For the past year, we've been pounding the table that 1) US oil production growth is materially lower than the consensus estimate and 2) US shale oil production is getting increasingly gassier.

Throughout 2024, the high-frequency data continued to validate our thesis with US oil production growth ending 2024 at the weakest exit-to-exit production growth since the shale revolution started in 2016.

And looking at the chart, 2025 is not doing any better.

Going Into Detail

Using our real-time US oil production tracker, you can see that the 4-week moving average is materially lower y-o-y. It is important to keep in mind that January US oil production was impacted by weather-related events. The freeze-off impacted production by ~500k b/d.

We saw this manifest in lower natural gas production via real-time pipeflow data.

But the troubling disconnect, and the basis for this article, is that US oil production meaningfully disappointed starting in December.

This is important to note because historically, US oil production ramps the hardest in Q4. Without a Q4 ramp in production, Q1 and Q2 of the following year usually exhibit very weak production profiles. Seasonality, capex timing, and natural decline usually push US oil production materially lower in the following quarters. So we won't see any pickup in US shale oil production until H2 2025, which by this point will show a lower absolute US oil production figure.

The high base decline of US shale will be the key reason why the ~13.5 to ~13.7 million b/d is a permanent plateau.

More importantly for us, the disappointment in US oil production comes at a time when the consensus expected a meaningful ramp in production thanks to higher natural gas takeaway capacity in the Permian.

On Sept 16, Javier Blas wrote an article noting that the Matterhorn expansion could meaningfully boost Permian oil production. Since then, our real-time US oil production only shows disappointing production figures.

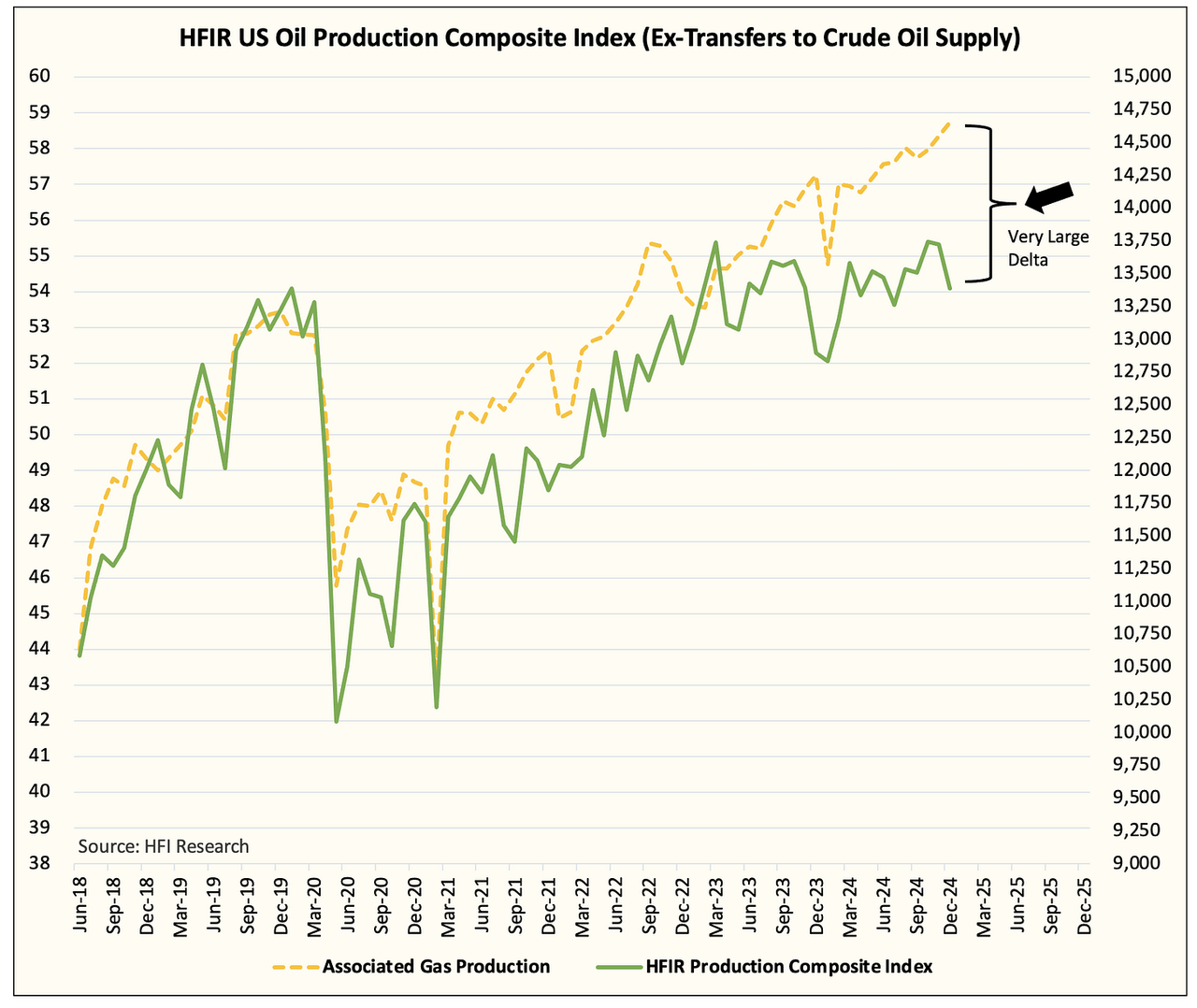

Meanwhile, associated natural gas production is on pace to hit an all-time high.

Again, none of this is a surprise to informed readers. We've been hammering this point away for over a year now, and the data is just becoming that obvious.

With the latest data, we can confirm that the report we wrote earlier this year is on track. This is where the beauty of real-time data comes in. In the latest EIA weekly oil storage report, implied US oil production came in at 12.63 million b/d.

Even if we factor in "noise", the 2-week average shows US oil production at 12.96 million b/d and the 4-week average shows US oil production at 12.946 million b/d.

So why am I pounding the table? Because associated gas production last week hit an all-time high. Even if we normalize our real-time US oil production from 12.63 million b/d to 12.96 million b/d (2-week average), the delta is becoming too large to ignore.