On July 6, the V8 will meet again to discuss whether or not to announce another truncated production increase. Judging by the leaks so far, it appears OPEC+ or V8 will agree to another +411k b/d increase. But since this plan was first announced in early April (coinciding with the Liberation Day tariff announcements), the increase in OPEC+ crude exports has been nonexistent.

But this is not news to anyone that read our OPEC+ gameplan report. This is what we said:

It was never a cohesive production cut agreement from the beginning. It was always a Saudi production cut. The actual impact of the truncated production increase is more semantic than something fundamental, and those who don't understand that will continue to use this as a bearish signal, when it's really the opposite.

But as the perception of a faster-than-expected increase continues to pressure the market bearishly, energy specialists have to wait for the reality (no real increase) to set in. This will take time, and I think people will grow increasingly frustrated with the material disconnect that's going to take place.

So, yes, while I am saying that the production increase won't actually impact the market all that much, I am not saying to ignore the market price action implications of this. Oil will be negatively perceived because perception "trumps" reality.

With the meeting this weekend set to increase production by another 411k b/d, there will only be one truncated production increase left before all of the voluntary production curtailment disappears. At this point, the oil bears that pointed to the impossible task of unwinding production cuts will have to accept the reality: the production cut was never cohesive; it was a Saudi cut.

It Gets Interesting

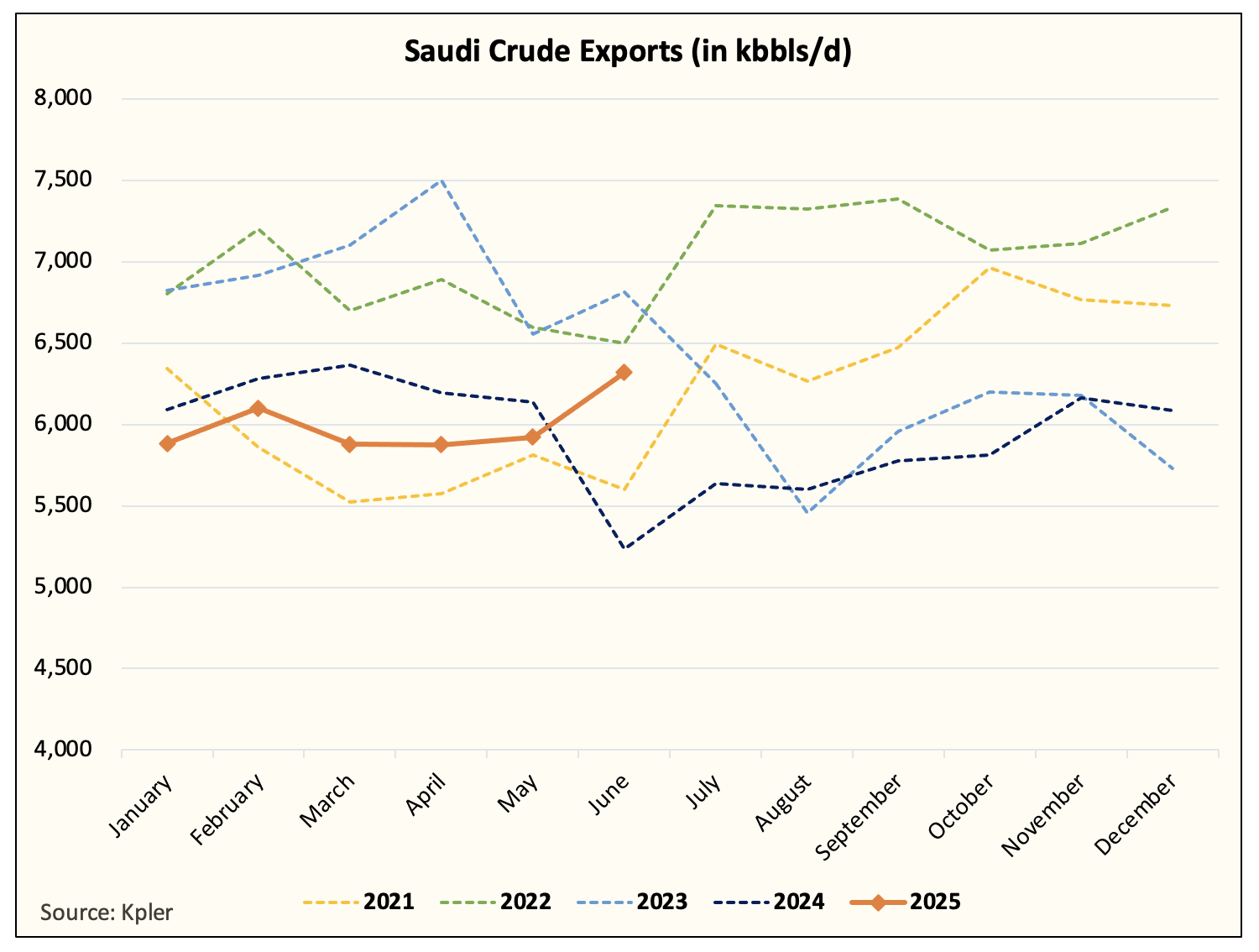

For the next two months (July and August), OPEC+ crude exports will remain muted due to higher domestic power burn demand. It is, however, important to keep in mind that despite flat crude exports, the group's overall volumes are higher y-o-y by ~1 million b/d.

The entirety of the delta is coming from the Saudis. As we wrote before, the incoming production increase from the Saudis is real. For market participants who think otherwise, the chart above should dissuade you.