Please read the following articles on the oil market breaking point:

(WCTW) The Oil Market Breaking Point

(WCTW) The Oil Market Breaking Point Is Here

(WCTW) The Oil Market Breaking Point And How It Unfolds

We have reached the point of no return. In the past week, sellside analysts came out in unison declaring that the Strait of Hormuz will reopen sometime in June. JPM, Goldman, and Morgan Stanley are all basing their assumptions on the Strait opening “soon” and oil prices remaining around $100 through year-end.

If you are like me and have spent time analyzing the geopolitics, you may have arrived at a different conclusion. I detailed my thoughts on the endgame here.

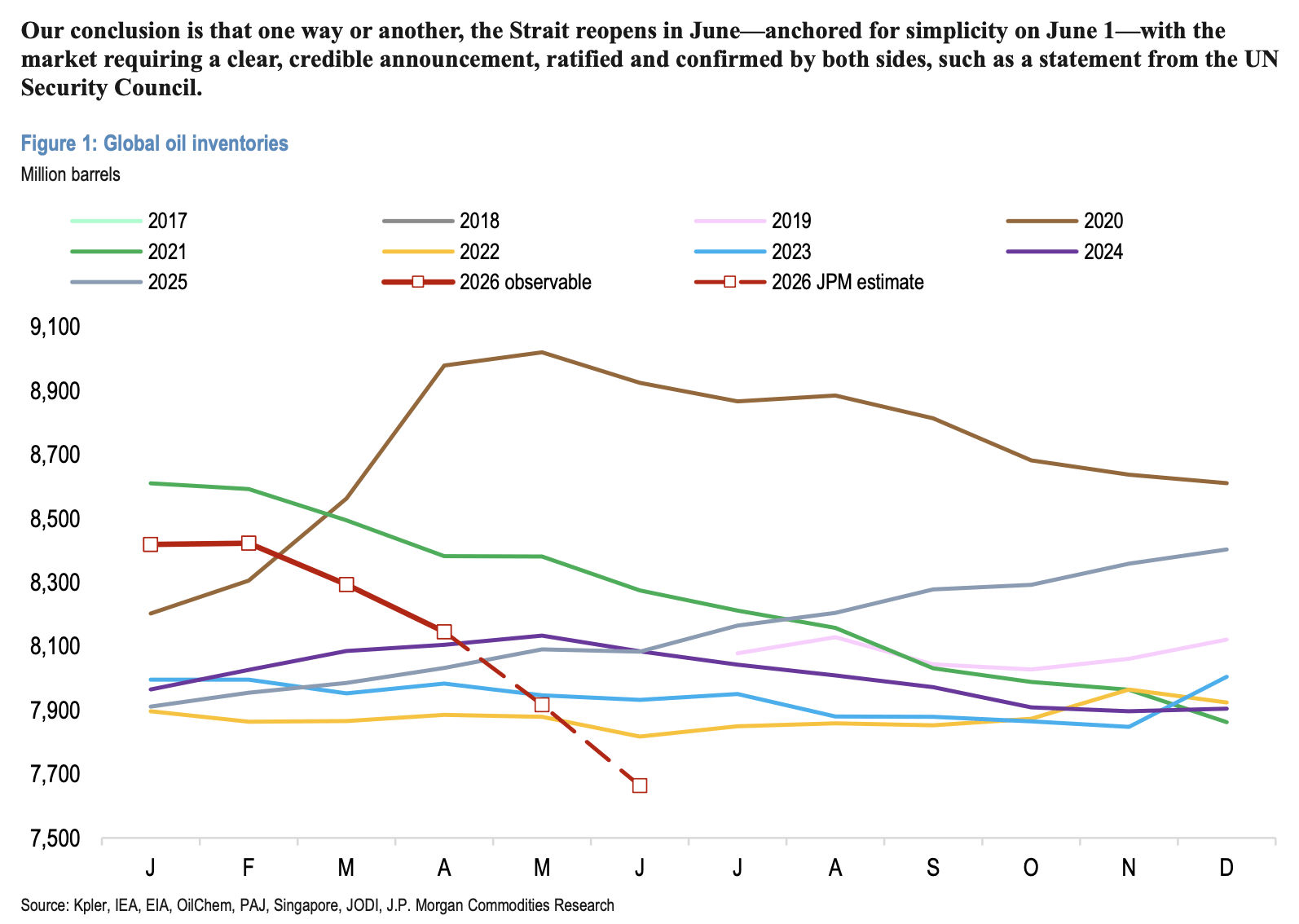

One of the most notable reports came from JPM’s team, which noted that the Strait of Hormuz will open one way or another because we are going to hit tank bottom in global oil inventories if it doesn’t open by June.

A core assumption of our framework is that the accelerating pace of oil inventory depletion will ultimately force the reopening of the Strait of Hormuz, one way or another.

And to be totally fair to the sellside community, this type of analysis is needed for those investing in energy stocks. Some degree of return to normality is required when assessing how to underwrite energy stocks. But for the purposes of analyzing where oil prices are headed, this is not the type of analysis you want to publish.

The issue is that everyone who runs a global oil supply & demand model understands the implications. Now that we are a month past the oil market breaking point, logistical constraints make it impossible for production shut-in to restart until August.

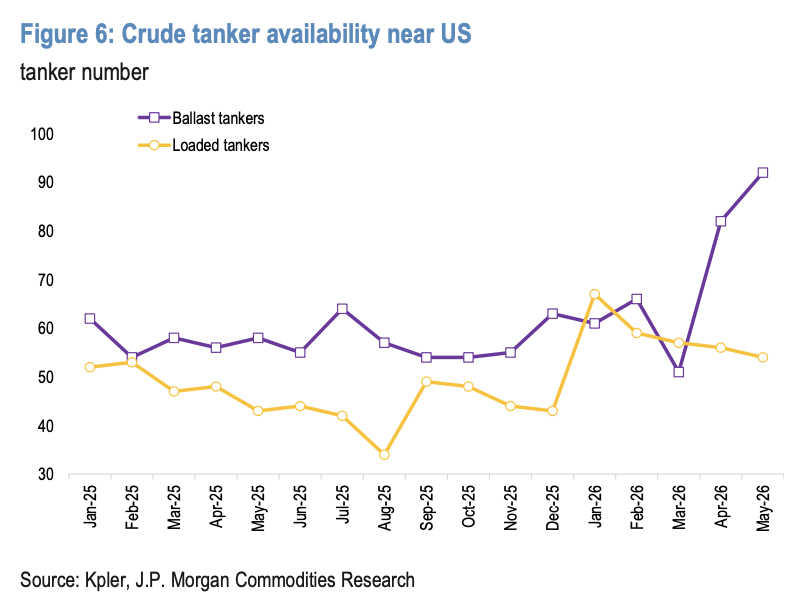

Most ballast tankers are headed for the US to drain the last remaining excess crude in storage, and the time it will take to return to the Persian Gulf all but guarantees more delays.

And that’s assuming we actually find a resolution by June 1. If not, I reckon the consensus will be in for a very rude awakening.

This brings me to the point of this article: we have now entered the point of no return. Since the beginning of the conflict, my core thesis has been simple: every day that passes without a resolution increases the probability that there is no resolution.

Emotional and cognitive biases prevent people at the top from reaching a diplomatic resolution when the cost of anchoring becomes too great. From the US’s side, leaving now would look like a total strategic defeat, while for the Iranians, the cost of enduring the current conflict has already been spent; you will anchor down and outlast your adversary.

So to assume that the Strait of Hormuz will reopen by June 1 is just wishful thinking. I am somewhat relieved that the sellside community has not analyzed what it would do to oil prices if the Strait remains closed. When that day comes, it could be a contrarian signal to start exiting our oil long exposure. But judging by the reports I went through the past week, we are quite a ways from that scenario.

There’s nothing like price changing the narrative. I guess only time will tell who changes their tone first.

The Point of No Return

The implied oil flow for May has averaged -7.5 million b/d.

This makes sense considering the following variables:

Production shut-in: 12 million b/d

Demand loss: 2 million b/d

SPR: 2.5 million b/d

Net: 7.5 million b/d