Explaining The Long Oil Trade

This is public.

To make everyone’s life simpler, I’m going to explain why I’m long oil. I’m not going to mince words here. If you want a more detailed explanation of what I’m going to write here, read our reports. I’ve made the Breaking Point series public. Part 1, part 2, and part 3.

As of this writing, everyone who has traded oil in the last 2 months has PTSD. PTSD from what? Headlines.

As an oil trader said to me, “Death by a thousand headlines.”

So I’m going to say it here: The long oil trade works even if the Strait of Hormuz opens this very second.

Why?

Simple:

Logistical delays. Even if the Strait of Hormuz reopens, it would take 2+ months before flows in the Middle East return to normal. Production shut-in returns will be gradual, so visible oil inventories will continue to fall.

Every trader on the planet right now is waiting to go long in size AFTER the Strait of Hormuz reopens because they are aware of this logistical delay. Just because the Strait reopens doesn’t mean production shut-in returns. If you still don’t grasp this logic, I explained it in detail here.

As of this writing, we are on pace to lose 1.59 billion bbls. This eclipses the ~400 million bbls released from the SPR and would force another round of SPR releases even after the Strait reopens. Yes, the inventory draws coming will force this outcome regardless.

Everyone in the oil community agrees on the math to a certain degree.

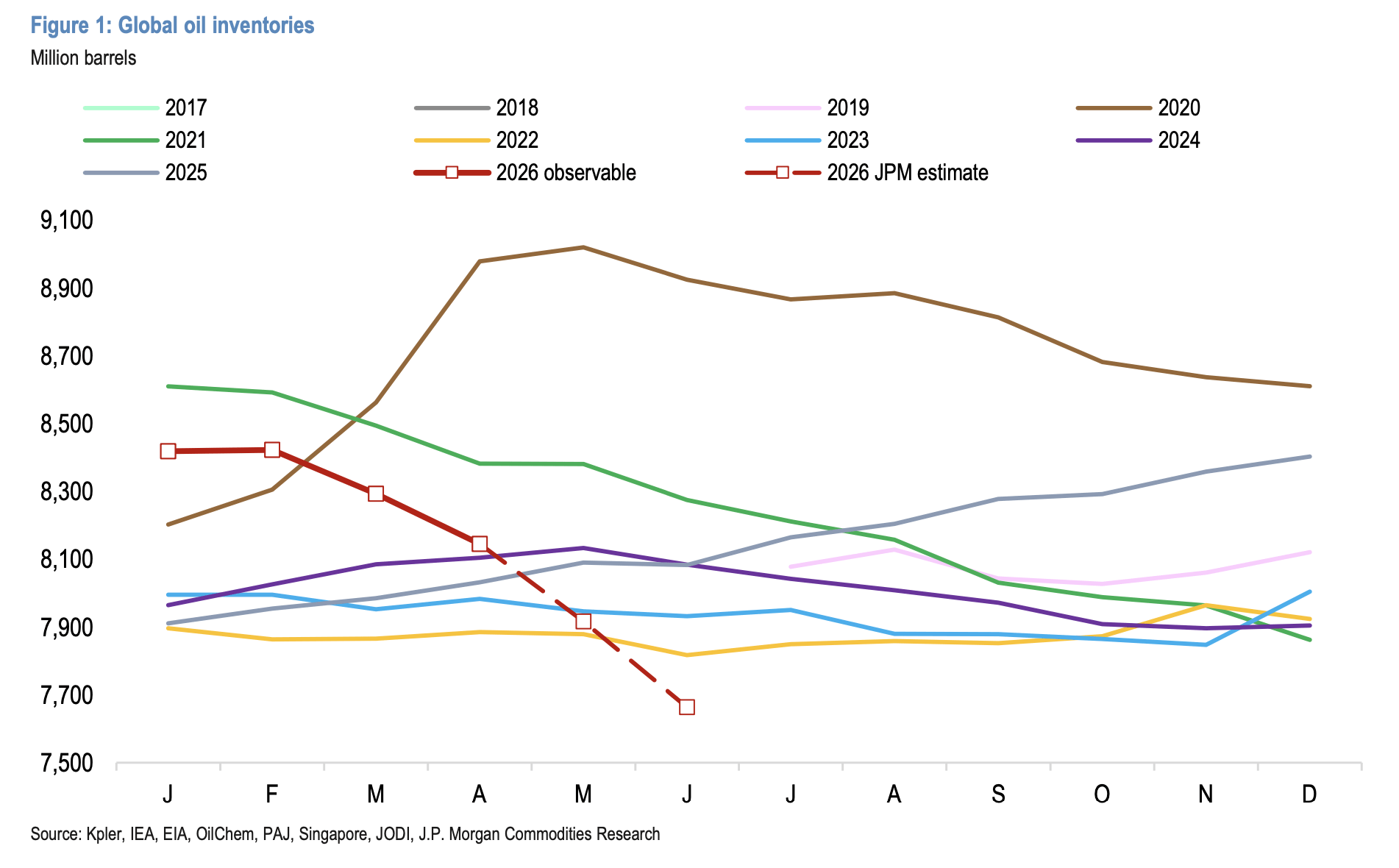

JPM:

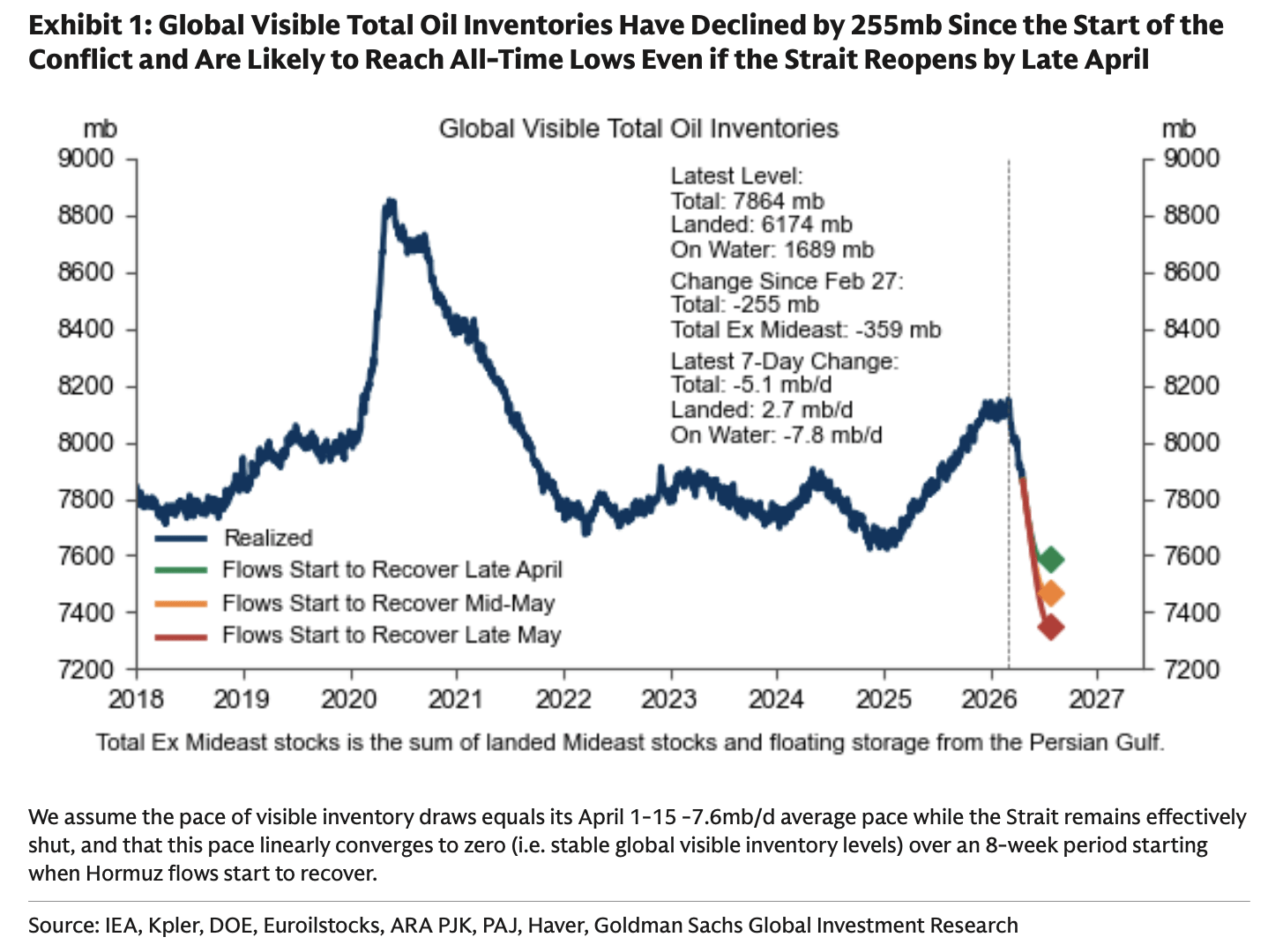

Goldman:

Inventory draws are coming even if the Strait of Hormuz opens this very second.

That’s the whole point. That’s the entire long thesis. If your worst-case scenario is a complete reopening and the oil trade works, it works. That’s it.

What price?

True to my words, I don’t know as I explained in my mid-April write-up. Because the visible oil inventory draws are literally punching us all in the face now, it will be hard to figure out a price that rebalances that much of the supply gap.

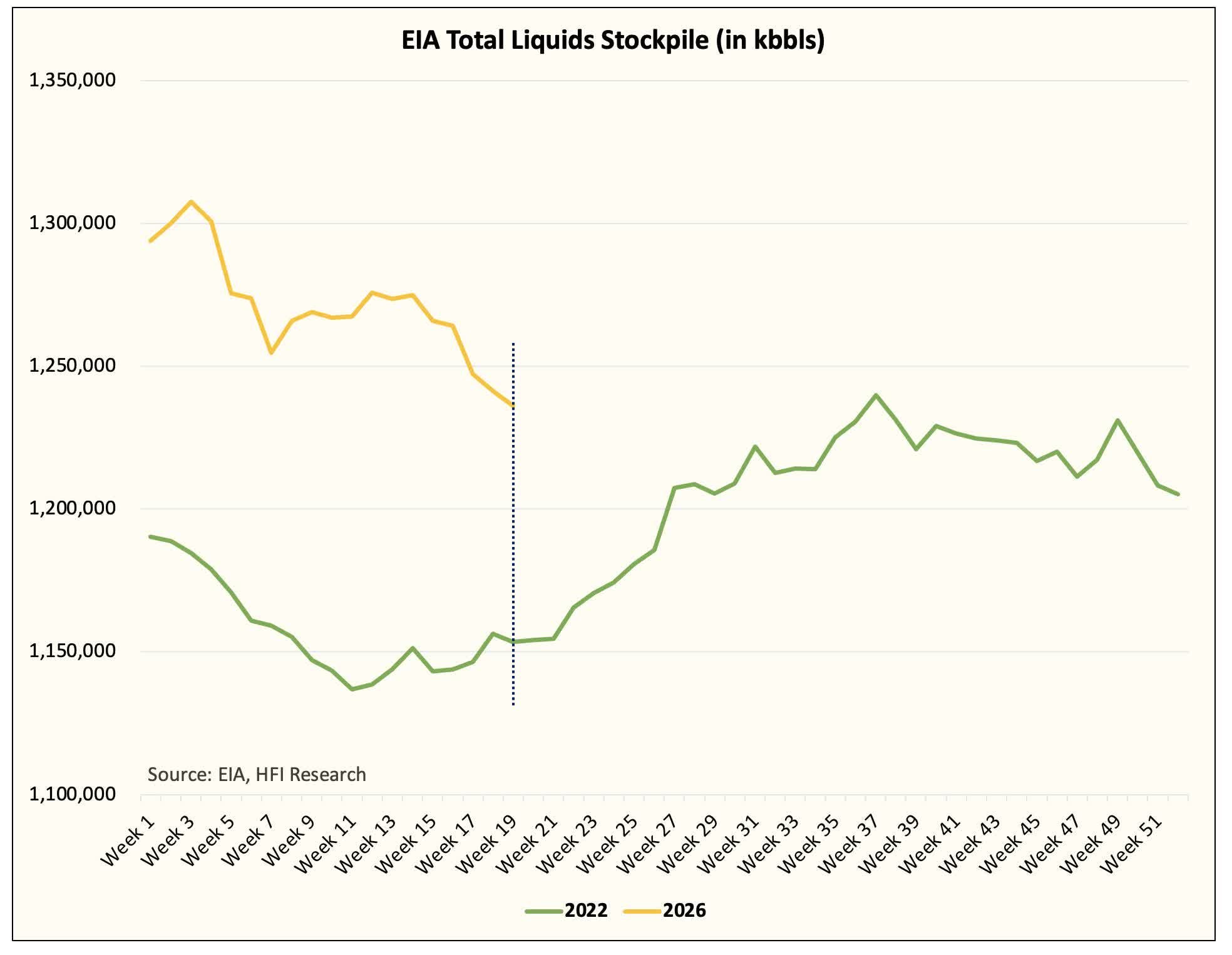

But for context, in April 2022, the most visible oil inventory data in the world (the US) started to turn bearish. And despite no supply outages, Brent went on to hit $120 in June.

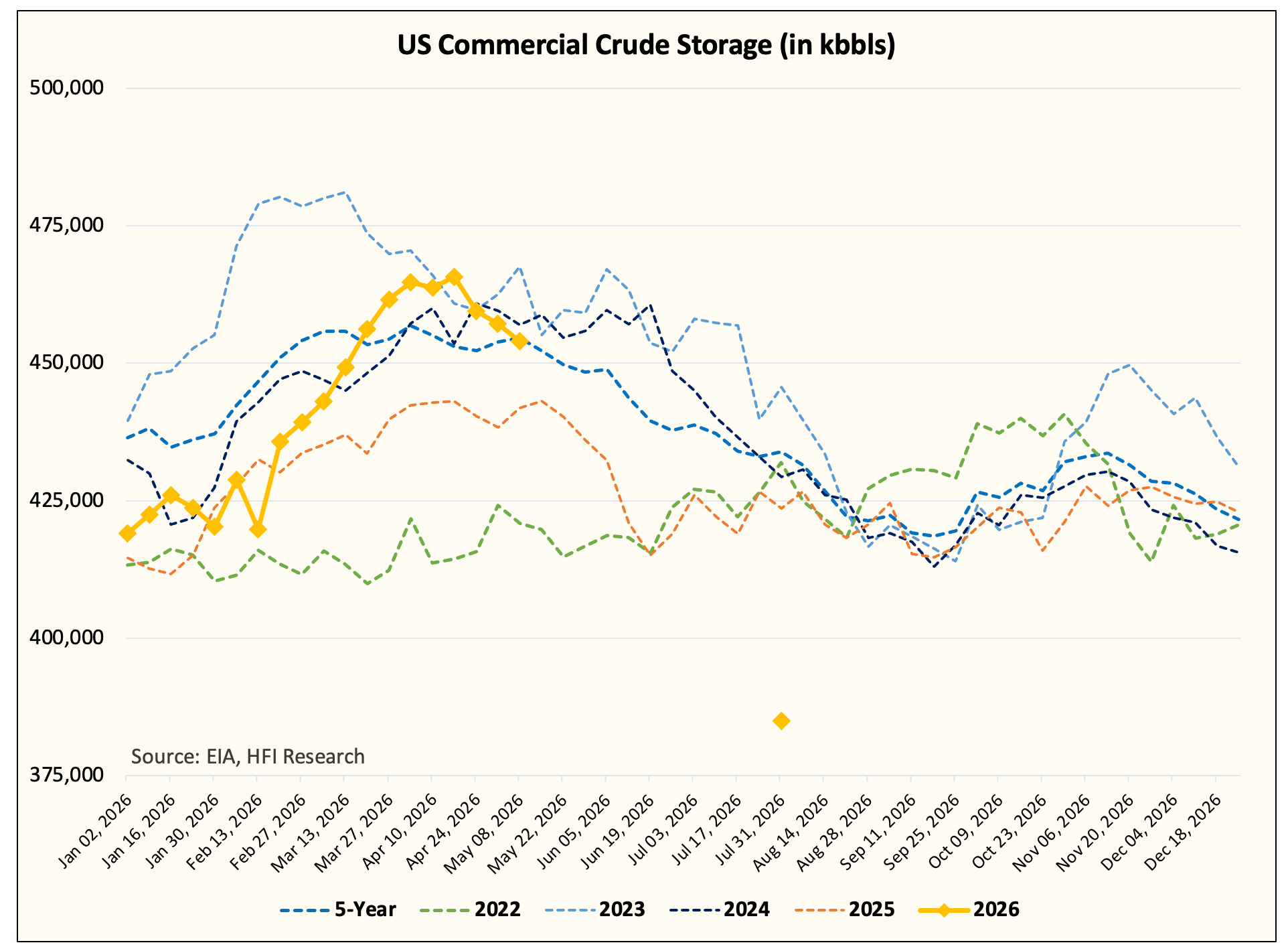

And although we are not at the same level of oil inventory in the US this time around, we are about to see the fastest visible decline in oil inventory in history. We will reach 2022 levels in 4-5 weeks. For US commercial crude storage, we will hit multi-year lows sometime in July:

Relatively speaking, and using US oil inventory as a barometer, Brent will be above $120 in a month. And that’s assuming everywhere else’s storage is flat as a pancake (zero percent chance of this happening, by the way).

What is the price?

I don’t know, but it’s not $105 Brent.

Positioning

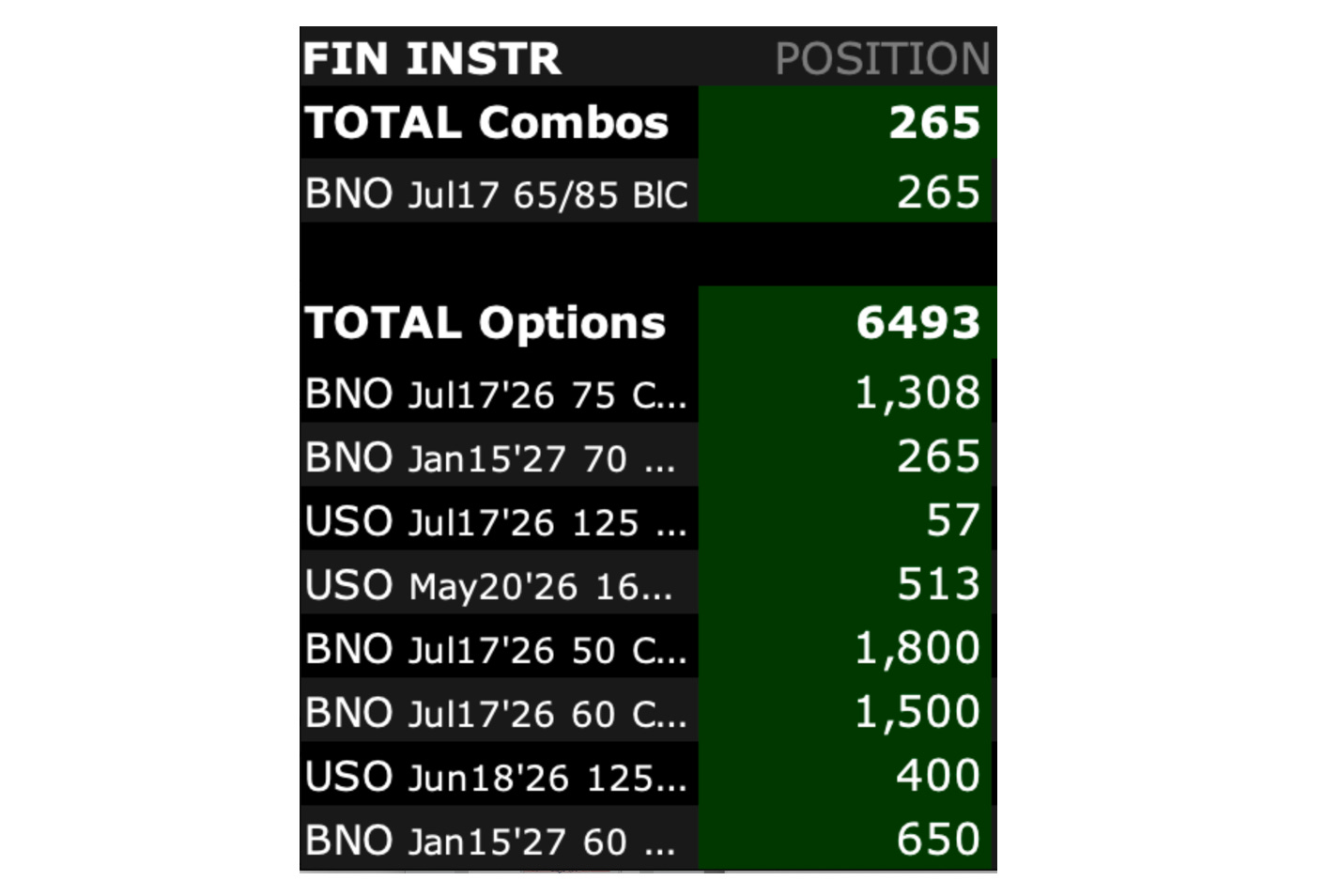

I am very long.

This is obviously not financial advice. You do whatever you want, but I’m putting my money where my mouth is.

It is what it is.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO, UCO, BNO either through stock ownership, options, or other derivatives.

Why the focus on July options and not October for more breathing room?

What would be very helpful is if you were to provide a small table showing how much July 17 BNO call options at one or more of the strike prices you hold would be worth on July 17 at a few different oil prices, like 100, 110, 120, 130 140 and 150 say. Probably many of your readers could do this themselves, but I, for one, would have more confidence in your calculations than mine.