(Public) Death By A Thousand Headlines

Jawbone headlines are delaying the inevitable in the oil market: demand destruction.

Someone recently asked me, “How are you so calm through all of this chaos?”

My answer is simple: I find all the fake jawbone headlines amusing because if the oil math were off, there would be no need for any of this mess. The more desperate the attempt to keep oil prices tamed from fake “imminent deal resolution” headlines, the more convinced I am that the oil math is right.

Today was one of those wild days. Al Arabiya, with the likes of Axios, already had a reputation for publishing premature peace resolution agreements.

It wasn’t long ago, on May 7, that the Al Arabiya diplomatic source published that securing safe passage for ships in the Strait of Hormuz was imminent. Now that it’s 14 days later, I guess there was nothing imminent about that.

But the funniest one of them all came today.

Now Al Arabiya has come out denying that it was a professional error to have attributed the breaking news to it, and they have since deleted the tweets.

Why is the oil market so susceptible to these daily fake headlines? I will explore that further later, but the important thing to remember here is that you cannot borrow conviction, and these are trying times.

Times like these require you to dig deep and assess the level of conviction in your own analysis. As I’ve been saying since the start, there is no historical analog to the level of supply outage we are seeing today. The oil specialists all agree on the production shut-in. That’s a fact. There might be some back-and-forth on 1) operational minimum/tank bottom, 2) demand destruction level, and 3) inventory storage decline pace. But the reality is simpler than that: this is the largest oil supply outage by 4x. You can be off by 1 million b/d, and it won’t change a thing.

When does the jawboning stop working?

Death by a thousand headlines has made trading oil particularly difficult, even for the physical oil traders. No one can take conviction positions in futures today without getting their daily beatdowns.

JH did a wonderful job breaking down what’s happening, so I highly recommend that you read that.

In essence, volatility in futures has forced traders to turn to options to play any upside. There is currently no price discovery because no one has the financial firepower to force it.

In an ideal world, prices should have gradually moved higher to a level that slows incoming visible oil inventory draws. This would remove the sudden knee-jerk reaction of what happens when global commercial oil inventories reach operational minimums. We are already seeing several oil hubs reach that level. Fujairah, the closest oil hub to all of this, has already reached tank bottom.

But since there’s no way to force price discovery and we have not had the intended effect on demand destruction (~2 million b/d is our estimate), we will just need to run out of commercial oil inventories before the jawbone stops working.

In my mind, it’s either the US/Iran conflict escalates again, and traders have no choice but to lock in the physical barrels needed for August, or we go straight to operational minimums.

Pick your poison.

And speaking of demand destruction, these daily attempts to keep oil prices tamed have had the opposite effect of what an efficient market is supposed to do.

Japan is releasing the 2nd-largest SPR on record, and it has vowed to keep prices at pre-conflict levels, further stimulating demand.

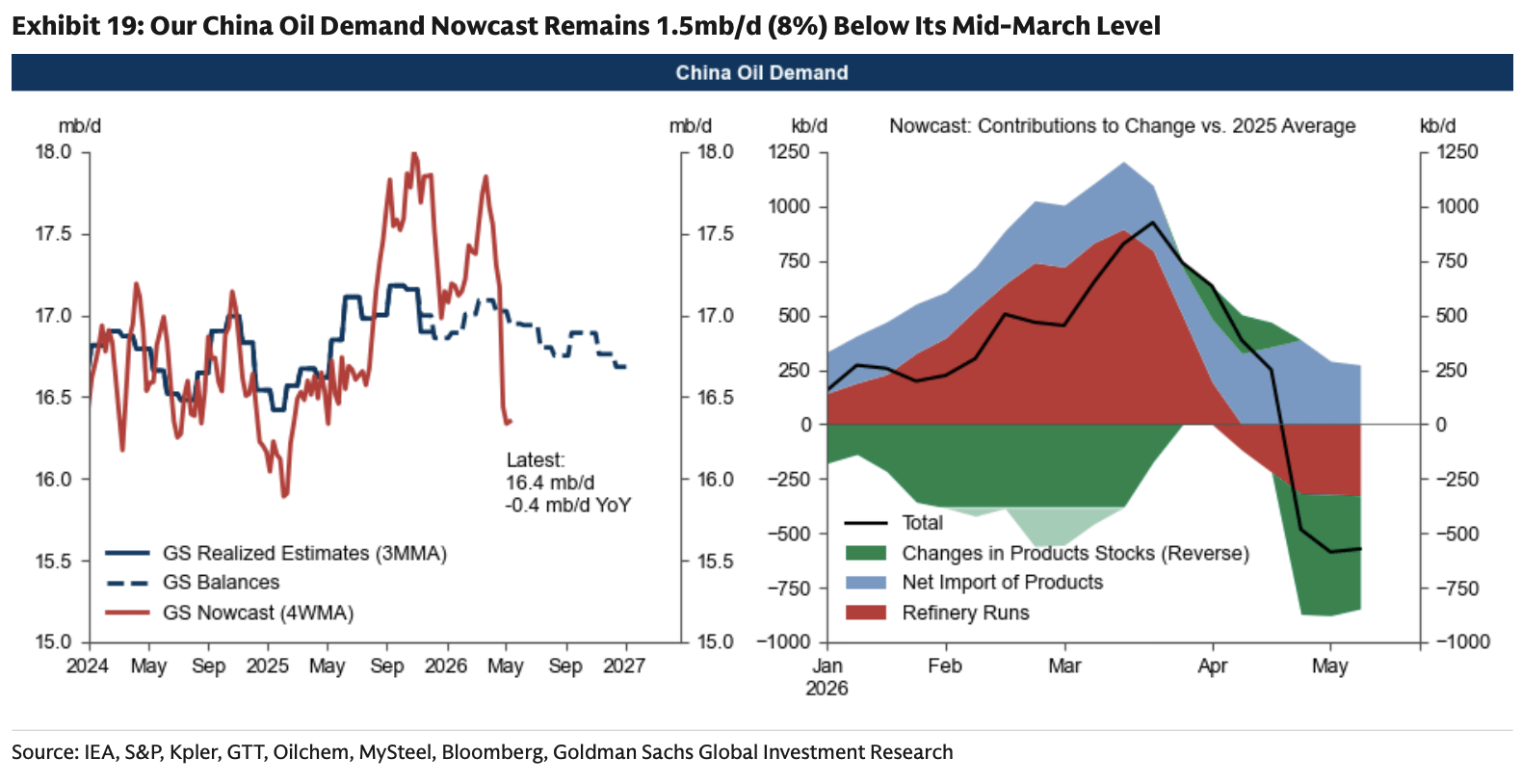

China is showing a demand drop of 0.4 million b/d y-o-y according to Goldman’s real-time data.

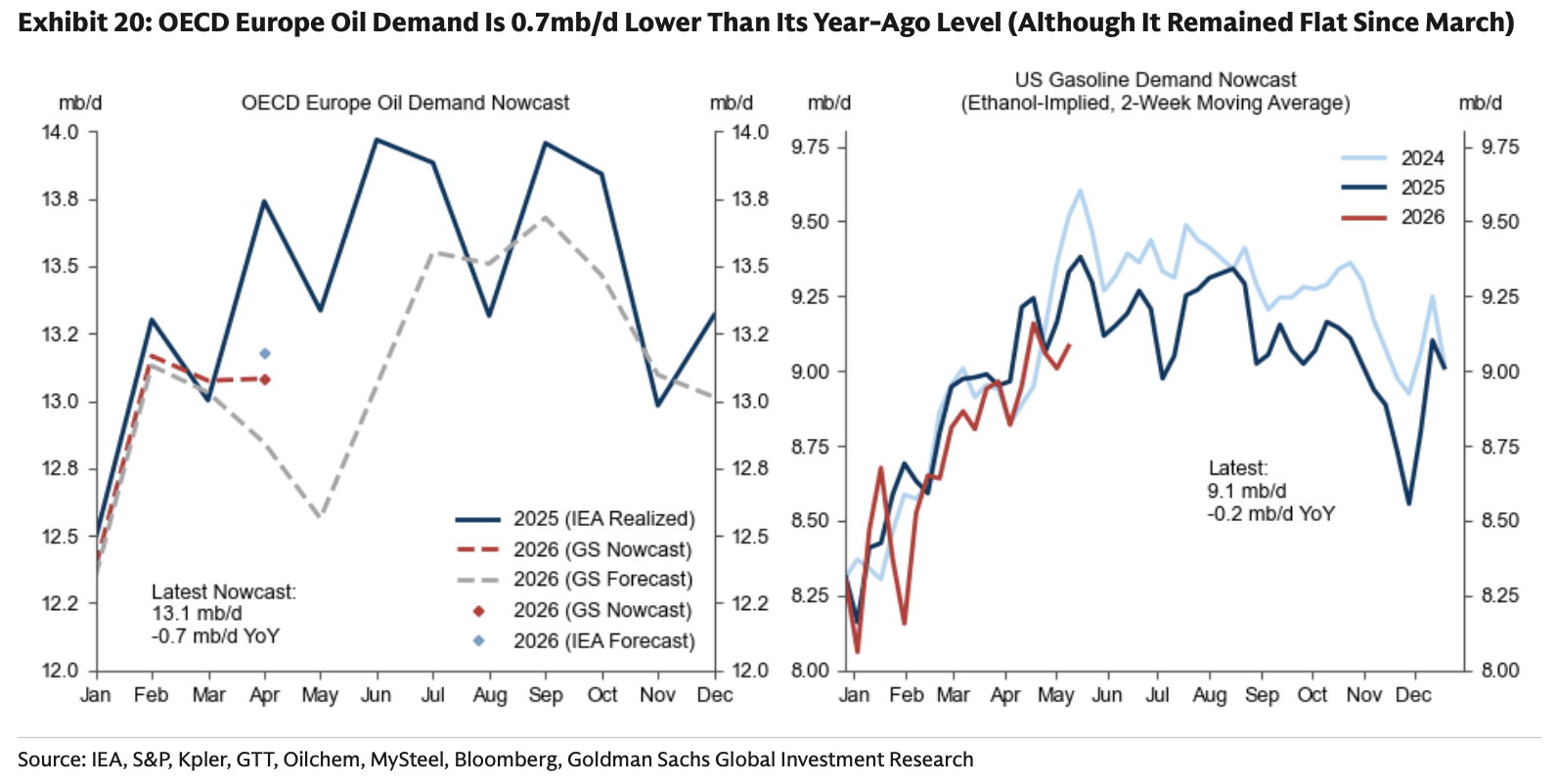

Europe is showing a demand drop of 0.7 million b/d y-o-y.

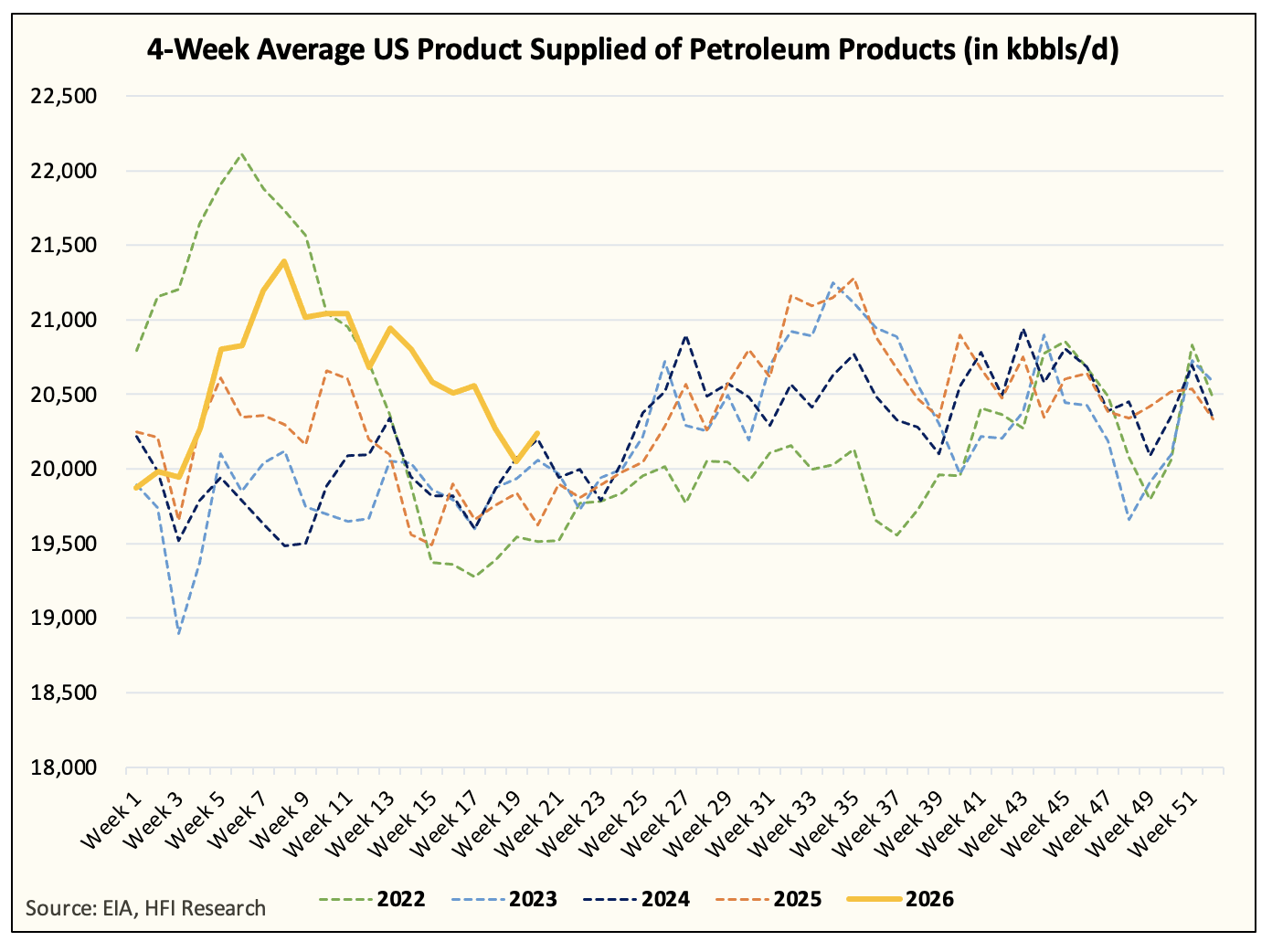

And US implied oil demand is up 0.6 million b/d y-o-y.

Japan: no change, 3.2 million b/d of demand

China: -0.4 million b/d, 16.35 million b/d of demand

OECD Europe: -0.7 million b/d, 13.1 million b/d of demand

US: +0.6 million b/d, 20.3 million b/d of demand

Net: -0.5 million b/d, total demand of 52.95 million b/d or just under ~50% of global oil demand

Look, the math is what it is. People are being lazy and assuming that a reduction in refinery throughput equates to demand destruction. It’s not. I don’t know how many times I have to say this.

In addition, it doesn’t take a rocket scientist to figure out that at the peak of COVID-driven demand destruction, global oil demand fell by ~20 million b/d. Just look at the global mobility indices, do you see an equivalent 25% in activity drop, the size of the drop we saw in COVID? Do you even see a blip?

If people want to ignore the data and focus on narratives, let them. I’m not interested in changing people’s minds because I’m here to make money. If they want to believe that, I really don’t care.

So yes, these daily jawbone attempts are keeping global oil demand higher than it should. We should already be moving towards demand-destruction levels to slow inventory draws, but we aren’t doing that. We are going full speed into the wall.

Timing

I get it. Everyone wants to know two things: when do the jawbones stop working, and when do prices reflect this?

As I explained above, you either get more conflict, which will be a catalyst in itself, or you just run out of inventory.

For this, I turn to Bennie K, whom I highly recommend along with JH.

Source: Bennie K

For me, I like to keep it simple.

There are only two regions in the world with “real” excess crude oil inventories today: China and the US.

China is a black box. No one even knows how much oil inventories it has. It doesn’t publish its data, so all 3rd-party providers are just guessing. We can estimate how much it has, but only after the fact.

I propose a simpler solution: follow the US.

Let me explain.

Since the onset of the conflict, oil barrel counters knew that the US would be the last place to draw. If you’ve been in oil long enough, you know why. The US, thanks to the US shale revolution, is in a particularly interesting situation.

US shale produces crude of a quality not needed by US domestic refineries. It produces ultra-light sweet crude, whereas US refineries require heavy/medium sour crude. Imagine playing tennis with a golf ball, and golf with a tennis ball. They are both balls, but they are not in the right sport. You can kind of get the gist.

US also benefits from landlocked Canadian heavy oil. With Venezuela as an ally now, the US also has another source of heavy crude. Because the barrels received from Canada and Venezuela usually have an API gravity below 25, we need to blend these barrels with condensate. The remaining excess gets exported. This is also another reason why the Trump administration should never ban US crude exports.

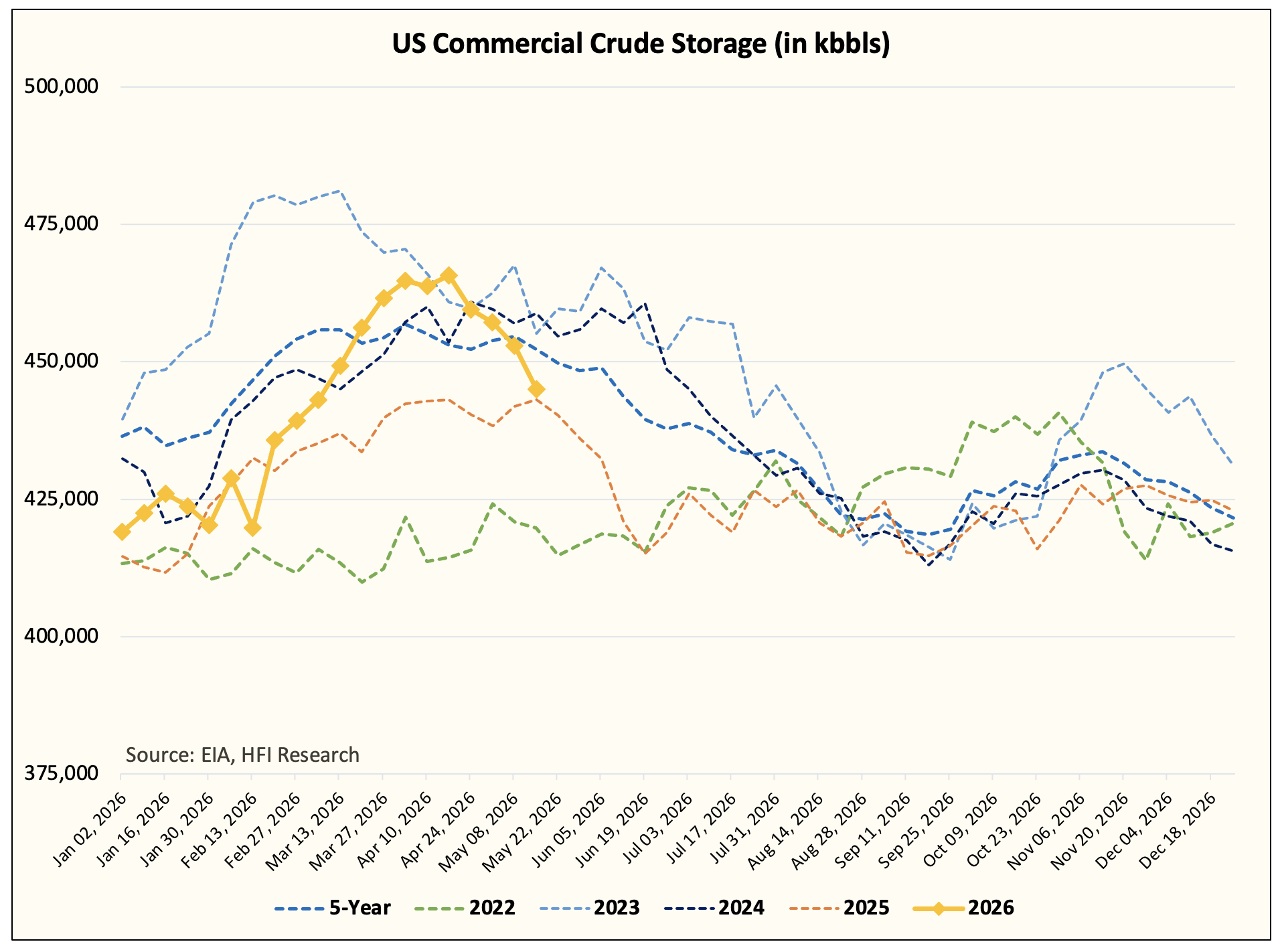

The only reason US commercial crude storage would drop is that there’s “demand” for the barrels. If there was low demand for the barrels, US commercial crude storage would build, all things equal. This is why you didn’t see a decline in US commercial crude storage at the start of the Iran conflict.

But this all changed by early April. When I wrote that the oil market breaking point was mid-April, it was because we knew from the deficit math that the world would start pulling US commercial crude storage lower. The US is releasing ~10 million bbls a week now in the SPR, and all of that implies the US is the last place with excess crude.

So the moment US commercial crude storage started to decline, I knew it was just a race against time. The demand pull would drop US commercial crude storage to an operational minimum, and the chaos would unfold. Once US crude exports get priced out, the rest of the world will suffer. The marginal barrel is gone, so everyone will have to compete for that extra 1-2 million b/d of crude. It adds up quickly.

The timing for US commercial crude storage to hit operational minimum is late July. But the market will need to price out US crude exports mid-June. Oil Bandit has already noted that US crude exports are getting priced out; it’s only a matter of time.

Why does it matter?

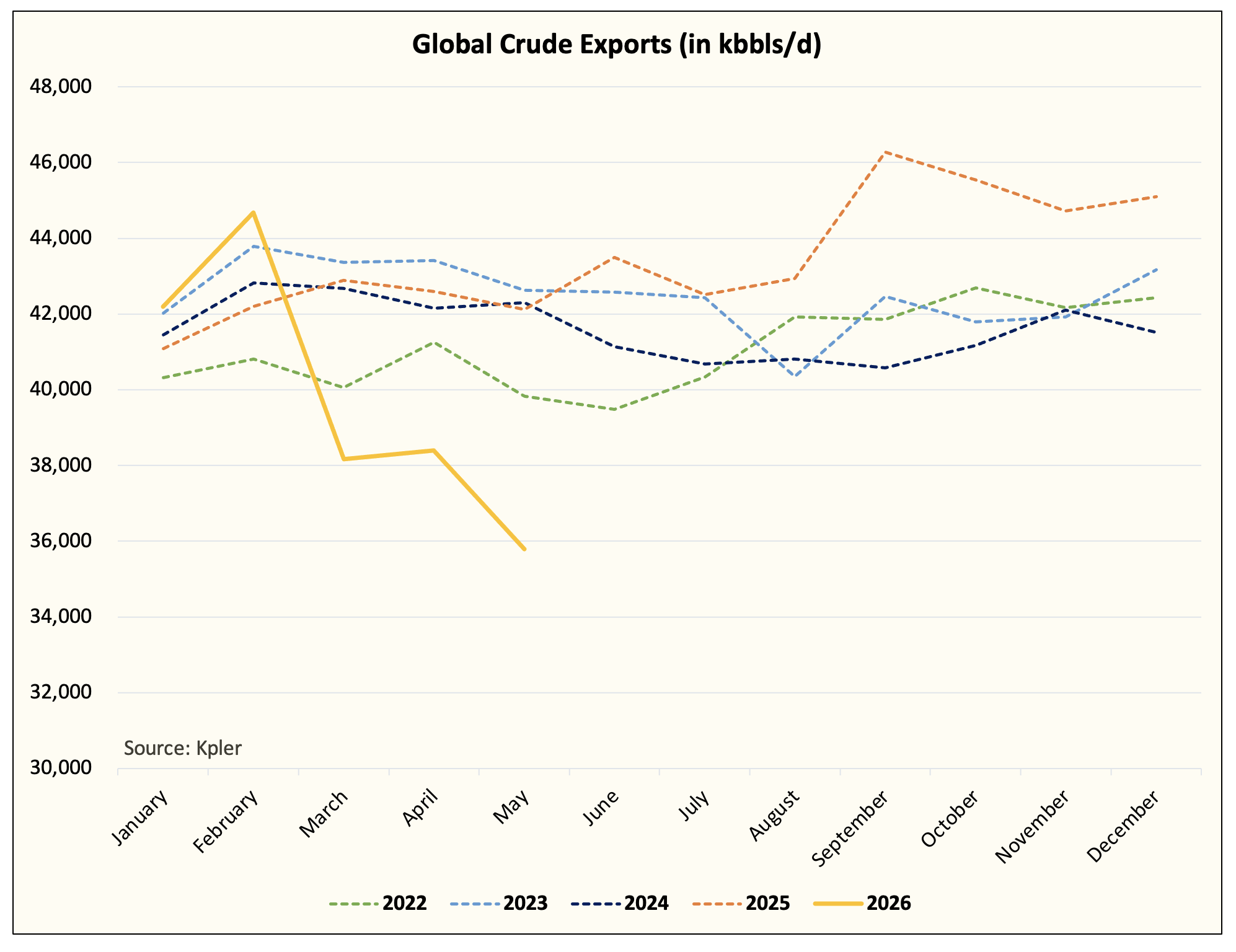

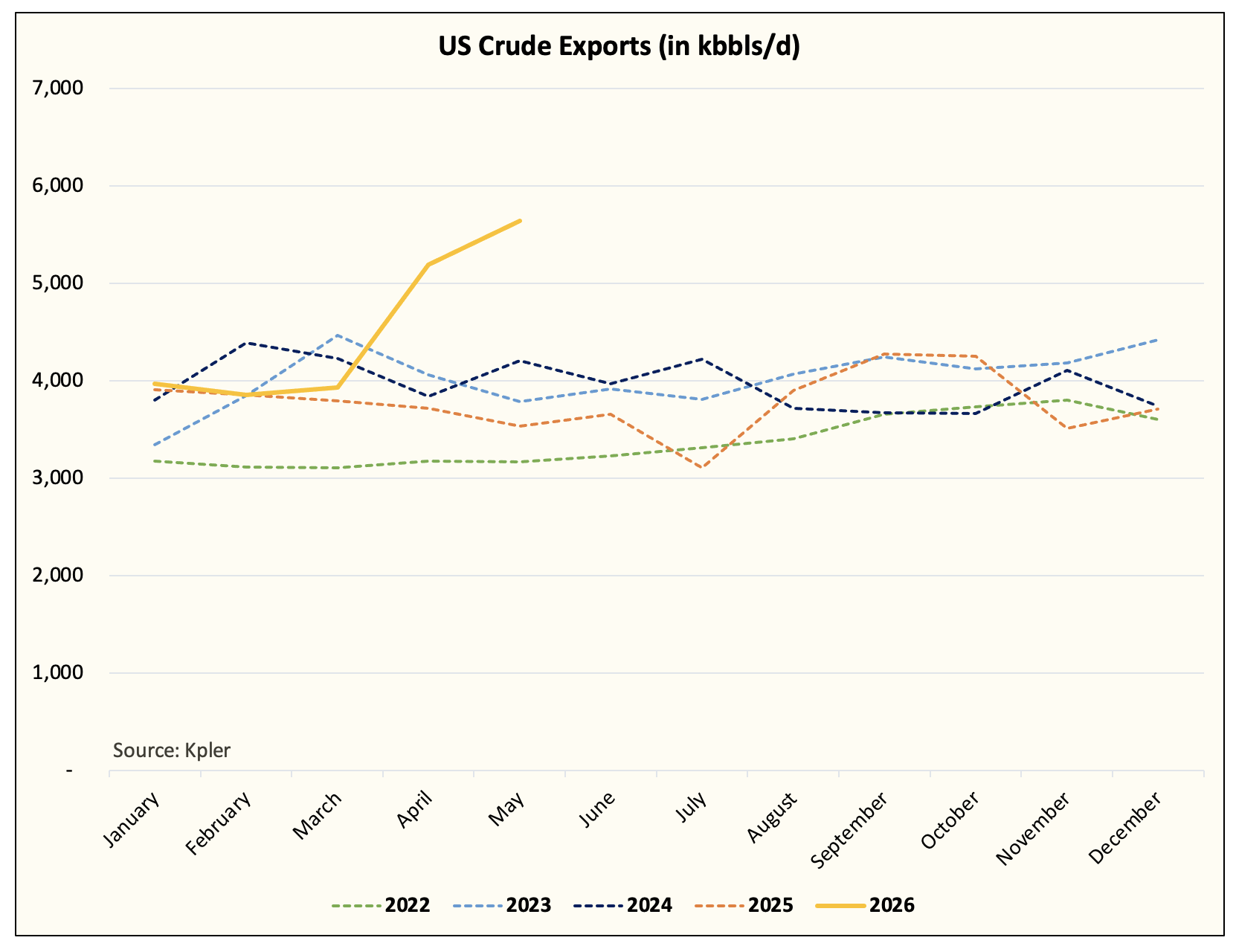

Global crude exports are currently down ~6 million b/d y-o-y.

US crude exports are up ~2.1 million b/d y-o-y.

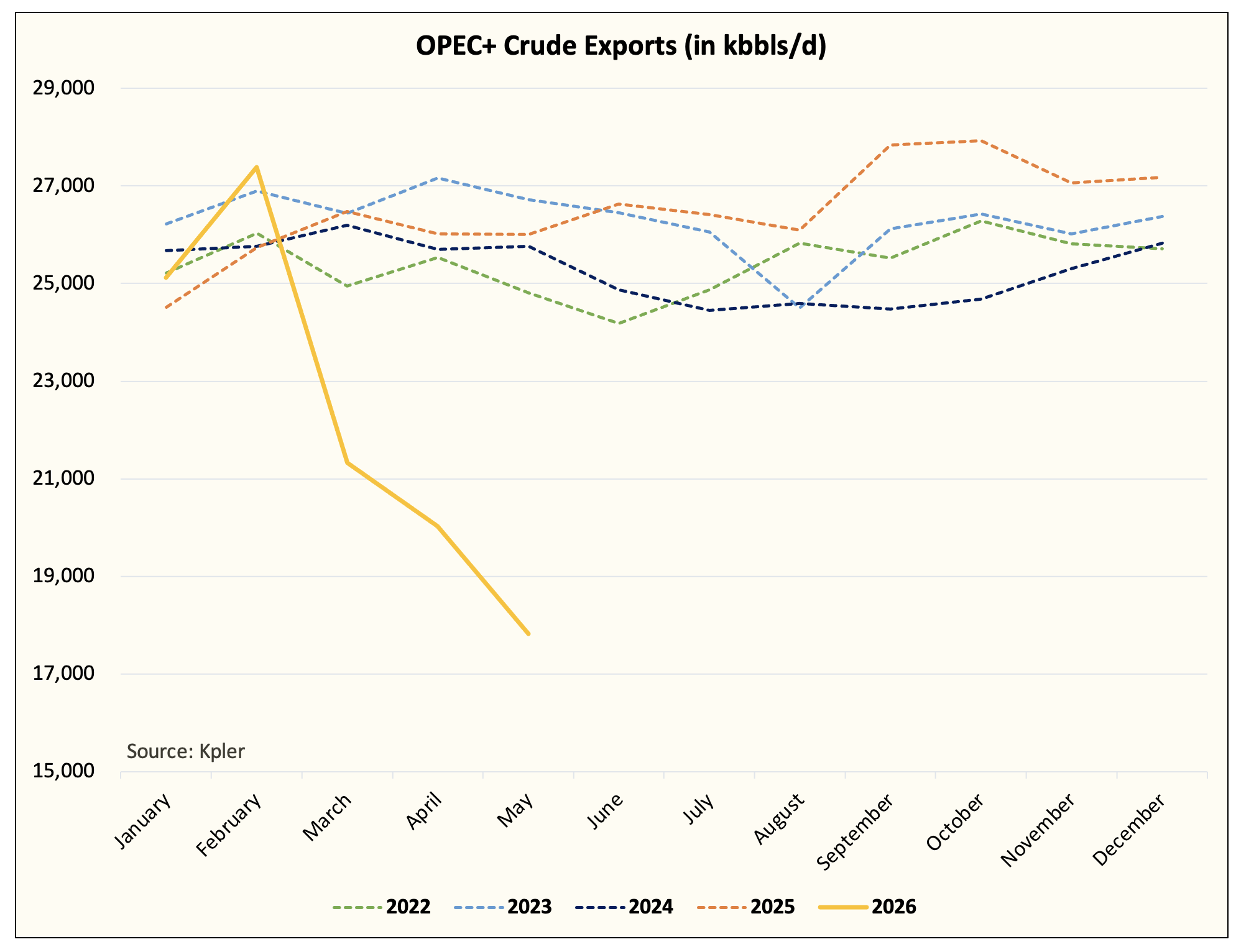

OPEC+ crude exports are down ~8 million b/d y-o-y.

I think you are getting the point. The US, thanks to its excess crude oil inventory, has managed to offset ~25% of the decline in crude exports, but that will run out.

And for those of you who have followed every tight oil market scenario over the last decade, the US is always the last place to draw, and so when it’s gone, it’s gone.

As a result, from a timing perspective, the market needs to price in this operational minimum scenario for US commercial crude storage in June. Because you will literally run out of excess crude.

Conclusion

The level of jawboning has reached unprecedented levels, but it just proves to me that the oil math is on the right track. I mean, these guys literally published that a deal was imminent on May 20th, 15 minutes before the EIA released the largest crude draw in history. You can’t even make this stuff up anymore, but it is what it is. The oil math is what it is.

The oil market might be suffering the death of a thousand headlines today, but it is a real commodity at the end of the day, and you can’t print more molecules.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO, UCO, BNO either through stock ownership, options, or other derivatives.