Editor’s Note: This article was first published to paid subscribers on April 27, 2026. This article is public.

In our April 19, 2026 WCTW report titled, “The Oil Market Breaking Point Is Here.” We said:

If the Strait of Hormuz opens after April, we cannot provide an accurate oil price forecast. We will have crossed too deep into the Rubicon. This will have been the largest oil supply outage in the history of the oil market by a magnitude of 4x. Fundamental market theories will no longer apply here because there’s no price for outright shortages. When a market runs out of fuel, it just runs out.

Over the coming weeks, if the Strait of Hormuz remains closed, sell-side analysts will try very hard to “forecast” an oil price only to fall short initially. As I’ve explained before, there’s no historical precedent for what we are witnessing in the market today. The only way to offset the supply loss of ~11 to ~13 million b/d is through COVID-like mandated lockdowns.

Outside of government-mandated lockdowns, market-led demand destruction of this magnitude has never occurred. Even during the Great Financial Crisis of 2008, we did not see demand destruction anywhere near ~12% of global demand. The only relevant timeframe was from 1980 to 1983, when global oil demand fell by 10%, but that was over 3 years. This time requires an instantaneous rebalancing to prevent oil inventories from hitting the tank bottom.

Again, no one, especially not us, can provide you with an accurate oil price forecast. Instead, I will walk you through the logistical roadmap of what I see happening.

Roadmap

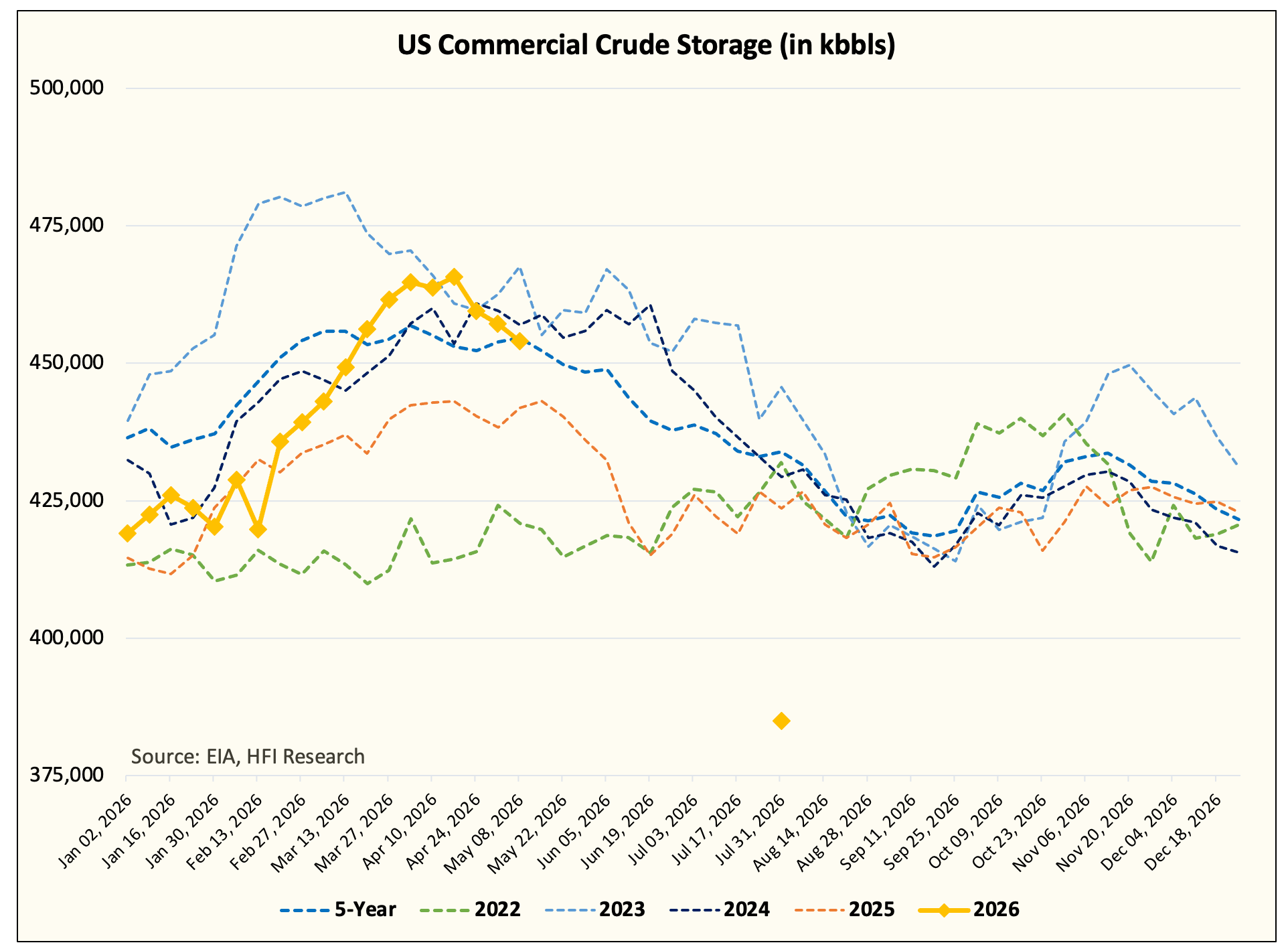

We are already past the oil market breaking point. As we explained in our initial oil market breaking point article, cumulative storage lost (including reopening) is now 1.2 billion bbls.

From here on out, oil market will follow the logic I explain below:

We have now exhausted excess oil-on-water and floating storage. Every barrel that declines now will be in the form of crude storage, product, or demand destruction.

Refineries with a lack of crude in storage will first reduce throughput. They will increase buying to compensate for the lack of crude. This buying will be in the form of higher backwardation in the prompt months. As a result, crude timespreads will remain steeply backwardated.

Given that the supply outage is concentrated in crude, refining margins will remain elevated in the regions with no excess in crude. Asian refining margins, for example, are very elevated today, assuming you have access to crude. Regions with not too much excess in crude, but also no material shortage in products will see refining margins compress (think Europe). Regions with both excess storage in crude and products will see refining margins elevated (think North America).

Because the shortage is in crude, Asian refineries will not be able to access the crude they need, so they will start importing products. Product demand from the East will pull higher refining margins from the West. Europe’s refineries will see a bump in refining margins, allowing them to afford the elevated cash crude price. The US will also be dragged higher, incentivizing higher throughput.

All the while this is happening, refining margins will remain elevated worldwide. This signal basically indicates there’s no demand destruction yet.

Note: We are now entering this phase below.

This step is when things get interesting. Product storage will get low in the West (inside a month for both Europe and the US). Refineries will be incentivized to keep products at home because domestic prices have reflected better economics. Now Asia will have both a crude and a product shortage. Asian refining margins will take another leg higher as the outright shortage translates into even higher product prices. Asian refineries, seeing the surge in margins, will have room to bid at any price for crude on the physical market. This will start to pull more crude from West to East.

Refineries in the West (the US and Europe) will all of a sudden have to compete against Asia for this increase in demand. This now becomes a bidding war among all the refineries over the crude shortage. The US, which previously had a surplus in crude inventory, will start bidding aggressively to keep barrels at home. Brent - WTI spread would collapse as a result.

As refineries start competing aggressively for crude, prices will not follow the usual linear pattern but will follow a parabolic pattern. The ripple effect will be that both refining margins and crude prices rally in tandem until one of those breaks.

How do you spot the eventual turning point:

First, global refining margins will fall as end-user product demand declines. Margins will remain positive. Refineries that can access crude will still be able to make money, while those unable to access it will have to shut down entirely.

Second, crude timespreads will start to fall. Backwardation will narrow. Refineries unable to compete for crude oil due to compressed margins will fall by the wayside. This incremental change in demand is the 2nd red flag.

Third, global onshore inventories will stop declining. Product demand destruction will first translate to a flat line in product storage. Once refinery throughput falls enough, crude storage will also have bottomed.

Finally, the combination of falling refining margins, falling crude timespreads, and lack of decline in onshore storage will signal to us that the physical oil market has rebalanced.

From an oil long standpoint, you want to sell your positions when the crazy bidding war starts. There’s no telling how high prices can go because it’s dependent on how much the end-user can handle. Marginally, we will lose some demand each time prices rise, but no one can forecast exactly how much. The only way we can measure that will be through real-time data like flights, mobility index, satellite storage data, and refining margins.

Coincidentally, when the shortage actually shows up is likely when the generalists will panic. We have developed sentiment indicators to identify the eventual turning point. I like the use of the term “contrarian indicator” here for people who can’t correctly understand the current outage. These are likely the same individuals who will get bullish oil at precisely the wrong time.

The Ripple Effect

Asia is the most dependent on the Strait of Hormuz oil flow, so it was always the first region to be impacted materially.

First, all poor countries will face fuel shortages, but as these shortages shake governments, panic buying will pull demand away from wealthier Asian countries.

This ripples into increased buying for crude from wealthier Asian countries. This starts to tighten crude supplies from the West.

Higher buying from Asia tightens crude storage in the West, forcing refineries there to compete to keep barrels at home.

We are 2-3 weeks away from this last step. Onshore oil inventories in the US will have to decline first, and since the US is releasing the largest amount of volumes from the SPR, the bid for US crude will continue. That is, until the US runs out of excess crude...

Editor’s Note: The above chart has been updated with the latest figures. The same forecast for the end of July holds.

Using the current tanker flow activity, US crude exports are expected to remain elevated until the end of June. As for after June, I think the tighter crude storage environment will start to pressure US crude exports lower. This will then manifest into even higher buying pressure from Asia.

The troubling thing about everything I’m writing is that now that we are here in the breaking point timeline, even a full reopening of the Strait of Hormuz in early May will ensure that no real flows to Asia occur until mid-July.

How will the market keep balancing the ~11 to ~13 million b/d outage until then?

I don’t know, but price will have to do most of the heavy lifting.

Asia ex-China is already seeing the steepest drop in crude storage in history. Most of those barrels belong to Japan and South Korea, so the lack of crude in storage will create the panic buying we described above.

The ripple effect is underway now. It’s too little too late.

It is what it is...

The oil math is hard to fathom, but we’ve never been in this situation before. We’ve never had an outage anywhere near 11 to 13 million b/d. As I wrote before, none of the energy specialists disagree on the math because we used to argue over 500k b/d to 1 million b/d. Once the outage reached this size, arguing between 11, 13, or 9 million b/d becomes irrelevant. The level of demand destruction needed to balance the market will be either 4x or 6x that of the previous recession. You see, it starts to lose meaning after a while.

And unlike most sellside analysts, I can’t tell you what price everything will settle at. If they were intellectually honest, they would tell you the same. The sequencing I explained above requires us to react in real-time. There’s no predetermined outcome here. We can only assume the price will be higher than today’s because demand has not fallen anywhere near 11 to 13 million b/d.

Instead, the point of the article is to offer you the roadmap of how I see the events unfold. To recap the turning point:

Refining margins will fall first.

Crude timespreads will materially lose the backwardation.

Visible onshore inventories start to bottom.

So long as we are equipped with the tools to spot the turning point, I know I am well prepared for the scenarios ahead. In the meantime, let the geopolitics do its thing; we can only focus on the things we can control.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of USO, UCO, BNO either through stock ownership, options, or other derivatives.

How would the sequence change under:

1) U.S. crude-export ban

2) U.S. clean-product export ban

3) both?

My intuition is that a crude-only ban widens Brent-WTI rather than collapses it, (traps light sweet?), while a product ban crushes local cracks and forces run cuts before the U.S. crude squeeze fully completes.

What do you think about the grade mismatch here?

In light of that possibility, what's the right mix of Brent, WTI, and products for our longs?