The US cannot ban either crude or products. The world is not ready for it. I’m going to be very straightforward here; it will be a disaster.

To put into context the magnitude of an export ban, here are the figures you should know:

US crude exports average ~4 million b/d, or ~9% of global seaborne crude exports. Europe gets ~1.8 million b/d of crude, and Asia gets ~1.6 million b/d.

If the US bans petroleum exports, it will increase the current “flow” outage we are seeing out of the Strait of Hormuz. The US exported ~10.7 million b/d of petroleum products in 2025, effectively doubling the current outage. Strait of Hormuz flow outage is ~11 million b/d, and the US petroleum product export ban would be 10.7 million b/d, bringing the total outage to 21.7 million b/d. In the context of global oil market fundamentals, this is ~20% of global oil demand.

US crude oil production is ~13.5 million b/d with plant condensate accounting for an additional 0.7 million b/d. Refineries in the US are not geared to process ultra-light sweet crude produced by US shale producers. The EIA stopped producing the crude quality table that illustrated the different grades, but based on a rough estimate, the US produced close to 7 million b/d of API gravity 40+ crude. US refineries run an average API gravity of 33. This quality mismatch will reduce US refinery throughput.

Would a crude export ban lower oil prices in the US?

Yes.

Would a ban on petroleum product exports lower prices in the US?

Yes.

But... and this is a really big issue, US shale oil producers will suffer greatly. At the moment, Brent-WTI spreads are blowing out, with WTI remaining flat, but the scenario I’m going to explain will show why WTI will go down.

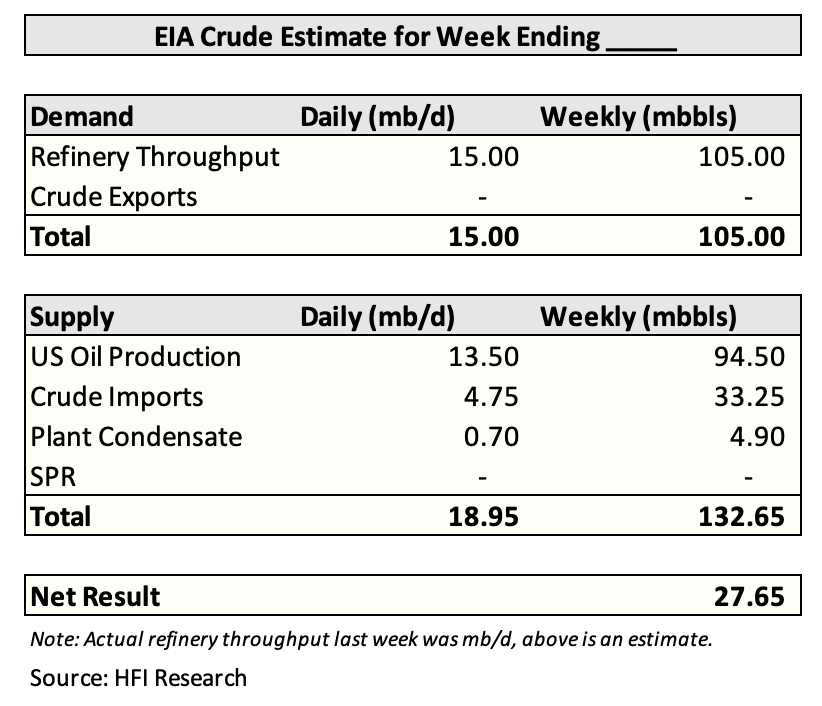

Every week, we publish our US crude storage estimate. We have built this expertise over the last 8 years. Yes, it’s a long ass time to be doing something like forecasting US crude storage.

In the above scenario, a hypothetical roadmap of what would happen to US commercial crude storage on a weekly basis if US crude exports were banned.

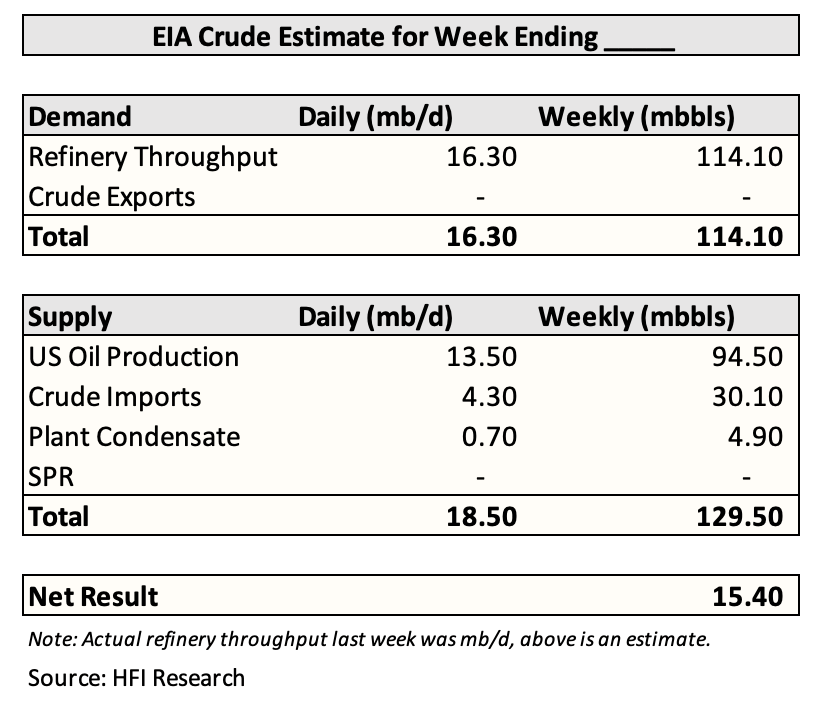

If product exports were also banned, it would further lower US refinery throughput, but for this mental exercise, we will only look at crude.

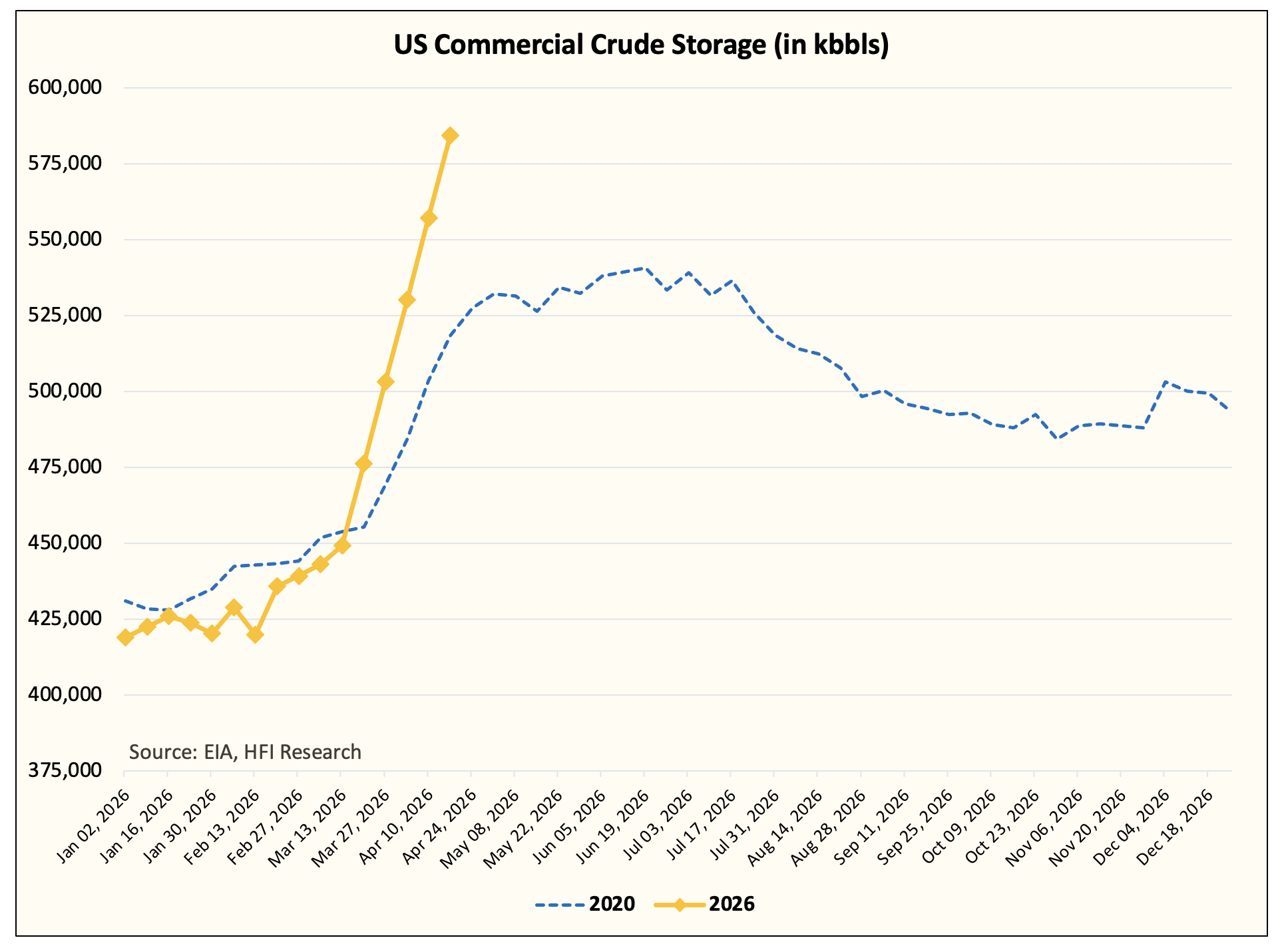

At the moment, US commercial crude storage is at 449 million bbls. In 2020, US commercial crude storage topped out at around ~540 million bbls. This coincided with Cushing reaching the tank top level of ~65 million bbls. The operational maximum capacity is between 540 to 570 million bbls.

By our estimate, if US crude exports were banned and US shale producers continued to produce the exact same volume, US commercial crude storage would hit tank top by mid-April.

Please keep in mind that the market will likely force a response before that by sending WTI sharply lower, forcing producers to shut in production.

The US commercial storage landscape and the shale boom were built on the notion that we can freely export crude and products. Without the export ban being lifted in 2015, US shale producers would never have had the room to grow production meaningfully. It was thanks to the lifting of the export ban that this happened.

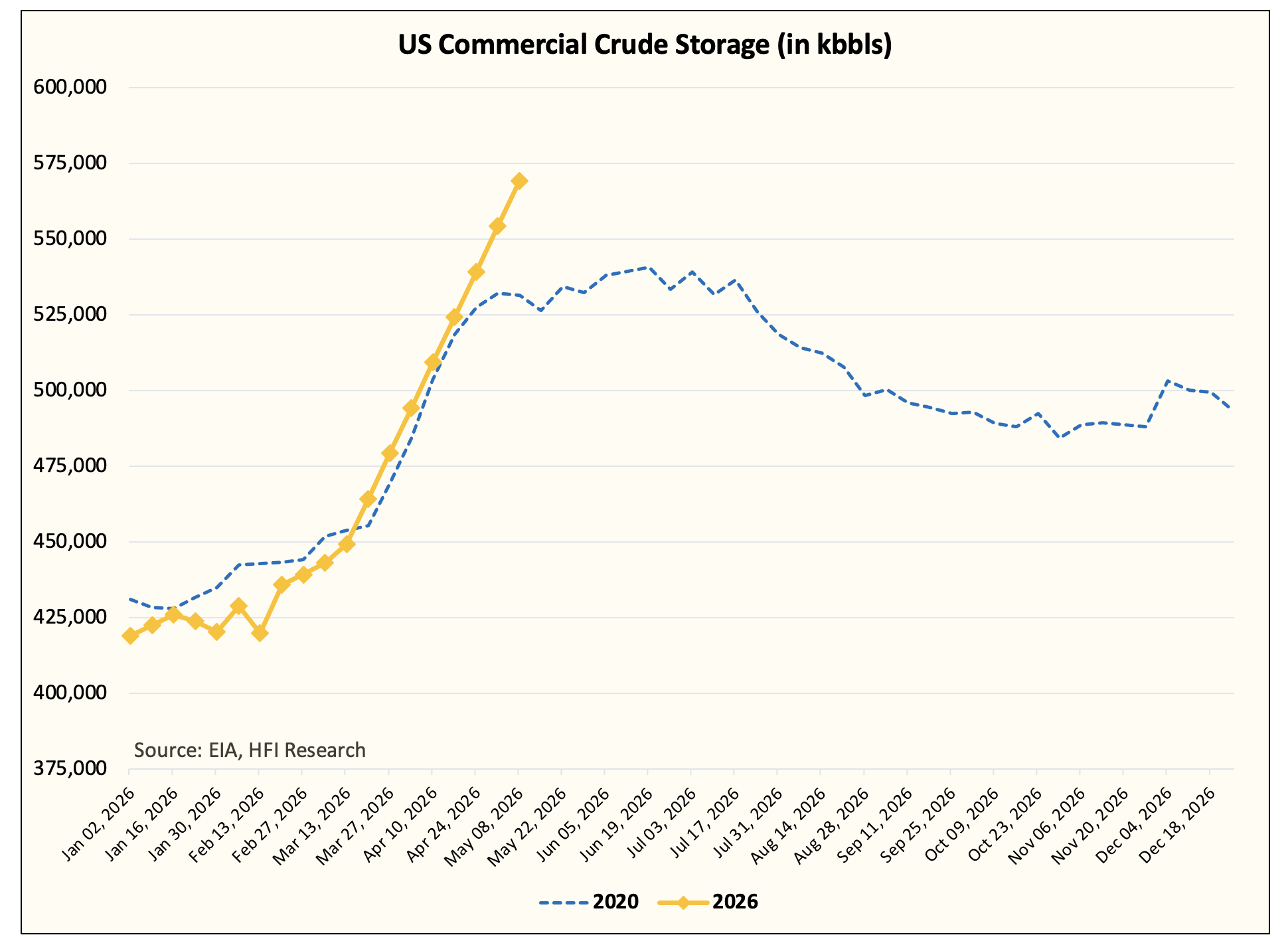

Now, if we assume that US refineries continue to draw down medium/heavy crude during this time period, and we start to price out seaborne crude imports, this is what the weekly balance would look like:

At +15 million bbls per week, we will reach tank top by the first week of May.

Again, if this scenario happens, storage in PADD 3 would swell, basin crude differentials would blow out, and US shale producers would have to shut in production.

This is not a scenario you even want to contemplate here. It’s like shooting yourself in the foot.

Investment Implications

If the Trump administration bans US crude exports:

Short WTI

Long Henry Hub

Long natural gas producers in the US and Canada (associated gas production will fall due to production shut-in)

Be ready to buy the dip in US and Canadian oil producers.

Because of the implications I wrote above, the export ban, if enacted, won’t last long at all. Storage tank tops will force the Trump administration to act, so we don’t see this lasting more than a month.

Readers who are aware of the dynamics can take full advantage of this disconnect.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.

You know this already, but I just wanted to say thanks for ramping up the notes and commentary despite everything else on your plate. It would’ve been a lot harder - and a lot less profitable - without your insights. And 8 years of forecasting crude storage? That’s insane. Hats off to you.

Btw is this accurate? Summarizing what I learned.

What happens to WTI prices if the U.S. bans oil exports? It will push WTI prices lower because:

a) Domestic storage will fill up quickly, and

b) With storage maxed out, producers will be forced to shut in production.

c) Prices will fall to levels where production becomes unprofitable or unattractive.

What I don't quite understand yet is why nat gas producers will benefit. Will do more research later but will appreciate any resources you have. Thanks!