A month ago, we wrote an article titled, "U.S. Oil Production Report Out With Far More Questions Than Answers." The gist of the article was that if we added adjustment to US oil production, total crude supplies in December came out to 13.719 million b/d. We wrote at the time that the January report will result in a major downward revision to reflect the overstated figure in December.

Fast forwarding to today, EIA reported the latest US oil production for January 2024 and it was a doozy.

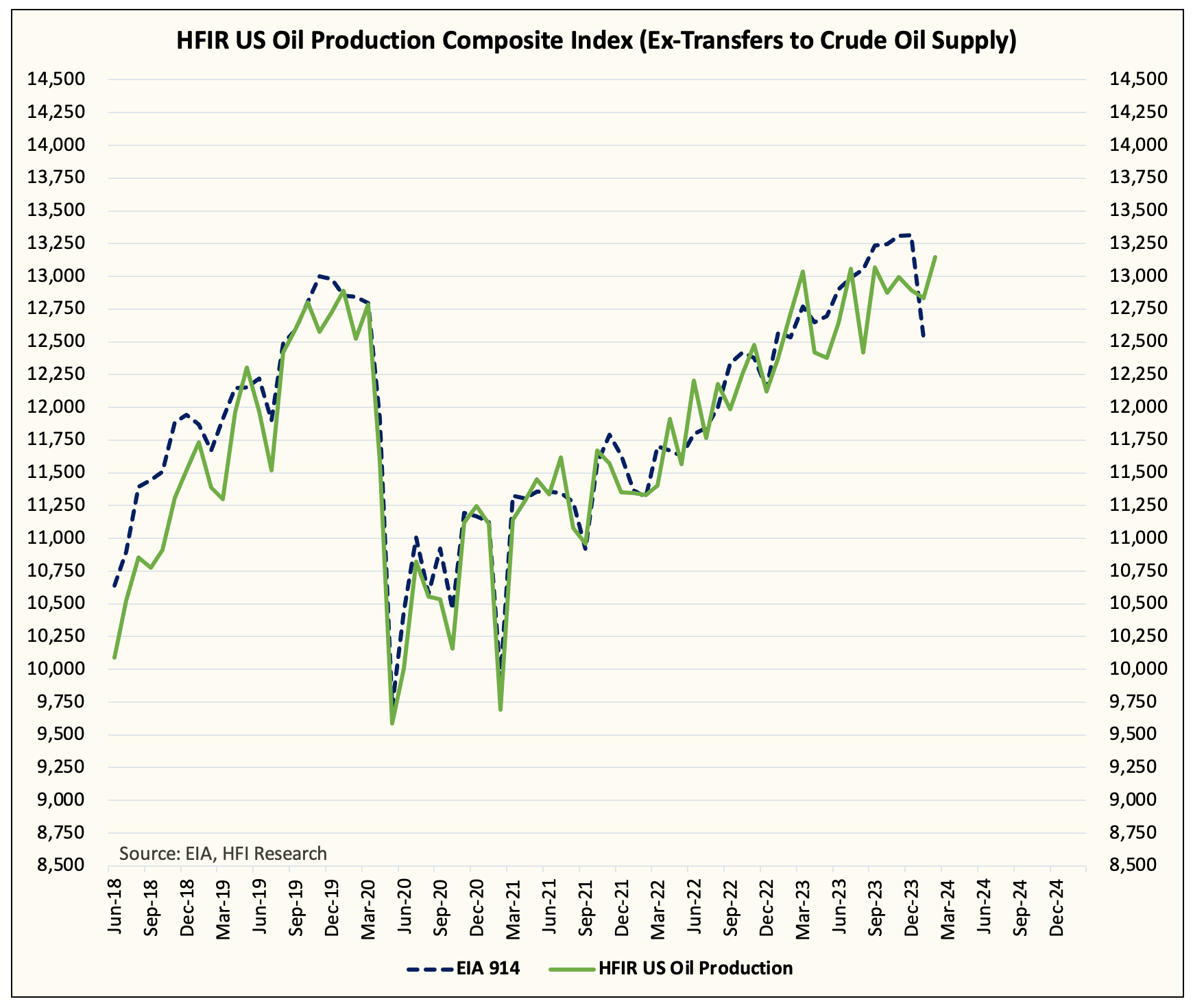

Source: EIA

For January, US oil production came in at 12.533 million b/d. The adjustment came in at -43k b/d.

Total crude supply was 12.976 million b/d. Excluding transfers to crude oil supply, crude + adjustment was 12.49 million b/d.

Relative to our model, US oil production came in well below what we had expected. Our real-time US oil production data showed a reading of 12.833 million b/d.

Why is the difference so large?

First, it's important to remember that January experienced a very severe snowstorm that shut-in US oil production. We saw this in real-time in natural gas production data.

Since then, Lower 48 gas production has recovered and our real-time US oil production figure puts the average around ~13.148 million b/d for February.

Second, we believe it has to do with the fact that EIA materially overstated the total crude supply in December. As we wrote last month, ~13.7 million b/d for crude + adjustment overstated US oil production by ~900k b/d. In turn, January has eliminated ~400k b/d of that with February likely to show another month of negative adjustment.

Since EIA made the change to its reporting methodology in June 2023, we are seeing a material overstatement of US oil production from the EIA 914.

The new methodology change, while encouraged, has resulted in this large disparity. As a result, the market is being fooled into thinking US oil production is larger than it looks.

Hammering away this point until people get it...

EIA understated US oil production at the end of 2022 and overstated US oil production at the end of 2023. The end result was a headline production growth figure of ~1 million b/d, when the reality was closer to 400k b/d to 500k b/d. We explained why in this article.

And because the growth rate was much smaller than what headline figures showed, the implied velocity of growth going forward will also be much smaller.

Our base case view is that US oil production will finish this year around ~13.3 to ~13.4 million b/d (growth of +300k b/d to +400k b/d), but on the surface, it will look like US oil production has stalled out completely. Either way, the truth is going to be revealed to the market by year-end.

Implications for the oil market... It all starts with domestic US crude storage

The first domino to fall because of inherently lower US oil production is US commercial crude storage. Because real US oil production is lower, the total crude supply will be lower, which will result in the weekly EIA crude storage reports to surprise to the upside. This will, in turn, tighten domestic US crude storage to the point of shutting in US crude exports.

Source: Barchart.com

We are already seeing this in WTI timespreads. This coupled with the material narrowing we are seeing in Brent - WTI tells us that US crude exports will fall going forward.

Source: Barchart.com

And since US crude exports are such a dominant variable in the US crude storage balance, the easiest way to keep more supplies domestically is by shutting off export arbitrage.

But as US crude exports fall, Brent along with other global light sweet crude grades will tighten. Given that US commercial crude storage is already ~30 million bbls below last year, US crude exports should be lower y-o-y.

Signals

The easiest way for readers to validate whether or not we are right about US oil production is to watch the weekly US commercial crude storage estimates. Typically, if US oil production is underperforming, then the draw will be larger than our estimate or the build will be lower than our estimate. This is by far the easiest way to know in real-time just how much US oil production is outperforming or underperforming by (vs our tracker).

Second, if we are right that US oil production is lower than what it appears, then you will see WTI timespreads remain in backwardation. Tightness in the US crude storage market is needed to validate our thesis here.

Lastly, it should all manifest into US crude exports. When you see US crude exports flatline over the summer relative to last year, you will know that we are correct about underperforming US oil production.

Conclusion

US oil production is a lot uglier than you think. Overstated US oil production into the end of 2023 made people falsely believe that US oil production growth exit-to-exit returned to +1 million b/d, when the reality was closer to +500k b/d. The velocity of growth is important here because it directly links to how you project supply growth for the years ahead. And with US shale peak here sooner than people expect, the oil market going forward will also be much tighter than people expect.

Analyst's Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours.