global oil inventories won't build at all in Q1.

At the end of Q1, if the Trump administration enforces sanctions on Iran, then I think we will see OPEC+ gradually return barrels onto the market. In total, I expect Iran to lose ~1.2 million b/d of headline production and ~800k b/d of real production.